179Views 0Comments

Debt Consolidation Loans: Lower Your Monthly Payments

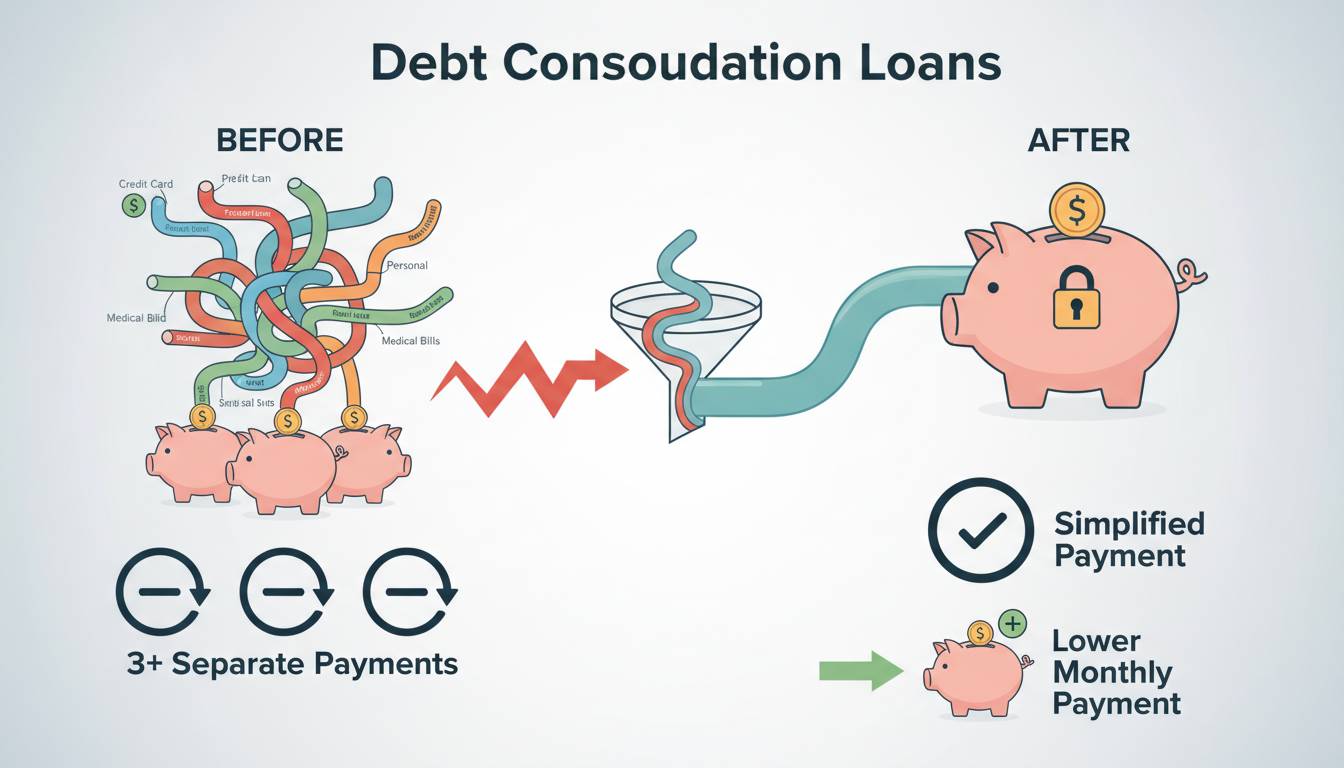

If you’re juggling multiple credit card bills, medical debts, and personal loans, you might have considered rolling them all into one payment. That’s essentially what a debt consolidation loan does—and for many Americans drowning in high-interest debt, it can actually work.

Here’s how it works: you take out a new personal loan (usually at a lower interest rate than what your current debts charge), use that money to pay off everything you owe, and then make a single monthly payment to your new lender. Instead of tracking five different due dates and interest rates, you just have one bill.

The math can work out nicely. Credit card rates often exceed 20% or even 30%. A consolidation loan might get you 10% or 12% if your credit is decent. Over the life of a three-to-five-year loan, that difference can mean thousands of dollars in savings.

Understanding Debt Consolidation Loans

Debt consolidation loans are unsecured personal loans offered through banks, credit unions, and online lenders. “Unsecured” means you don’t put up collateral—no house, no car. Approval depends on your credit score, income, and debt-to-income ratio.

The big selling point is simplicity. One payment, one due date, one interest rate. But here’s the catch: you still need to qualify for a rate that’s actually lower than what you’re paying now. If your credit isn’t great, you might not save much—or anything at all.

The Current State of Consumer Debt in America

Americans now carry over $17 trillion in consumer debt. Credit card balances keep climbing, and a lot of households are juggling multiple cards with punishing interest rates.

In this environment, consolidation makes sense for some people. The fixed rate gives you predictability—your payment doesn’t suddenly jump because the Fed changed interest rates. But it’s not magic. You’re not eliminating debt; you’re restructuring it. And if you don’t change the habits that got you into debt in the first place, you could end up in a worse position.

Benefits of Debt Consolidation Loans

Simplified Financial Management

One payment is easier to track than five or six. Less chance of missing something and getting hit with late fees.

Potentially Lower Interest Rates

This is the main reason people consolidate. A few percentage points might not sound like much, but it adds up over time.

Fixed Repayment Timeline

Credit cards let you pay the minimum forever (or close to it). A consolidation loan has a set end date. That can actually help you pay off debt faster instead of letting it drag on.

Improved Credit Score Potential

Paying off credit cards improves your credit utilization ratio. Making on-time payments on the new loan builds positive payment history. Both can boost your score over time.

Risks and Considerations

You Might Not Qualify for a Better Rate

If your credit is poor, you might not get offered anything better than what you’re already paying. Or you might not get approved at all.

Watch Out for Fees

Some loans charge origination fees or balance transfer fees. Read the fine print. A fee of 3-5% can eat into your savings.

You Still Need to Change Habits

Paying off credit cards doesn’t mean you can’t use them again. If you run up new balances while paying off the consolidation loan, you’ll be worse off than before.

Longer Terms Can Cost More

Lower monthly payments feel good, but stretching the loan out for five or seven years might mean paying more total interest—even with a lower rate.

How to Qualify for the Best Rates

Lenders look at several things:

- Credit score: Above 700 usually gets you the best rates. Below 640, expect problems.

- Debt-to-income ratio: Most lenders want this below 40%.

- Income stability: Consistent employment helps.

- Existing relationships: If you bank somewhere, ask what they can offer. Credit unions often have competitive rates.

Check your credit report for errors before applying. Fixing mistakes can give your score a quick boost.

Steps to Pursue Debt Consolidation

-

List everything you owe. Balances, interest rates, minimum payments. Know what you’re working with.

-

Shop around. Get quotes from at least three lenders. Online platforms, your bank, a local credit union—check them all. Most let you prequalify without hurting your credit.

-

Apply. Approval can take anywhere from hours to a week. Once approved, you either get a check or the lender pays your creditors directly.

-

Commit to the plan. Set up automatic payments. Close the old credit cards if you have to. Don’t rack up new debt.

The Future of Debt Consolidation

Fintech companies are making it easier to compare options and see exactly how much consolidation might save you. AI is speeding up approvals. And regulators are paying more attention to predatory lending—good news for consumers.

Interest rates will fluctuate with the economy, which means the value of consolidation will too. What makes sense today might not next year.

Conclusion

Debt consolidation works well for people with stable income, decent credit, and the discipline to stop accumulating debt. It simplifies payments and can save money on interest. But it’s not a fix for overspending, and it’s not the right move for everyone. Do the math, read the fine print, and make sure you’re not just moving debt around without actually paying it down.

Frequently Asked Questions

What’s the difference between a debt consolidation loan and a balance transfer card?

A consolidation loan is an installment loan with a fixed rate. A balance transfer card usually gives you 0% interest for a promotional period—often 12-18 months—but then hits you with a much higher rate. Balance transfers also typically charge a 3-5% fee. Consolidation loans have rates that stay the same the whole time.

How long does approval take?

Online lenders: sometimes same day, usually one to two days. Banks: a few days to a week. Funding usually happens within a week of approval.

Will this hurt my credit?

The application itself causes a small, temporary dip from the hard inquiry. But if you pay off old cards and make on-time payments on the new loan, your score will likely improve within a few months.

Can I consolidate car loans or mortgages?

Those are secured debts—your car or house is collateral. You’d need to refinance them separately. Trying to roll them into an unsecured personal loan generally doesn’t work and probably isn’t a good idea.

What if I can’t make payments?

Contact your lender immediately. Many offer hardship programs or payment modifications. Missing payments hurts your credit and can lead to default. The sooner you act, the more options you have.

Is this right for everyone?

No. It’s best for people with multiple high-interest debts, stable income, and the ability to avoid new debt. If your credit is poor, you might not get a better rate. And if you can’t stop overspending, consolidation just delays the problem.