184Views 0Comments

Cryptocurrency Investment: Proven Strategies for Maximum Returns

The cryptocurrency market moves fast—so fast it can feel overwhelming. If you’re an American investor trying to figure out whether digital assets fit into your portfolio, this guide breaks down what actually matters without the hype.

The Current State of Crypto

Let’s be honest: crypto isn’t going anywhere. Bitcoin and Ethereum have been around for over a decade, and the market now sits comfortably above $1 trillion in total value. Daily trading volumes routinely exceed $50 billion. That’s real money, and it’s attracted real institutional players—hedge funds, pension funds, the kind of names you’d see on a traditional Wall Street balance sheet.

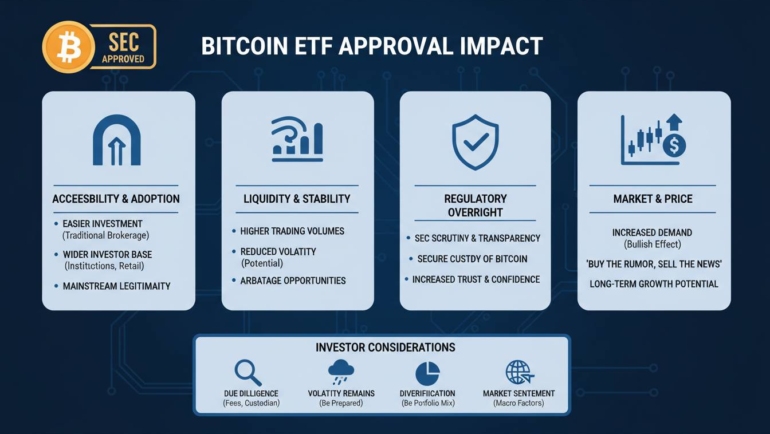

The big shift happened when regulators started approving exchange-traded products. Now you can get exposure to Bitcoin through your regular brokerage account without dealing with digital wallets or learning how crypto exchanges work. That’s a game changer for a lot of investors who were curious but didn’t want the technical headache.

Ethereum made its own big move to proof-of-stake, which essentially made the network more energy-efficient and changed how the whole system economics works. Whether that’s good or bad depends on who you ask, but it’s worth understanding if you’re holding ETH.

What Actually Works

I’m going to be straight with you: there’s no secret formula. If there were, everyone would use it. But some approaches have proven more sustainable than others.

Dollar-cost averaging is the strategy most people actually stick with. You put in a fixed amount every month—say $500—regardless of whether prices are up or down. This removes the impossible task of timing the market. You won’t buy at the absolute bottom, but you also won’t fomo in at the top. Over time, this smooths out the volatility problem that makes crypto so stressful.

Diversification sounds obvious, but people get it wrong. Don’t just buy five different coins because they seem different. Look at how assets correlate. Layer-one blockchains, DeFi tokens, and utility tokens all behave differently depending on what’s driving the market. Spreading across these sectors actually reduces volatility rather than just adding more volatile positions.

Research matters more than memes. Before buying anything, dig into the fundamentals: Is the network secure? Are developers actually building on it? What’s the token supply and distribution look like? A coin with 90% of supply held by insiders is a different bet than one with fair distribution. This is boring work, but it’s the difference between investing and gambling.

Risk Management Nobody Talks About

Here’s the uncomfortable truth: crypto can go to zero. Not to scare you off, but to make sure you’re allocating money you can actually afford to lose.

The 5-10% rule gets thrown around a lot, and it’s reasonable. If you have $100k in total investments, $5-10k in crypto gives you exposure without destroying your financial plan if things go wrong.

On the security side, if you’re holding significant amounts, hardware wallets are non-negotiable. Exchange hacks happen. Two-factor authentication is the bare minimum. And please—ignore the DMs from people promising to double your money. That’s always a scam.

Stop-loss orders are useful if you can’t watch your portfolio every day. Set them at a level where you’d want to exit anyway. Don’t just panic-sell at -50% because you didn’t think it through beforehand.

The Regulatory Mess

I won’t pretend this is clear. It’s not. The SEC keeps suing exchanges and projects. The CFTC has its own ideas about what’s a commodity versus a security. The IRS treats crypto as property, which means every trade is a taxable event. Yes, even swapping one coin for another.

State laws vary too. Some states are crypto-friendly; others make life difficult. If you’re using a platform, check that it operates in your state.

The bottom line: keep meticulous records. Crypto tax software helps. So does a good accountant who understands this space.

What Institutional Adoption Actually Means

Big financial institutions now offer custody services for crypto. Asset managers have launched investment products. This matters because it brings legitimacy—and liquidity. But it also means crypto behaves more like a traditional asset during market stress. The “uncorrelated asset” narrative has cracked during major selloffs.

Where Things Are Heading

Layer-2 solutions are solving the speed and cost problems that have plagued Ethereum. DeFi keeps building financial tools outside traditional banking. NFTs found real utility beyond JPEGs—gaming, identity, ownership tracking.

CBDCs are still experimental in the US, but other countries are further along. Whether a digital dollar happens in your lifetime is an open question.

Common Questions

Is crypto right for me?

Only you can answer this. It comes down to risk tolerance, timeline, and whether you understand what you’re buying. Don’t invest money you need in the next five years. Don’t invest because FOMO is telling you to.

How do I start?

Pick a reputable exchange that operates in your state, complete verification, fund your account, and start with Bitcoin or Ethereum. Move holdings to a hardware wallet if you’re planning to hold for years.

What about taxes?

Every trade is a taxable event. Use crypto tax software or work with a professional. The penalties for getting this wrong are real.

How much should I put in?

Most advisors suggest 5-10% maximum. Adjust based on your situation—but don’t treat crypto as your retirement plan.

Are exchanges safe?

Safer than they used to be, but not bulletproof. Keep significant holdings in cold storage. Don’t leave money on exchanges longer than necessary.

Bitcoin vs. Ethereum?

Bitcoin is digital gold—a store of value with fixed supply. Ethereum is a platform for apps and smart contracts. Different tools for different jobs.

The Real Talk

Crypto isn’t a get-rich-quick scheme, and anyone telling you otherwise is selling something. It’s a legitimate asset class with real use cases—and real risks. The strategies that work here aren’t different from investing anywhere else: do your homework, manage risk, don’t invest money you can’t afford to lose, and expect the unexpected.

The market will keep evolving. Regulators will keep debating. New technologies will keep emerging. Your job is to stay informed, stay skeptical of hype, and make decisions that make sense for your actual financial situation.