137Views 0Comments

Decentralized Finance Explained: Complete Beginner’s Guide

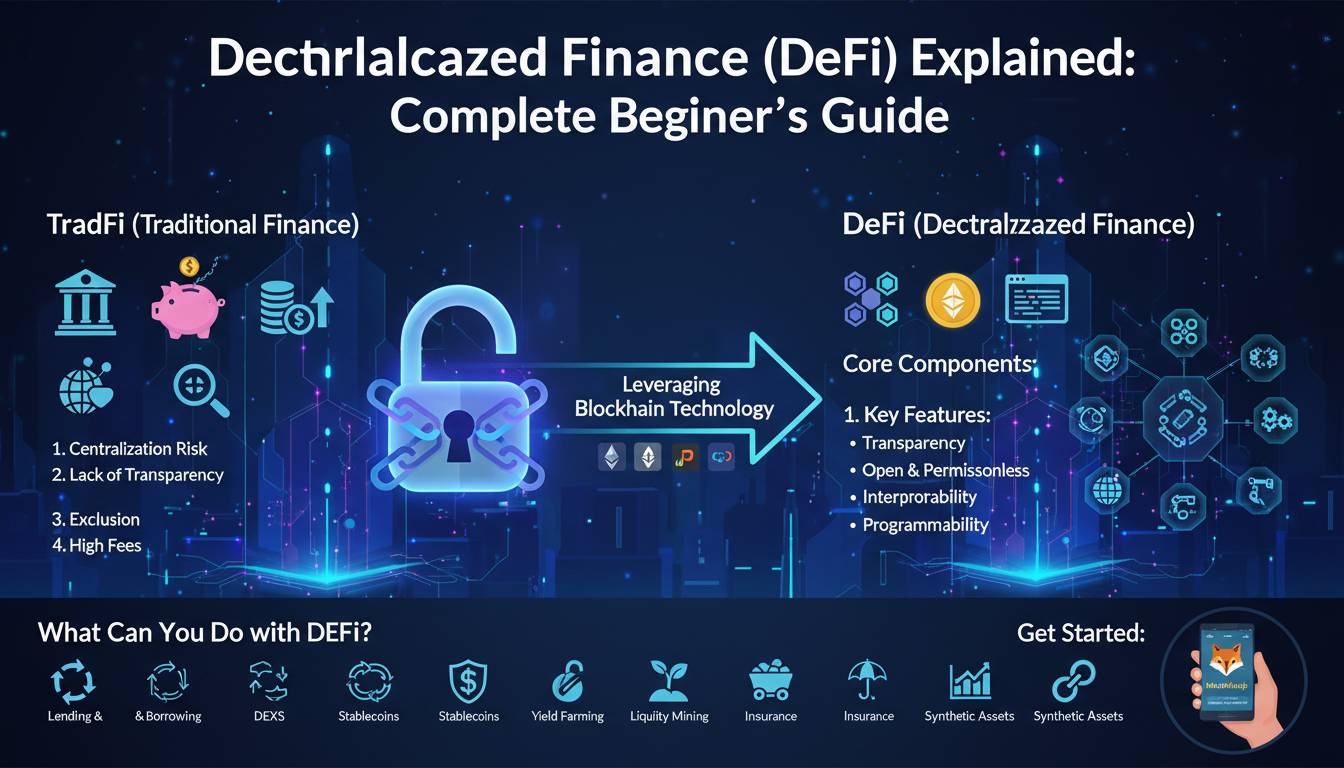

Decentralized finance, commonly called DeFi, represents a revolutionary approach to financial services that operates without traditional intermediaries like banks, brokers, or insurance companies. Instead, DeFi uses blockchain technology and smart contracts to enable peer-to-peer financial transactions—allowing anyone with an internet connection to lend, borrow, trade, and earn interest on assets directly from their digital wallet. This fundamental shift in how money moves around the world has grown from a niche crypto experiment into a multi-billion-dollar ecosystem that challenges the entire traditional financial infrastructure.

Key Insights

- DeFi eliminates middlemen by using self-executing smart contracts on blockchains like Ethereum

- The total value locked in DeFi protocols has reached billions of dollars, showing mainstream adoption

- Users can earn significantly higher interest rates on savings compared to traditional banks

- Smart contracts automate financial agreements, removing the need for trust in institutions

- DeFi operates 24/7, unlike banks that close evenings and weekends

What Exactly Is Decentralized Finance?

DeFi refers to a collection of financial applications built on public blockchains that replicate traditional financial services but remove the centralized intermediaries. When you use a conventional bank, you trust that institution to hold your money, process your transactions, and honor your agreements. DeFi replaces this institutional trust with cryptographic code and network consensus.

The core innovation enabling DeFi is the smart contract—a self-executing program stored on a blockchain that automatically enforces the terms of an agreement when predetermined conditions are met. For example, if you want to lend your cryptocurrency to earn interest, a smart contract can automatically distribute interest payments to your wallet without any human involvement or intermediary taking a cut.

Unlike traditional finance, which operates within national boundaries and requires extensive identity verification, DeFi is borderless and pseudonymous. Anyone with a compatible wallet can interact with DeFi protocols regardless of their location or citizenship status. This accessibility represents perhaps the most transformative aspect of decentralized finance—financial services traditionally available only to those with good credit scores, banking relationships, or substantial wealth become accessible to anyone with an internet connection and a small amount of cryptocurrency to get started.

The DeFi ecosystem encompasses numerous financial products and services, including decentralized exchanges where users trade cryptocurrencies directly with each other, lending protocols that allow users to supply assets and earn interest or borrow against collateral, yield farming strategies that maximize returns across multiple protocols, and synthetic assets that represent real-world commodities and financial instruments.

How DeFi Works: The Technical Foundation

Understanding DeFi requires grasping three foundational technologies: blockchain networks, smart contracts, and decentralized oracles. Together, these components create a trustless financial infrastructure where participants can verify and execute transactions without relying on any central authority.

Blockchain networks serve as the foundational ledger recording all DeFi transactions. Ethereum remains the dominant platform for DeFi development, hosting the majority of popular protocols. Other blockchains including Solana, Avalanche, and Binance Smart Chain have also developed substantial DeFi ecosystems offering varying levels of functionality, speed, and cost. These networks maintain consensus across thousands of nodes, ensuring that transaction records remain transparent and resistant to manipulation.

Smart contracts are the building blocks of DeFi applications. Written in programming languages like Solidity for Ethereum, these contracts define the rules governing financial interactions. A lending protocol’s smart contract, for instance, contains code specifying interest rates, collateral requirements, liquidation conditions, and the mechanics of supplying and borrowing funds. Because these contracts run exactly as written without possibility of modification or interference, users need only trust the code rather than any counterparty.

Decentralized oracles address a critical challenge: smart contracts cannot access external data on their own. A protocol needs to know the current price of Ethereum to determine whether a loan position should be liquidated, for instance. Oracle networks like Chainlink aggregate real-world data from multiple sources and deliver it to smart contracts in a trustworthy manner, enabling DeFi protocols to interact with real-world information.

| Component | Function | Example |

|---|---|---|

| Blockchain | Immutable transaction ledger | Records all lending and borrowing activity |

| Smart Contract | Self-executing financial logic | Automatically calculates and distributes interest |

| Oracle | External data delivery | Provides real-time asset prices for liquidation decisions |

| Wallet | User interface for interactions | MetaMask, Rainbow, or Coinbase Wallet |

The composability of DeFi represents one of its most powerful characteristics. Because all DeFi protocols are built on public blockchains with open-source code, developers can combine multiple protocols to create new financial products. A developer might build an application that automatically supplies collateral to a lending protocol, borrows against that collateral, uses borrowed funds to provide liquidity to a decentralized exchange, and routes trading fees back to the user. This stackable architecture allows innovation to compound rapidly across the ecosystem.

Major DeFi Use Cases and Applications

The DeFi ecosystem has expanded to encompass virtually every traditional financial service, with some applications offering capabilities that conventional finance cannot match. Understanding these use cases helps clarify both the current state and future potential of decentralized finance.

Decentralized Exchanges (DEXs) allow users to trade cryptocurrencies directly from their wallets without depositing funds on a centralized exchange. Uniswap, SushiSwap, and Curve Finance use automated market maker algorithms that price assets based on supply and demand in liquidity pools rather than matching buy and sell orders like traditional exchanges. This innovation enables continuous liquidity and operates continuously without trading hours or order book limitations.

Lending and borrowing protocols like Aave, Compound, and MakerDAO enable users to supply cryptocurrency as collateral and borrow other assets. These platforms use algorithmic interest rates that adjust based on supply and demand, often offering significantly higher yields on deposits than traditional savings accounts. Borrowers can obtain liquidity without selling their crypto holdings, avoiding taxable events while maintaining exposure to asset appreciation.

Yield farming involves strategically moving assets across multiple DeFi protocols to maximize returns. A yield farmer might supply stablecoins to a lending protocol to earn interest, then stake the received protocol tokens for additional rewards, then deposit those tokens in another protocol for even more yield. While potentially profitable, yield farming requires sophisticated understanding of smart contract risks, impermanent loss, and token volatility.

Stablecoins like USDC, DAI, and USDT maintain a peg to fiat currencies, typically the US dollar. These cryptocurrencies provide the stability necessary for DeFi transactions, enabling users to borrow, lend, and trade without exposure to the extreme volatility of uncorrelated cryptocurrencies. Centralized stablecoins like USDC maintain reserves audited by traditional accounting firms, while decentralized variants like DAI use over-collateralization with other cryptocurrencies to maintain their peg.

Benefits and Advantages of Decentralized Finance

DeFi offers several compelling advantages over traditional financial systems, though these benefits come with corresponding risks that users must understand before participating.

Financial inclusion stands as DeFi’s most transformative potential. Approximately 1.4 billion adults globally lack access to traditional banking services, according to World Bank data. DeFi requires only an internet connection and a smartphone, removing geographic barriers, minimum balance requirements, and the need for extensive identity documentation that traditional banks often demand.

Higher yields on savings and lending represent a significant advantage. Traditional banks offer annual percentage yields often below 0.10% on savings accounts, while DeFi lending protocols have historically offered yields ranging from 2% to 8% on stablecoin deposits, and substantially higher yields on volatile assets. These differences reflect both the efficiency of removing intermediaries and the risks inherent in cryptocurrency volatility.

Transparency in DeFi surpasses what traditional finance can offer. Every transaction, interest rate, and smart contract function is publicly visible on the blockchain. Users can independently verify protocol TVL (total value locked), audit code for vulnerabilities, and track exactly how their funds are being used. This radical transparency enables community oversight that traditional financial institutions simply cannot match.

Speed and accessibility characterize DeFi transactions. Cross-border payments that traditionally require days and multiple intermediary fees settle within minutes on blockchain networks. The financial infrastructure operates continuously without closing times, allowing users to access liquidity or execute trades whenever needed.

| Traditional Finance | Decentralized Finance |

|---|---|

| Hours: Weekdays 9-5 | 24/7/365 operation |

| Settlement: 2-5 business days | Minutes to hours |

| Interest on savings | ~0.01% APY |

| Minimum accounts often required | No minimums |

| Requires identity verification | Pseudonymous |

| Single currency per region | Any cryptocurrency |

Programmable money enables novel financial products impossible in traditional systems. Smart contracts can encode complex conditions that automatically execute based on real-world events, market movements, or time-based triggers. Insurance protocols can automatically pay claims when oracles confirm covered events occurred. Derivatives can be structured with conditions impossible to enforce through traditional legal contracts.

Getting Started with DeFi: A Practical Walkthrough

Entering the DeFi ecosystem requires careful preparation and systematic learning. The following framework helps beginners navigate their first steps while minimizing risks.

Step 1: Secure a cryptocurrency wallet. MetaMask remains the most widely supported wallet for Ethereum and EVM-compatible networks. Download the browser extension or mobile app, write down your seed phrase on paper (never digital), and never share this phrase with anyone. Anyone with your seed phrase controls your funds permanently.

Step 2: Acquire cryptocurrency. Most DeFi operations require gas fees paid in the native blockchain token—Ethereum on Ethereum Mainnet, SOL on Solana, and so forth. Purchase a small amount of the native token alongside your intended DeFi asset through a centralized exchange like Coinbase or Kraken, then transfer to your wallet. Keep enough native tokens for transaction fees.

Step 3: Connect wallet to a DeFi application. Navigate to a DeFi protocol’s website and look for a “Connect Wallet” button. Your wallet will prompt you to approve the connection. Always verify you’re on the correct website—phishing sites that mimic legitimate protocols have stolen millions in user funds. Check the URL carefully and consider using a hardware wallet for larger holdings.

Step 4: Start with small amounts. Begin with amounts you can afford to lose entirely. DeFi involves smart contract risk, smart contract bugs, temporary losses from providing liquidity, and the inherent volatility of cryptocurrency markets. The learning curve is real, and mistakes can be expensive.

Essential precautions for beginners:

- Never share your seed phrase with anyone, including support staff

- Always verify website URLs before connecting your wallet

- Use hardware wallets for significant holdings

- Start with small amounts while learning

- Research smart contract audits before using unfamiliar protocols

- Understand that cryptocurrency prices can drop significantly

Risks, Challenges, and Common Pitfalls

DeFi offers tremendous potential but comes with substantial risks that every participant must understand. The same openness and accessibility that make DeFi powerful also create opportunities for malicious actors and amplify the consequences of user error.

Smart contract vulnerabilities represent one of the most significant risks in DeFi. While audited protocols undergo extensive security reviews, vulnerabilities still emerge. The Wormhole bridge hack in 2022 resulted in approximately $320 million in losses due to a validation flaw. Ronin Network lost $615 million in another bridge exploit. These events demonstrate that even heavily audited systems can contain exploitable flaws.

Impermanent loss affects liquidity providers when the price relationship between deposited tokens changes significantly. AMM liquidity pools require token pairs to maintain trading balances, meaning providers can end up with less value than if they had simply held their tokens. Beginners should research impermanent loss extensively before providing liquidity.

Scams and phishing proliferate in DeFi’s unregulated environment. Fake token airdrops, fraudulent investment schemes, and cloned websites constantly target DeFi users. Never approve token transfers from unknown addresses, verify all website URLs meticulously, and be skeptical of any “free giveaways” or guaranteed returns.

Regulatory uncertainty creates ongoing risk for DeFi participants. Governments worldwide are developing approaches to cryptocurrency regulation, and significant policy changes could impact certain DeFi use cases or even make some activities illegal in certain jurisdictions. The permissionless nature of DeFi means regulators may target users rather than protocols.

| Risk Type | Description | Mitigation |

|---|---|---|

| Smart Contract Bugs | Code vulnerabilities exploited by attackers | Use audited protocols, start small |

| Impermanent Loss | Loss from providing liquidity vs holding | Understand before providing LP |

| Scams/Phishing | Fraudulent sites stealing credentials | Verify URLs, never share seed phrase |

| Regulatory | Policy changes affecting DeFi use | Stay informed, diversify geographically |

| Volatility | Crypto price swings affecting collateral | Don’t over-collateralize |

The Future of Decentralized Finance

DeFi continues evolving rapidly, with several emerging trends likely to shape the ecosystem’s near-term development. The convergence of traditional finance with blockchain technology, often called “CeFi meets DeFi,” is bringing institutional capital into the space through regulated on-ramps and compliant protocols.

Layer-2 scaling solutions like Arbitrum, Optimism, and zkSync are dramatically reducing transaction costs and increasing throughput on Ethereum. These technologies bundle multiple transactions together and settle them on the main Ethereum network, enabling DeFi applications that were previously impractical due to high gas fees. User experience improvements from scaling solutions may accelerate mainstream adoption significantly.

Real-world asset tokenization represents a significant expansion vector for DeFi. Protocols are developing infrastructure to represent real estate, treasury bonds, company equity, and other traditional assets on-chain. This integration could bring trillions of dollars in traditional assets into the DeFi ecosystem, creating new liquidity and enabling financial products previously impossible.

Cross-chain interoperability continues improving through bridges and cross-chain messaging protocols. As users can move value seamlessly between different blockchains, the DeFi ecosystem becomes more unified and liquid. However, bridge security remains a significant concern, with several major exploits targeting cross-chain infrastructure.

Institutional adoption is accelerating as major financial institutions develop cryptocurrency custody solutions, trade execution infrastructure, and investment products. BlackRock’s tokenized treasury fund, Franklin Templeton’s OnChain US Government Money Fund, and similar offerings from traditional finance giants signal growing legitimacy for blockchain-based financial services.

Frequently Asked Questions

Is DeFi legal in the United States?

DeFi operates in a regulatory gray area in the United States. Existing securities and commodities regulations may apply to certain DeFi tokens and protocols, and the SEC has indicated interest in regulating platforms that resemble regulated exchanges or investment vehicles. Users should consult qualified legal professionals regarding their specific situation and remain informed about evolving regulations.

How much money do I need to start using DeFi?

You can begin using DeFi with very small amounts. Some protocols have minimum deposits as low as a few dollars, though transaction fees (gas costs) on networks like Ethereum make small positions impractical. Starting with $100-500 provides enough capital to learn the mechanics while limiting potential losses from mistakes.

Can I lose all my money in DeFi?

Yes, complete loss of funds is possible in DeFi through several mechanisms: smart contract exploits can drain all protocol funds, rug pulls can eliminate worthless token investments, liquidation of collateral can occur during volatility, and simple user error like sending funds to wrong addresses results in permanent loss. Never invest more than you can afford to lose entirely.

How is DeFi different from regular cryptocurrency investing?

Regular cryptocurrency investing typically involves buying and holding tokens hoping for appreciation. DeFi involves actively using those tokens within financial protocols—lending, borrowing, providing liquidity, or automating yield strategies. All cryptocurrency investments carry risk, but DeFi adds smart contract risk, liquidation risk, and complexity requiring active management.

What’s the biggest risk for DeFi beginners?

The biggest risk is overconfidence leading to insufficient research. Beginners may connect wallets to unaudited protocols, approve malicious token permissions, provide liquidity without understanding impermanent loss, or take on excessive leverage without understanding liquidation mechanics. Education before participation is essential.

Conclusion

Decentralized finance represents a fundamental transformation in how financial services function globally. By replacing trust in institutions with trust in code and network consensus, DeFi creates opportunities for financial inclusion, transparency, and efficiency that traditional systems cannot match. The ecosystem has grown from experimental code to a multi-billion-dollar infrastructure supporting lending, borrowing, trading, and sophisticated financial engineering.

However, participating in DeFi requires genuine responsibility for your own security and education. Smart contract risks, market volatility, regulatory uncertainty, and sophisticated scams all threaten unwary participants. The advice to start small, research thoroughly, and never invest more than you can afford to lose applies more strongly in DeFi than almost any other financial domain.

As the ecosystem matures through improved scaling technology, institutional integration, and better security practices, DeFi’s benefits will likely become accessible to mainstream users who today find the technical barriers overwhelming. The question for interested participants is not whether decentralized finance will matter—its impact is already substantial—but whether they will participate as informed, prepared users ready to embrace both its opportunities and its risks.