212Views 0Comments

Crypto Tax Calculator: How It Works | Complete Guide

Understanding how crypto tax calculators work is essential for any investor navigating the complex intersection of cryptocurrency and tax obligations. These specialized tools have become indispensable as the IRS and state tax authorities increasingly scrutinize digital asset transactions, with failure to report potentially resulting in audits, penalties, and interest charges.

Key Insights

- Cryptocurrency is treated as property by the IRS, meaning every sale, trade, or transaction triggers potential capital gains or losses

- The average crypto investor faces calculating taxes across dozens or hundreds of transactions per year

- Professional crypto tax software can reduce calculation time from hours to minutes while minimizing errors

- The IRS has increased enforcement actions, with crypto transaction reporting now required on Form 8949 and Schedule D

What Is a Crypto Tax Calculator and Why Do You Need One?

A crypto tax calculator is specialized software designed to track, categorize, and calculate the tax implications of cryptocurrency transactions. Unlike traditional investment tax tools, these calculators must handle the unique characteristics of digital assets: multiple wallet addresses, blockchain confirmations, varied transaction types, and rapidly changing valuations.

The Internal Revenue Service treats cryptocurrency as property rather than currency, meaning each disposal triggers capital gains or losses calculation. A disposal includes selling crypto for fiat, trading one cryptocurrency for another, using crypto to purchase goods or services, and even receiving mined or staking rewards. This broad definition means virtually every crypto activity except simply holding generates a taxable event.

Crypto tax calculators solve several critical problems that manual tracking cannot address. First, blockchain transactions create an extensive transaction history that grows exponentially with active trading. A singleDeFi investor might execute hundreds of swaps, liquidity provision transactions, and token transfers annually. Manually tracking cost basis, acquisition dates, and sale prices across this volume invites calculation errors. Second, different calculation methods produce dramatically different tax outcomes. The same portfolio can result in thousands of dollars of tax difference depending on whether you use First-In-First-Out (FIFO), Last-In-First-Out (LIFO), or Specific Identification. Third, tax regulations continue evolving, with recent changes requiring detailed reporting of crypto transactions on various tax forms.

How Crypto Tax Calculators Track Your Transactions

Modern crypto tax calculators employ multiple integration methods to automatically import transaction data from exchanges, wallets, and blockchain networks. Understanding these tracking mechanisms helps you ensure comprehensive tax reporting.

Exchange API Integrations

The most common data source involves connecting directly to cryptocurrency exchanges through Application Programming Interface (API) connections. When you authorize the tax software to read your exchange data, the API pulls your complete transaction history including trades, deposits, withdrawals, and historical price data at the time of each transaction. Major exchanges including Coinbase, Binance, Kraken, Gemini, and hundreds of others integrate with leading tax platforms.

API connections provide several advantages over manual entry. They capture every transaction automatically, including small trades you might forget to record. They import precise timestamps, which matter significantly for long-term versus short-term capital gains calculations. They also pull historical price data, eliminating the need to research what Bitcoin or Ethereum was worth on a specific date two years ago.

Blockchain Wallet Connections

Beyond exchange data, many calculators support direct blockchain wallet connections. These integrations read on-chain transactions from your personal wallets, capturing transfers between wallets, transactions to decentralized exchanges, and interactions with smart contracts. This becomes particularly important for DeFi participants who may never touch centralized exchanges yet still have substantial transaction histories.

Manual Transaction Entry

No system captures everything perfectly. Airdrops, token forks, mining rewards, and transactions from defunct exchanges may require manual entry. Quality tax calculators provide intuitive forms for adding these transactions, including tools to look up historical cryptocurrency prices on specific dates.

The Calculation Methods: FIFO, LIFO, and Specific Identification

Understanding calculation methods proves crucial because they directly determine your tax liability. Crypto tax calculators typically support multiple approaches, allowing you to compare outcomes.

First-In-First-Out (FIFO)

FIFO represents the default method most brokers and tax software apply. When you sell cryptocurrency, this method assumes you sell your oldest holdings first. This creates a straightforward audit trail but may result in higher taxes during bull markets when early purchases carried substantially lower costs.

For example, imagine you purchased 1 Bitcoin at $20,000 in 2020, another at $40,000 in 2021, and a third at $60,000 in 2022. If you sell 1 Bitcoin in 2024 when the price reaches $70,000, FIFO assumes you sold the $20,000 purchase first, resulting in a $50,000 capital gain. However, if you sold the $60,000 purchase instead, your gain would only be $10,000.

Last-In-First-Out (LIFO)

LIFO reverses this assumption, selling your most recently acquired assets first. This often produces lower capital gains in rising markets because you sell assets purchased at higher prices first, minimizing profits. However, LIFO requires more detailed record-keeping and may face IRS scrutiny if not properly documented.

Specific Identification

This method allows you to identify exactly which units you’re selling, providing maximum control over your tax outcome. You might deliberately sell specific lots with the highest cost basis to minimize gains or harvest losses. Specific Identification requires maintaining detailed records of each individual purchase and requires explicit identification at the time of sale.

| Method | Best For | Potential Drawback |

|---|---|---|

| FIFO | Simple record-keeping, long-term holding | Higher taxes in bull markets |

| LIFO | Active trading, rising prices | Complex tracking, audit risk |

| Specific ID | Tax optimization, loss harvesting | Requires meticulous records |

The IRS generally accepts any consistent method, though you cannot switch between methods without IRS approval or clear documentation of a new accounting method. Most tax professionals recommend FIFO as the safest approach unless you have specific tax optimization strategies.

Step-by-Step: Using a Crypto Tax Calculator

Understanding the practical workflow helps you maximize the tool’s effectiveness while ensuring accurate reporting.

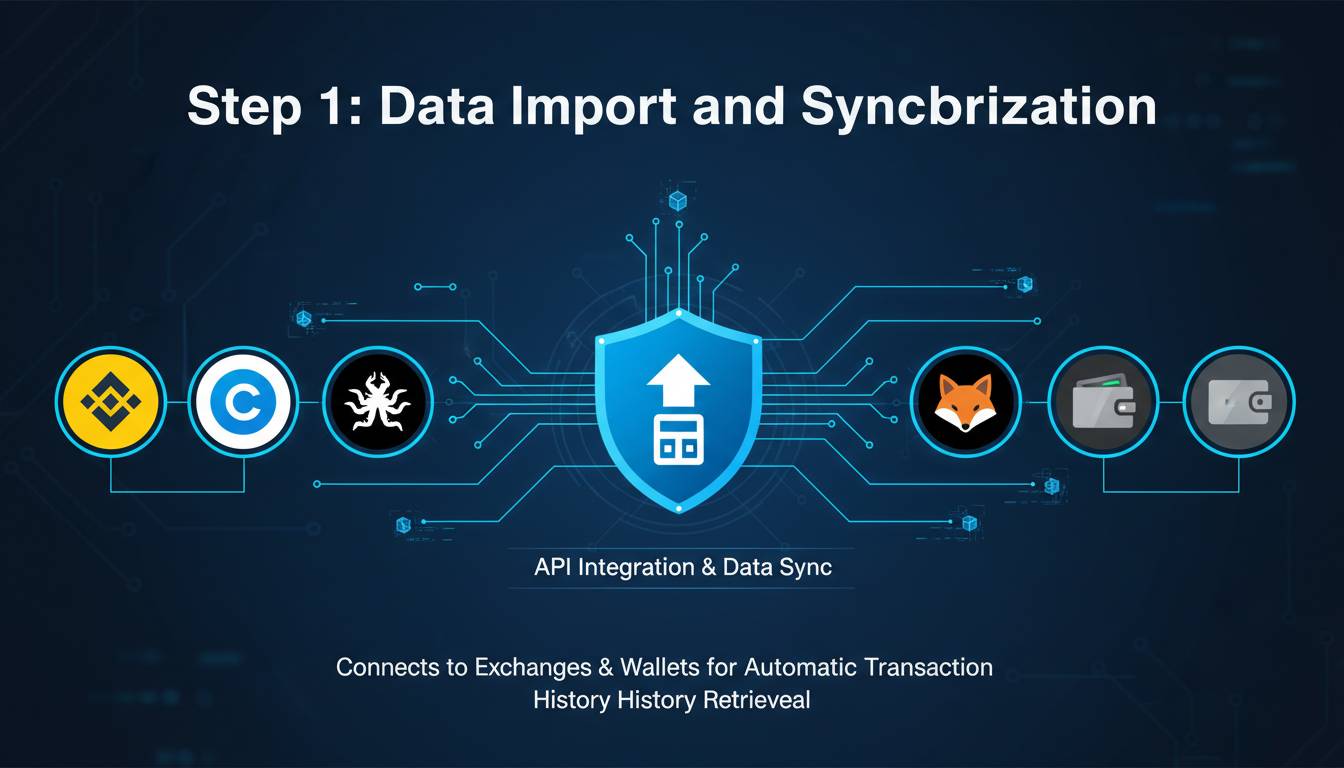

Step 1: Account Setup and Exchange Connections

Begin by creating an account with your chosen crypto tax software. Most platforms offer free tiers for simple portfolios with limited transactions, while complex portfolios require paid plans. Once registered, navigate to the connections or integrations section to link your exchange accounts. The software will display a list of supported exchanges with authorization buttons. After clicking to connect, you’ll be redirected to the exchange to authorize read-only API access.

Step 2: Transaction Import and Review

After connections establish, the software pulls your transaction history. Review the imported transactions carefully, checking for duplicates or missing entries. Most platforms automatically categorize transactions—trades, transfers, deposits, withdrawals—but you should verify these categorizations. Incorrect categorization directly impacts your tax calculation.

Step 3: Addressing Gaps and Missing Data

No automated import is perfect. Review the “missing” or “unmatched” transactions section that most platforms provide. You may need to manually add transactions the system couldn’t reconcile, such as transactions from unsupported exchanges, off-chain transfers, or historical data from platforms no longer operating.

Step 4: Selecting Your Calculation Method

Choose your preferred cost basis calculation method. Consider consulting a tax professional to determine which approach suits your situation. Many platforms allow different methods for different assets, providing flexibility to optimize your overall tax position.

Step 5: Reviewing Tax-Loss Harvesting Opportunities

Quality tax calculators highlight positions with unrealized losses and opportunities for tax-loss harvesting. This involves selling assets at a loss to offset capital gains elsewhere in your portfolio. However, be aware of the wash-sale rule, which prevents claiming losses if you repurchase the same or substantially identical asset within 30 days.

Step 6: Generating Reports

Once satisfied with your data, generate the required tax reports. Most platforms produce Form 8949-ready reports showing each transaction’s cost basis, proceeds, gain or loss, and holding period. You can also generate Schedule D summaries and export data for your tax professional.

Common Features of Professional Crypto Tax Software

Beyond basic transaction tracking, professional crypto tax platforms offer features addressing complex tax scenarios.

DeFi and Staking Support

Decentralized finance transactions create unique tax challenges. Staking rewards constitute taxable income at fair market value when received, while liquidity provision generates both taxable income and potential capital gains upon removal. Professional software tracks these complex transactions, including impermanent loss calculations for liquidity providers.

NFT Transaction Tracking

Non-fungible token transactions have exploded in popularity, yet tax treatment remains somewhat unclear. Professional calculators now support NFT transactions, treating purchases and sales similarly to other crypto assets while providing fields for metadata relevant to art and collectible transactions.

Multi-Currency and Cross-Border Capabilities

Investors holding cryptocurrency across international exchanges face additional complexity. Tax calculators with multi-currency support automatically convert foreign transactions to USD using appropriate exchange rates, simplifying reporting for both US persons with international accounts and non-US persons with US tax obligations.

Audit Trail Documentation

Quality platforms maintain comprehensive audit trails showing exactly how they calculated each gain or loss. This documentation proves invaluable if the IRS questions your returns, providing evidence of good-faith compliance efforts.

Crypto Tax Rules and Regulations in the United States

The regulatory landscape for cryptocurrency taxation continues developing, with recent years bringing increased clarity and enforcement focus.

Current Reporting Requirements

As of the most recent tax years, the IRS requires reporting cryptocurrency transactions on Form 8949 (Sales and Other Dispositions of Capital Assets) and Schedule D (Capital Gains and Losses). If you receive cryptocurrency payments exceeding $600 annually from an employer or client paying via crypto, you should receive Form W-2 or 1099 reporting this income.

The Infrastructure Investment and Jobs Act passed in 2021 expanded reporting requirements further, requiring brokers—including certain crypto exchanges—to report transactions to both the IRS and taxpayers starting in 2026 for the 2025 tax year.

Capital Gains Treatment

Cryptocurrency holdings are categorized as capital assets, meaning gains and losses receive capital gains treatment. Assets held for one year or less generate short-term capital gains taxed at your ordinary income tax rate. Those held longer qualify for long-term capital gains rates of 0%, 15%, or 20% depending on your income level.

Income Events

Not all cryptocurrency transactions generate capital gains. Receiving cryptocurrency as payment for goods or services, mining rewards, staking rewards, airdropped tokens, and hard fork proceeds all constitute ordinary income at the fair market value received. This income is taxable in the year received, regardless of whether you subsequently sell the assets.

Record-Keeping Requirements

The IRS requires taxpayers to maintain records showing the basis in cryptocurrency acquired, the date acquired, and the date sold or disposed of. Crypto tax calculators can satisfy this requirement, but you should maintain backups and ensure the software retains historical data accessible for audit purposes.

Frequently Asked Questions

How do I calculate my crypto taxes manually?

Manual calculation requires tracking every transaction’s cost basis and sale price, determining holding periods for long-term versus short-term treatment, and applying the appropriate tax rates. For each sale, subtract your cost basis (including fees) from your sale proceeds to calculate gain or loss. This becomes exponentially difficult with multiple transactions, making software strongly advisable for portfolios beyond a few transactions.

Do I have to pay taxes on cryptocurrency if I don’t sell?

Simply holding cryptocurrency does not trigger a taxable event. The IRS only taxes disposals, which include sales, trades, spending crypto for purchases, and certain conversions. However, receiving new cryptocurrency through mining, staking, airdrops, or hard forks constitutes taxable income at fair market value even if you don’t sell.

What happens if I don’t report my crypto transactions?

Failure to report cryptocurrency transactions can result in IRS audits, penalties of up to 75% of the unpaid tax, and potential criminal prosecution for willful evasion. The IRS has significantly increased enforcement focus on cryptocurrency, including sending letters to thousands of taxpayers potentially failing to report crypto transactions.

Can I use my exchange’s transaction history for tax purposes?

Exchange transaction histories provide useful data but may not satisfy IRS requirements alone. Records should include your specific cost basis (which exchanges often don’t track across wallets), complete transaction details, and documentation supporting your calculation method. Crypto tax software aggregates this information and adds the necessary calculations and reporting formats.

How does the IRS know about my cryptocurrency transactions?

The IRS obtains cryptocurrency transaction information through multiple channels. Exchanges report certain transactions to the IRS, and beginning in 2026, expanded broker reporting will significantly increase the information available. Additionally, the IRS uses blockchain analysis companies to identify wallet addresses and may match cryptocurrency holdings against information returns from employers and clients paying in crypto.

Conclusion

Crypto tax calculators transform an overwhelming compliance burden into a manageable process. By automatically importing transactions, calculating cost basis using your chosen method, and generating IRS-ready reports, these tools protect you from calculation errors that could trigger audits or penalties.

The key to successful tax compliance lies in consistent record-keeping throughout the year rather than scrambling at tax time. Connect your exchanges and wallets to your chosen tax software, review transactions regularly, and address any gaps promptly. Consider consulting with a tax professional experienced in cryptocurrency to ensure you’re maximizing legitimate tax strategies while remaining compliant with evolving regulations.

As cryptocurrency adoption grows and regulatory scrutiny intensifies, proper tax documentation will only grow more important. Investing time in understanding how these calculators work—and using them consistently—protects your financial wellbeing and ensures you’re prepared regardless of enforcement developments.