219Views 0Comments

What Are Index Funds? A Simple Guide to Building Wealth

Index funds have transformed how millions of Americans invest for retirement, college, and long-term wealth building. These investment vehicles offer a simple way to own pieces of hundreds or thousands of companies with a single purchase, making them particularly attractive for beginners and experienced investors alike. Understanding how index funds work can help you make informed decisions about growing your money while minimizing fees and complexity.

Understanding Index Funds: The Basics

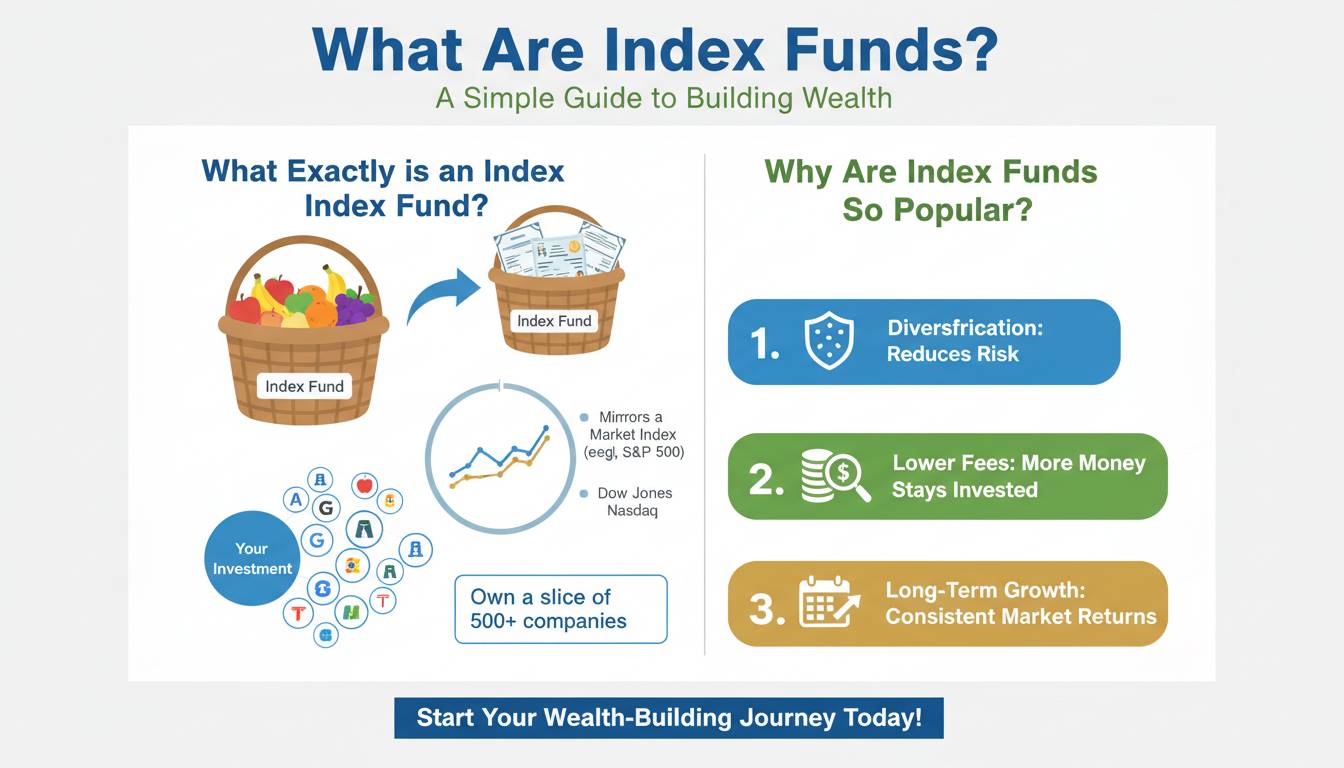

An index fund is a type of mutual fund or exchange-traded fund (ETF) designed to track a specific financial market index, such as the S&P 500, NASDAQ-100, or Wilshire 5000. Rather than trying to beat the market through active stock picking, index funds aim to match the performance of their chosen index by holding the same securities in similar proportions.

The concept originated in the 1970s when Vanguard founder John Bogle introduced the first retail index fund for individual investors. Before this innovation, index investing was primarily reserved for institutional investors due to high transaction costs and complexity. Bogle’s insight was remarkably simple: most actively managed funds fail to outperform the market after fees, so why not simply own the entire market at a low cost?

When you invest in an index fund, your money gets pooled together with other investors’ money. The fund manager then uses this pool to purchase small portions of every company included in the target index. If the index contains 500 companies, your investment automatically includes all 500, providing instant diversification that would be impractical to achieve through individual stock purchases.

How Index Funds Work: The Mechanics

The operation of index funds revolves around a straightforward principle: passive management with minimal human intervention. Unlike actively managed funds where portfolio managers constantly buy and sell stocks trying to outperform the market, index funds follow a “buy and hold” approach that mirrors the index’s composition.

The Process Works Like This:

First, the fund provider selects an index to track, such as the S&P 500, which includes 500 of the largest publicly traded U.S. companies. The fund then purchases shares in each company within that index, adjusting the holdings quarterly when the index itself rebalances. When companies are added to or removed from the underlying index, the fund automatically adjusts its holdings to match.

This passive approach dramatically reduces operating costs. Active fund managers employ teams of analysts, pay for research, and execute frequent trades—all of which generate fees. Index funds require far less human intervention, resulting in significantly lower expense ratios. According to the Investment Company Institute, the average actively managed equity mutual fund charges 0.71% annually, while the average index equity mutual fund charges just 0.06%—a difference that compounds substantially over time.

Your shares in an index fund represent proportional ownership in all the underlying securities. If Apple comprises 7% of the S&P 500, your index fund holding will include approximately 7% exposure to Apple. As companies in the index grow or shrink in market value, the fund’s composition automatically adjusts to maintain proper weighting.

Types of Index Funds

Index funds come in several varieties, each tracking different segments of the financial markets. Understanding these categories helps you choose the right mix for your investment goals.

| Index Fund Type | What It Tracks | Examples | Best For |

|---|---|---|---|

| U.S. Large-Cap | 500 largest U.S. companies | S&P 500 Index funds | General market exposure |

| U.S. Total Market | All U.S. publicly traded companies | Total Stock Market funds | Broader diversification |

| International | Non-U.S. companies globally | MSCI EAFE, MSCI World | Geographic diversification |

| Bond Index | Government and corporate bonds | Aggregate Bond Index | Income and stability |

| Sector-Specific | Single industry segments | Technology, Healthcare funds | Targeted exposure |

Stock Index Funds form the largest category and include large-cap funds tracking the S&P 500, total market funds covering the entire U.S. stock universe, and international funds providing exposure to foreign markets. Many investors build core portfolios using one or two broad stock index funds.

Bond Index Funds offer fixed-income exposure, tracking indexes of government securities, corporate bonds, or municipal bonds. These funds generally provide lower returns than stock funds but offer stability and regular income through interest payments.

International Index Funds have gained popularity as investors seek geographic diversification. These funds track foreign stock markets, ranging from developed countries in Europe and Asia to emerging markets with higher growth potential but greater volatility.

Benefits of Index Fund Investing

The advantages of index funds extend far beyond low costs, though that remains a primary selling point. Understanding the full range of benefits helps explain why index funds have become the preferred vehicle for retirement accounts and long-term investment portfolios.

Instant Diversification

Rather than researching and purchasing individual stocks—which requires significant time, knowledge, and capital—you gain exposure to hundreds or thousands of companies instantly. This diversification protects against any single company performing poorly. If one company in the index collapses, its minimal weighting means your overall portfolio barely notices.

Research from Dartmouth professor Kenneth French demonstrates that diversification reduces portfolio volatility without sacrificing expected returns—a mathematical advantage unavailable through concentrated stock picking.

Lower Costs Mean Higher Returns

The math of fees powerfully demonstrates why index funds often outperform actively managed counterparts over long periods. Consider an investor putting $10,000 into a fund earning 7% annually over 30 years. At a 0.06% expense ratio (typical for index funds), you’d pay approximately $1,800 in fees total. At a 0.71% expense ratio (typical for active funds), fees would reach approximately $21,200—nearly 12 times higher.

That $19,400 difference represents money leaving your portfolio and going to fund managers. Over decades, this fee drag significantly impacts your final balance, making low-cost index funds particularly valuable for long-term investors.

Tax Efficiency

Index funds generate fewer taxable events than actively managed funds because they rarely buy and sell securities within the portfolio. When managers actively trade stocks, they trigger capital gains taxes for shareholders. The buy-and-hold nature of index funds means fewer realized gains, resulting in more tax-efficient returns, especially in taxable brokerage accounts.

Time Savings and Simplicity

Active investing requires constant attention to market conditions, company news, and economic trends. Index funds eliminate this burden, allowing you to invest consistently without monitoring individual holdings. This simplicity makes index funds particularly appealing for busy professionals, new investors, or anyone preferring a set-it-and-forget-it approach.

Common Index Fund Mistakes to Avoid

While index funds offer remarkable simplicity, investors still encounter pitfalls that can undermine their returns. Understanding these common mistakes helps you navigate around them.

Over-Diversifying Into Confusion

Some investors buy dozens of different index funds, believing more funds equals better diversification. In reality, significant overlap exists between many index funds. Holding five different S&P 500 funds provides essentially the same exposure as holding one. Focus on a few broad funds covering different asset classes rather than accumulating overlapping holdings.

Ignoring Expense Ratios

While the difference between 0.06% and 0.15% seems trivial in isolation, the long-term impact proves substantial. Always compare expense ratios when selecting index funds, preferring those with the lowest costs within your chosen category.

Chasing Past Performance

The nature of index funds means their performance directly tracks the underlying index—no manager can “outperform” to generate exceptional results. Some index funds occasionally appear to “beat” their benchmark due to slight methodological differences, but this rarely persists. Focus on costs and broad market exposure rather than short-term performance chasing.

Neglecting Rebalancing

While index funds automatically rebalance when their underlying index changes, your overall portfolio allocation requires manual attention. If stocks soar while bonds stagnate, your allocation drifts from your target mix. Annual rebalancing ensures your risk level remains consistent with your investment policy.

How to Start Investing in Index Funds

Beginning your index fund journey requires only a few practical steps, though the specifics depend on your individual circumstances and preferences.

Step 1: Open an Investment Account

You’ll need a brokerage account to purchase index funds. Options include traditional brokerage accounts, Roth IRAs, or 401(k) plans through your employer. For long-term retirement savings, tax-advantaged accounts generally provide the best value due to their tax benefits.

Step 2: Determine Your Asset Allocation

Your ideal allocation depends on factors including your age, risk tolerance, investment timeline, and goals. A common guideline suggests holding your age in bonds (or subtracting your age from 100 for a more aggressive approach), though this formula has faced criticism in recent years. Younger investors with long time horizons typically benefit from higher stock allocations given their ability to recover from market downturns.

Step 3: Select Your Index Funds

Choose low-cost index funds matching your target allocation. Look for funds with expense ratios below 0.20% and adequate assets under management (generally above $1 billion, indicating market acceptance and stability). Popular options include:

- Total Stock Market Index Funds: Provide exposure to the entire U.S. stock market

- S&P 500 Index Funds: Track the 500 largest U.S. companies

- Total Bond Market Index Funds: Offer broad fixed-income exposure

- International Stock Index Funds: Provide non-U.S. market exposure

Step 4: Invest Regularly Through Dollar-Cost Averaging

Rather than attempting market timing—which consistently proves futile—evenly distribute your investments over time through dollar-cost averaging. This approach involves investing fixed amounts at regular intervals regardless of market conditions, automatically buying more shares when prices drop and fewer when prices rise.

Index Funds vs. ETFs: Understanding the Differences

While often discussed interchangeably, index funds and exchange-traded funds (ETFs) possess distinct characteristics worth understanding.

| Feature | Index Mutual Funds | ETFs |

|---|---|---|

| Trading | End-of-day pricing | Throughout trading day |

| Minimum Investment | Often $3,000+ | Share price (often under $100) |

| Tax Efficiency | Good | Slightly better |

| Expense Ratios | Very low | Very low |

| Automatic Investing | Often available | Limited availability |

Both vehicles can track identical indexes and offer similarly low costs. The choice often comes down to personal preference and account type. Index mutual funds typically work better for regular contributions through automatic investment plans, while ETFs offer flexibility for investors trading smaller amounts or preferring intraday pricing.

The Future of Index Fund Investing

Index fund investing continues evolving as the industry responds to changing investor needs and technological developments. Several trends shape the future landscape.

Smart beta strategies have emerged, offering index funds that incorporate factors like value, momentum, or low volatility rather than pure market-cap weighting. These approaches aim to capture systematic premiums without full active management.

Environmental, social, and governance (ESG) index funds have grown substantially, allowing investors to align portfolios with values while maintaining broad market exposure. These funds screen out certain industries or prioritize companies meeting specific sustainability criteria.

The trend toward ultra-low-cost investing continues, with several providers now offering commission-free trading and near-zero expense ratios. This compression forces traditional active managers to compete on fees or risk continued outflows to passive vehicles.

Frequently Asked Questions

What is the minimum amount needed to start investing in index funds?

The minimum investment varies by fund but has decreased significantly over time. Many index mutual funds now accept initial investments of $1 or $3,000, while ETFs can be purchased for the price of a single share—often under $100. Some brokerage platforms offer fractional shares, allowing you to invest any dollar amount in any fund.

Are index funds safe during market downturns?

Index funds are subject to market downturns since they hold securities that decline in value during bear markets. However, their diversification provides protection against individual company failures, and historically, markets have recovered from every downturn. Index funds designed for long-term goals should not be sold during temporary declines, as staying invested through recovery periods has historically produced positive returns.

How do I choose the right index fund for my retirement?

Select low-cost index funds matching your target asset allocation. For retirement, a three-fund portfolio combining U.S. stock index funds, international stock index funds, and bond index funds provides broad diversification. Choose funds with expense ratios below 0.20% and maintain your allocation through annual rebalancing.

Can I lose all my money in index funds?

While index funds can lose significant value during market crashes, total loss is extremely unlikely because index funds hold diverse securities across many companies. Even in extreme scenarios like the Great Depression or 2008 financial crisis, broad market indexes eventually recovered. Total loss would require every company in the index becoming worthless simultaneously—an event unlikely in a functioning economy.

How often should I contribute to my index fund investments?

Consistent monthly contributions through automatic investing represent the ideal approach for most investors. This dollar-cost averaging strategy reduces the impact of market volatility by buying more shares when prices drop. Set up automatic contributions aligned with your pay schedule, treating savings as a non-negotiable expense.

Do index funds pay dividends?

Yes, most stock index funds pay dividends received from the underlying companies. These dividends get distributed to fund shareholders either quarterly or annually, depending on the fund. You can reinvest dividends automatically through dividend reinvestment plans (DRIPs) to accelerate compounding.

Conclusion

Index funds represent one of the most powerful wealth-building tools available to individual investors. By providing broad market exposure, near-zero costs, tax efficiency, and remarkable simplicity, they level the playing field against expensive actively managed alternatives. Whether you’re saving for retirement, building an emergency fund, or planning for other long-term goals, index funds offer a proven strategy that works regardless of market conditions.

The beauty of index fund investing lies in its predictability: you won’t beat the market dramatically, but you won’t underperform it significantly either. Over decades, this consistency—when combined with regular contributions and patient holding—produces substantial wealth accumulation. For most investors seeking financial security, index funds provide the most reliable path forward without requiring financial expertise or constant attention to market movements.

Start by opening an account, select low-cost funds matching your goals, and commit to regular contributions. The compound growth over time will work silently in your favor, turning modest savings into meaningful wealth.