102Views 0Comments

How to Calculate Compound Interest for Savings – Easy Guide

Compound interest is often called the most powerful force in finance, and for good reason. When you deposit money in a savings account, compound interest works quietly in the background, turning your initial balance into something significantly larger over time. Understanding how to calculate compound interest for savings empowers you to make smarter financial decisions, compare account offers accurately, and project how much your money will grow.

The core compound interest formula is: A = P(1 + r/n)^(nt)

In plain English: your final amount equals your principal multiplied by one plus your annual interest rate divided by the number of compounding periods, all raised to the power of the number of compounding periods multiplied by time. While this looks complex, the calculation becomes straightforward once you break it into steps—and you don’t need advanced math skills to master it.

This guide walks you through everything from the basic formula to real-world examples, helping you calculate compound interest for any savings scenario you encounter.

What Is Compound Interest and Why It Matters

Compound interest differs fundamentally from simple interest. With simple interest, you earn returns only on your original principal. With compound interest, you earn returns on your principal plus the accumulated interest from previous periods. This creates a snowball effect where your money grows exponentially rather than linearly.

Albert Einstein reportedly called compound interest the “eighth wonder of the world,” and while the attribution is uncertain, the sentiment captures its transformative power. Consider this: if you deposit $10,000 in an account earning 5% annual interest, you’d have $12,500 after five years with simple interest—but with annual compounding, you’d have $12,763. The difference seems small initially, but over decades, the gap becomes dramatic.

The Math Behind Compound Growth

| Initial Deposit | 5% Annual Return | 10 Years | 20 Years | 30 Years |

|---|---|---|---|---|

| $1,000 | Compound | $1,629 | $2,653 | $4,322 |

| $1,000 | Simple | $1,500 | $2,000 | $2,500 |

| $5,000 | Compound | $8,144 | $13,266 | $21,611 |

| $5,000 | Simple | $7,500 | $10,000 | $12,500 |

| $10,000 | Compound | $16,289 | $26,533 | $43,219 |

The Federal Reserve’s Survey of Consumer Finances consistently shows that savings account ownership correlates strongly with wealth accumulation, particularly for households that maintain accounts over extended periods. Compound interest rewards patience more than aggressive investment strategies, making it accessible to anyone with a savings account.

The Compound Interest Formula Explained

Understanding each variable in the formula A = P(1 + r/n)^(nt) unlocks the ability to calculate compound interest for any scenario:

- A = The future value of your investment (what you’ll have at the end)

- P = The principal (your initial deposit)

- r = Annual interest rate (expressed as a decimal, so 5% becomes 0.05)

- n = Number of times interest compounds per year

- t = Number of years

The exponent (nt) represents total compounding periods. When interest compounds more frequently—monthly instead of annually, for example—you earn interest on interest more often, resulting in greater overall returns.

Common Compounding Frequencies

| Compounding Period | n Value | How Often Interest Is Added |

|---|---|---|

| Annually | 1 | Once per year |

| Semi-annually | 2 | Twice per year |

| Quarterly | 4 | Four times per year |

| Monthly | 12 | Twelve times per year |

| Daily | 365 | Every day |

Most savings accounts compound monthly, though some high-yield accounts compound daily. The difference matters: $10,000 at 4% APY compounds to $14,859 after 10 years with monthly compounding, but $14,921 with daily compounding—a $62 difference that scales up with larger balances.

Step-by-Step: How to Calculate Compound Interest for Your Savings

Step 1: Gather Your Numbers

Before calculating, collect four pieces of information:

- Principal (P): How much you’re depositing initially

- Annual Interest Rate (r): The stated APY or interest rate

- Compounding Frequency (n): How often interest is calculated and added

- Time Period (t): How long you’ll keep money in the account

Your savings account documents or online banking portal typically list the APY, which already accounts for compounding. If you only see the nominal interest rate, check whether compounding is monthly, daily, or another frequency.

Step 2: Convert Percentages to Decimals

Divide the interest rate by 100. A 5% interest rate becomes 0.05 in the formula. This conversion is essential—using 5 instead of 0.05 would produce an answer 100 times too large.

Step 3: Apply the Formula

Let’s walk through a complete example:

Scenario: You deposit $5,000 in a savings account with 4% APY, compounded monthly, for 5 years.

- P = $5,000

- r = 0.04

- n = 12 (monthly compounding)

- t = 5

Calculation: A = 5000(1 + 0.04/12)^(12×5)

First, divide the rate by compounding frequency: 0.04/12 = 0.003333

Add 1: 1.003333

Calculate the exponent: 12 × 5 = 60

Raise to the power: 1.003333^60 = 1.221

Multiply by principal: 5000 × 1.221 = $6,105

After five years, your $5,000 has grown to $6,105—earning $1,105 in interest. With simple interest at the same rate, you’d have only $6,000.

Step 4: Use Calculators or Spreadsheets

Manual calculations work for simple scenarios, but spreadsheet software or online calculators handle complex situations more efficiently. Excel’s =FV(rate/n, n*t, 0, -principal) function calculates future value instantly. Online compound interest calculators let you adjust variables and see results instantly, useful for comparing different account options.

Real-World Examples: Compound Interest in Action

Example 1: Emergency Fund Growth

Sarah opens an emergency fund with $3,000 and contributes $200 monthly. Her account earns 3.5% APY, compounded monthly. After five years, her balance reaches approximately $16,047—more than double her total contributions of $15,000. The $1,047 difference represents “free money” from compound interest, incentivizing her to maintain the account rather than keeping cash in a non-interest-bearing checking account.

Example 2: Long-Term Savings Goal

Marcus wants to save $50,000 for a house down payment in 10 years. Using a compound interest calculator with a 4.5% APY savings account, he discovers he needs to deposit approximately $334 monthly to reach his goal. Without compound interest working in his favor, he’d need to save the full $50,000 over 10 years ($500 monthly), meaning compound interest effectively contributes nearly $10,000 toward his goal.

Example 3: Comparing Account Options

When comparing savings accounts, the APY matters more than the nominal interest rate because it reflects actual yearly earnings after compounding.

| Account Type | Nominal Rate | APY | $10,000 after 5 years |

|---|---|---|---|

| Traditional Savings | 0.01% | 0.01% | $10,005 |

| Online High-Yield Savings | 4.50% | 4.50% | $12,461 |

| Money Market Account | 4.25% | 4.35% | $12,376 |

| Certificate of Deposit | 4.75% | 4.75% | $12,510 |

The difference between 0.01% APY and 4.50% APY amounts to $2,456 over five years—purely from choosing a better account.

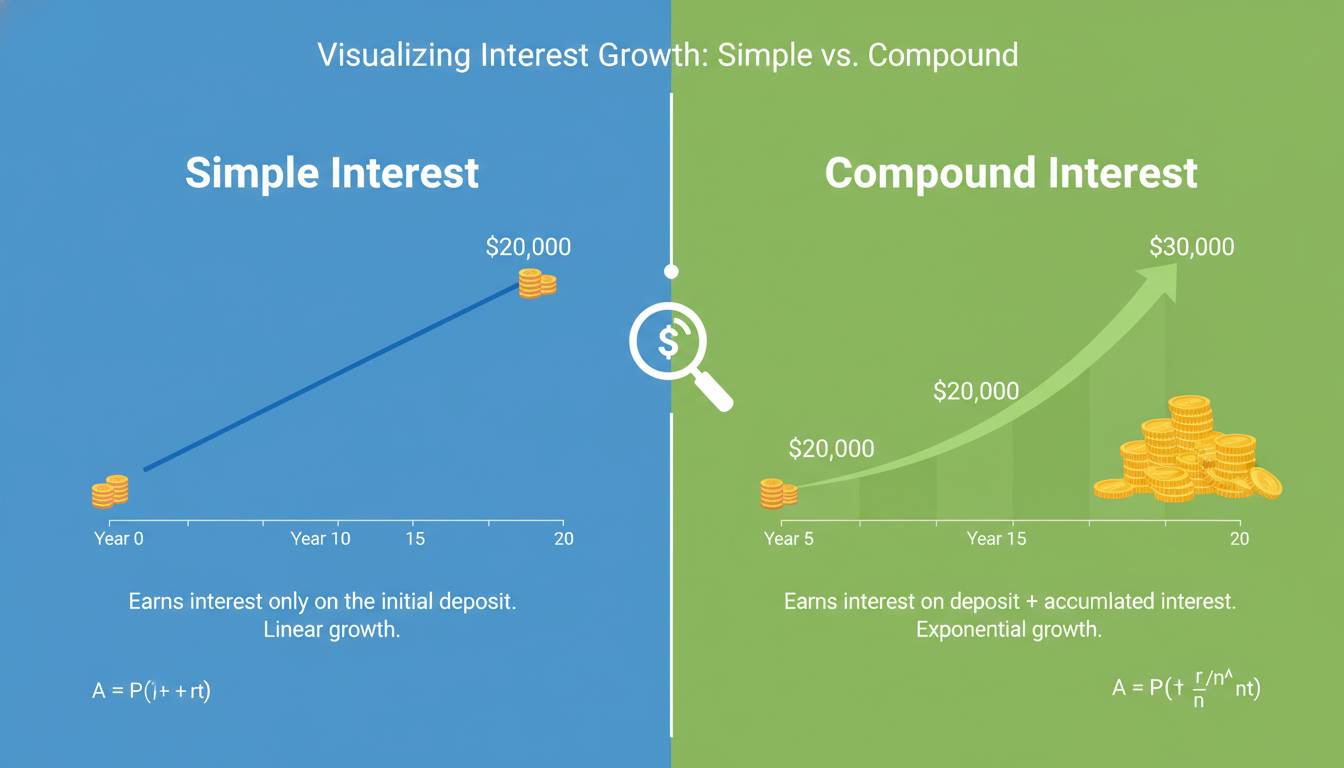

Simple Interest vs. Compound Interest: Understanding the Difference

Simple interest calculates returns based only on the principal balance. The formula is straightforward: Interest = P × r × t. This approach is common with short-term loans, certain bonds, and some promotional savings offers.

Compound interest, by contrast, recalculates the interest-bearing base with each compounding period. This creates exponential growth that accelerates over time.

Direct Comparison: $10,000 at 5% for 20 Years

| Year | Simple Interest Balance | Compound Interest Balance |

|---|---|---|

| 1 | $10,500 | $10,500 |

| 5 | $12,500 | $12,763 |

| 10 | $15,000 | $16,289 |

| 20 | $20,000 | $26,533 |

After 20 years, compound interest generates 33% more returns than simple interest—$26,533 versus $20,000. The gap widens continuously because each year’s interest earns returns on previous years’ accumulated interest.

Most savings accounts use compound interest, but some financial products specify simple interest calculations. Always verify which method applies to understand your actual returns.

Factors That Affect Your Compound Interest Returns

Interest Rate

The interest rate exerts the most significant influence on compound interest outcomes. Even small differences compound substantially over time. A 1% rate increase—from 3% to 4%—generates approximately 35% more interest over 20 years on a $10,000 principal.

Compounding Frequency

More frequent compounding produces higher returns because interest begins earning its own interest sooner. Daily compounding outperforms monthly, which outperforms annually, though the differences diminish at lower interest rates.

| $10,000 at 4% for 10 Years | Final Balance | Total Interest |

|---|---|---|

| Annually | $14,802 | $4,802 |

| Monthly | $14,908 | $4,908 |

| Daily | $14,921 | $4,921 |

The $119 difference between annual and daily compounding seems modest, but on a $100,000 balance, it grows to $1,190.

Time

Time is the most powerful variable in compound interest. The exponential nature means returns accelerate dramatically in later years. Money invested at age 25 will more than quadruple by age 65 at 7% annual returns, while money invested at age 45 will roughly double.

Regular Contributions

Adding regular deposits supercharges compound growth. Each contribution becomes a new principal amount that compounds going forward. Even modest monthly contributions generate substantial long-term wealth through this multiplier effect.

Practical Tips to Maximize Your Savings with Compound Interest

Choose High-Yield Savings Accounts: Traditional banks often offer minimal interest rates around 0.01% to 0.05%. Online banks, credit unions, and money market accounts frequently provide 4% to 5% APY with the same FDIC insurance protection. This single decision can multiply your returns fivefold or more.

Start Early: The difference between starting at age 25 versus age 35 for retirement savings is enormous. Even small amounts invested early outperform larger investments made later due to the extended compounding period.

Make Regular Deposits: Automating monthly contributions ensures consistent principal growth. Even $100 monthly adds $12,000 in principal over ten years, plus compound interest on every deposit.

Reinvest Your Interest: Many savings accounts automatically compound interest back into your balance. However, some accounts offer the option to withdraw interest periodically. Reinvesting rather than withdrawing accelerates compound growth.

Compare APY, Not Just Interest Rates: The Annual Percentage Yield accounts for compounding frequency, making it the accurate figure for comparing true returns. A 4.8% nominal rate with monthly compounding yields less than a 4.7% APY account.

Compound Interest Calculation Methods

Manual Calculation

For those wanting to understand the mechanics, manual calculation using the formula provides clarity:

- Divide annual rate by compounding periods: r/n

- Add 1 to result: 1 + (r/n)

- Multiply periods by years: n × t

- Raise base to calculated exponent: (1 + r/n)^(nt)

- Multiply by principal: P × result

This approach builds understanding and works when you lack access to calculators.

Spreadsheet Formulas

Spreadsheets streamline compound interest calculations:

- Excel/Google Sheets:

=FV(rate/periods, periods*years, payment, -present_value) - Example:

=FV(0.04/12, 12*5, -200, -5000)calculates future value with monthly contributions

Online Calculators

Many financial websites offer compound interest calculators where you input principal, rate, time, and compounding frequency to receive instant results. Bankrate, Investor.gov, and NerdWallet all provide free tools ideal for comparing scenarios.

Frequently Asked Questions

How do I calculate compound interest for monthly savings contributions?

Include your regular contribution as the “pmt” (payment) variable in financial calculators or spreadsheet formulas. The formula becomes A = P(1 + r/n)^(nt) + PMT × [((1 + r/n)^(nt) – 1) / (r/n)]. For example, $5,000 initial deposit plus $200 monthly at 4% APY for 10 years calculates to approximately $34,112 using this extended formula.

What is the difference between APR and APY?

APR (Annual Percentage Rate) represents the nominal yearly interest rate without accounting for compounding. APY (Annual Percentage Yield) includes the effects of compounding within the year, making it the true cost of borrowing or true return on savings. When comparing savings accounts, always use APY.

How often should compound interest be calculated for my savings?

For savings accounts, the compounding frequency is set by the financial institution—you cannot change how often interest compounds. However, you can choose accounts with more favorable compounding schedules. Daily or monthly compounding is standard for high-yield savings accounts, while some certificates of deposit compound semi-annually.

Does compound interest work on any savings account?

Yes, compound interest applies to any account that pays interest on your balance. This includes regular savings accounts, high-yield savings accounts, money market accounts, certificates of deposit, and most other interest-bearing deposit products. Checking accounts typically do not earn interest, though some do.

How long does it take for compound interest to double my money?

Using the Rule of 72, divide 72 by your interest rate to estimate years to double. At 4% APY, money doubles in approximately 18 years (72 ÷ 4 = 18). At 6% APY, it takes about 12 years. This quick mental math helps you understand the power of compound interest without detailed calculations.

Can compound interest work against me?

Yes, compound interest can work against you when borrowing money. Credit cards, loans, and mortgages often use compound interest calculations, meaning unpaid balances grow exponentially. This is why paying more than minimum payments on credit cards saves substantial money over time.

Conclusion

Compound interest represents one of the most accessible wealth-building tools available. Whether you’re saving for an emergency fund, a major purchase, or long-term financial goals, understanding how to calculate compound interest for savings helps you make informed decisions and project realistic growth for your money.

The formula A = P(1 + r/n)^(nt) is your gateway to financial clarity. Master this calculation, and you gain the ability to compare accounts accurately, set realistic savings goals, and understand exactly how your money grows over time.

Remember these key principles: higher interest rates dramatically increase returns, compounding frequency matters, and time is your greatest ally. Starting early—even with modest amounts—leverages compound interest’s exponential power more effectively than waiting to invest larger sums later.

Your next step is simple: calculate your own compound interest using the methods in this guide, then explore high-yield savings options that put this mathematical power to work for your financial future.