134Views 0Comments

How to Create a Budget Spreadsheet for Beginners – Simple Free Guide

Creating a budget spreadsheet is one of the most effective ways to take control of your finances, yet nearly 60% of Americans don’t use a budget at all according to a 2023 CNBC survey. The good news? You don’t need accounting expertise or expensive software to build one. A simple spreadsheet—free and customizable—can help you track income, categorize expenses, and finally understand where your money goes each month.

This guide walks you through creating a functional budget spreadsheet from scratch, whether you prefer Google Sheets, Microsoft Excel, or another platform. You’ll learn what sections to include, how to set up formulas that do the math automatically, and practical strategies to make budgeting actually stick.

Why a Budget Spreadsheet Works Better Than Apps

Before diving into the technical steps, understanding why spreadsheets outperform many budgeting apps makes the effort worthwhile. The average budgeting app costs between $5-$15 monthly, adding up to $180 per year—a cost you can avoid entirely with a spreadsheet you control completely.

Customization represents the biggest advantage. Most apps force you into predetermined categories that may not fit your lifestyle. If you’re a freelancer with irregular income or a parent managing childcare costs, spreadsheet flexibility lets you create categories that actually reflect your life. Research from the National Endowment for Financial Education indicates that people who customize their budgeting tools are 34% more likely to stick with them long-term.

Spreadsheets also provide transparency. When you build something yourself, you understand exactly how calculations work. This knowledge builds financial literacy while preventing the “black box” problem where app algorithms make assumptions you never see.

Finally, spreadsheets transfer easily. Your budget works offline, requires no subscription, and lives in your Google Drive or on your computer. No account closures, no data harvesting, no platform switching hassles.

Essential Components of Any Budget Spreadsheet

Every effective budget spreadsheet contains three core sections: income tracking, expense categorization, and summary calculations. Building these correctly from the start prevents the frustration of retrofitting formulas later.

Income Section

The income section should include columns for income source, expected amount, and actual amount. Common income sources include:

- Primary salary or wages

- Side gig or freelance income

- Self-employment earnings

- Benefits or government payments

- Investment dividends or interest

- Any other regular income

The distinction between “expected” and “actual” columns matters enormously. Expected income represents your plan—what you anticipate earning. Actual income is what hits your account. Comparing these two columns reveals income variability and helps you plan for fluctuations.

For those with variable income, creating a rolling three-month average in a separate cell helps establish a realistic baseline. Add all actual income from the past three months, divide by three, and use this number as your planning figure. This approach prevents the common mistake of budgeting based on a single high-earning month.

Expense Categories

Expense categorization requires balancing detail with simplicity. Too many categories become overwhelming; too few hide important spending patterns. Most beginners succeed with 10-15 categories organized into logical groups.

Fixed Expenses (recurring monthly costs)

- Housing (rent or mortgage)

- Utilities (electricity, gas, water, internet)

- Insurance (health, car, life)

- Loan payments (student loans, car payments)

- Subscriptions and memberships

- Childcare or dependent care

Variable Expenses (amounts that change monthly)

- Groceries and food

- Transportation (gas, public transit, rideshare)

- Dining out and entertainment

- Healthcare and medical

- Personal care (haircuts, toiletries)

- Clothing and accessories

Financial Goals

- Emergency fund contributions

- Retirement savings

- Debt repayment beyond minimums

- Investment contributions

- Savings for large purchases

Creating separate rows for each expense category lets you see exactly where money goes. Grouping related expenses under section headers improves readability without sacrificing detail.

Summary Section

The summary section calculates the numbers that matter: total income, total expenses, and the difference between them. This is where formulas earn their keep.

The basic formula chain works like this:

- Sum all expected income

- Sum all actual income

- Sum all budgeted (planned) expenses

- Sum all actual expenses

- Calculate: Income minus Expenses = Remaining balance

A well-built spreadsheet shows both budget versus actual for every category, plus overall monthly performance. Color-coding (conditional formatting) highlights overspending in red and underspending in green, making problem areas immediately visible.

Step-by-Step: Building Your First Budget Spreadsheet

Now comes the hands-on work. These instructions work in both Google Sheets and Microsoft Excel, with minor differences noted where relevant.

Step 1: Set Up Your Column Headers

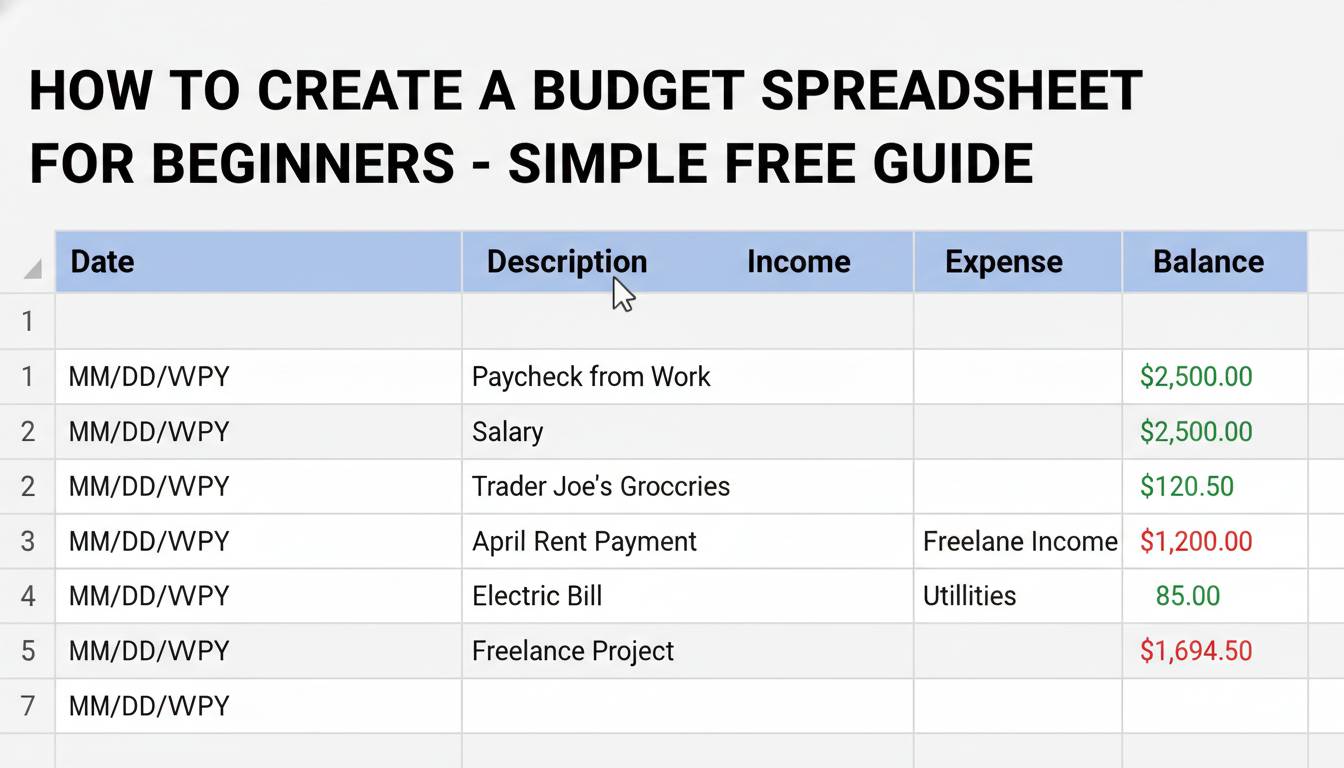

Open a new spreadsheet and create these column headers in row 1:

Income columns: A (Source), B (Expected), C (Actual), D (Difference)

Expense columns: A (Category), B (Budgeted), C (Actual), D (Difference)

For a two-section layout, place income in columns A through D, then add a blank column E, then place expenses in columns F through I. Alternatively, stack income on top and expenses below within a single section. Both approaches work; choose based on visual preference.

Step 2: Enter Your Income Sources

List all income sources in column A, starting in row 2. Enter expected monthly amounts in column B. Leave column C empty for now—you’ll fill this as money arrives.

In a new cell below your income list, create a sum formula: =SUM(B2:B10) where B2:B10 covers all your income cells. This calculates total expected income. Do the same for column C once you start tracking actual amounts.

Step 3: Enter Your Expense Categories

Below your income section, create headers for expenses. List each category in column A, entering budgeted amounts in column B based on your income and goals.

The budgeted amounts should equal your income minus your savings goals. If you earn $4,000 monthly and want to save $400, your total budgeted expenses equal $3,600. Every dollar has a job—assign it to a category rather than leaving it as “miscellaneous.”

Step 4: Add Formulas for Automatic Calculations

The magic of spreadsheets lies in formulas. Set up these essential calculations:

Income total: =SUM(B2:B10)

Expense total: =SUM(B15:B30)

Net income: =SUM(B2:B10)-SUM(B15:B30)

Category variance: =C2-B2 (copied down each row)

The category variance formula shows whether you’re over or under budget in each area. A negative number means you spent less than planned (good for most categories, though some require context). A positive number indicates overspending.

Step 5: Add Conditional Formatting

Select your expense actual amounts and apply conditional formatting rules:

- If value is greater than budgeted → red background

- If value is less than or equal to budgeted → green background

This visual system works faster than reading numbers. When you check your spreadsheet weekly, problem categories immediately catch your eye.

Step 6: Create Monthly Tracking Tabs

Create separate tabs for each month (January, February, etc.) by right-clicking your original sheet tab and choosing “Duplicate” or “Duplicate sheet.” Rename each copy for the corresponding month. This builds a full-year view showing trends over time.

Include a summary tab that pulls key numbers from each monthly tab. This lets you see annual spending patterns, identify seasonal variations, and track progress toward long-term goals.

Advanced Features for Ongoing Budget Management

Once your basic spreadsheet functions reliably, these enhancements add significant value without much additional effort.

Yearly View Tab

Create a separate tab showing monthly totals for each category across the full year. A simple table with months as columns and categories as rows, using SUMIF formulas to pull from your monthly tabs, reveals annual spending patterns that monthly views obscure.

This perspective matters for irregular expenses. Holiday spending, annual subscriptions, and birthday gifts spread unevenly throughout the year. A yearly view shows whether you’re on track even when a single month looks off.

Savings Goal Tracker

Add a section tracking progress toward specific savings goals. Create rows for each goal (emergency fund, vacation, new car, home down payment), showing:

- Target amount

- Current balance

- Monthly contribution

- Projected completion date

The projected completion date uses a simple formula: =(Target-Current)/MonthlyContribution. Watching a goal move from “3 years away” to “18 months away” provides motivation that pure budgeting rarely achieves.

Category Transfer System

When you overspend in one category, allow transfers from others rather than just noting the overspend. Create a “funds moved” column in your expenses section.

The formula: Beginning budget + transfers in – transfers out = adjusted budget. This prevents the common failure mode where one category going over derails the entire budget. Money moves between categories in real life—it should move in your spreadsheet too.

Common Budget Spreadsheet Mistakes to Avoid

Building a spreadsheet introduces several predictable pitfalls. Steering clear of these saves time and frustration.

Mistake #1: Over-complicating categories

Starting with 30+ categories overwhelms most beginners. Begin with 8-10 broad categories. Add detail only after tracking for two or three months reveals the need. You can always split categories later; merging them proves harder.

Mistake #2: Ignoring irregular expenses

Annual subscriptions, car registration fees, and holiday gifts ambush budgets every year. Create a “sinking fund” category that sets aside small amounts monthly for predictable irregular expenses. Divide annual costs by 12 and save that amount monthly.

Mistake #3: Not updating regularly

A budget spreadsheet only works when you use it. Schedule a specific time weekly—Sunday evenings work well for many—to update actual expenses. Waiting until month-end creates data entry nightmares and loses the behavioral benefit of real-time awareness.

Mistake #4: Making it perfect before starting

Perfectionism kills more budgets than overspending. Launch with basic categories and refine over time. Your first spreadsheet should launch within one sitting; detailed optimization comes later.

Free Templates and Resources

You don’t need to build from scratch. Both Google Sheets and Excel offer free budget templates, though customization typically improves results.

Google Sheets template gallery includes several budget options accessible by clicking File > New > From template gallery > Budgets. The “Annual budget” template provides month-by-month tracking with category summaries.

Microsoft Excel’s template collection works similarly, accessible via File > New and searching “budget.” These templates include pre-built formulas and formatting, reducing setup time significantly.

For those wanting step-by-step guidance, the Federal Financial Literacy and Education Commission offers free resources at MyMoney.gov, including budget worksheets specifically designed for beginners.

Conclusion

Creating a budget spreadsheet costs nothing but time and provides value that compounds over months and years. The process teaches financial awareness while the tool itself adapts to your changing circumstances. Whether you use Google Sheets, Excel, or another platform, the core structure remains: income, expenses, and the calculation showing the difference.

Start simply. Track your money for one month using minimal categories. Refine from there. The spreadsheet evolves with your financial literacy, becoming more sophisticated precisely when you’re ready for additional complexity. Your future self—debt-free, saving consistently, financially aware—will thank you for starting today.

The best budget spreadsheet isn’t the most complex or visually impressive. It’s the one you’ll actually use. Build something you’re comfortable opening weekly, and the habits will follow the tool.

Frequently Asked Questions

What is the best free spreadsheet program for budgeting?

Google Sheets and Microsoft Excel both work excellently for budgeting. Google Sheets offers the advantage of free access, automatic cloud saving, and easy sharing with partners. Excel provides more advanced features and is better for complex calculations. Both are available on mobile devices, letting you track expenses on the go.

How do I track expenses in a spreadsheet for beginners?

Create categories in one column, enter your planned budget amounts in the next column, and leave a column for actual spending. Update the “actual” column throughout the month as purchases occur. Use SUM formulas to calculate totals and conditional formatting to highlight overspending categories.

Should I budget zero-based (giving every dollar a job)?

Zero-based budgeting, where income minus expenses equals zero, is highly effective but requires more effort. Beginners might start with a simpler “pay yourself first” approach—setting aside savings automatically, then budgeting the remainder. As comfort grows, transition to zero-based budgeting for complete awareness.

How often should I update my budget spreadsheet?

Weekly updates work best for most people. Updating weekly keeps financial awareness fresh without becoming time-consuming. Set a recurring calendar reminder. Monthly updates are better than nothing but allow problems to compound unnoticed.

What’s the minimum number of expense categories needed?

Ten to fifteen categories provide enough detail without overwhelm. Essential categories include housing, food, transportation, utilities, insurance, healthcare, personal, entertainment, and savings. Add categories only when tracking reveals specific spending patterns needing attention.

How do I handle variable income in a budget spreadsheet?

Use a rolling average of your last three months’ income as your budget baseline. This approach smooths out fluctuations while remaining realistic. Alternatively, budget using your lowest-earning month and treat extra income as “bonus” savings. Both methods prevent overspending during leaner months.