393Views 0Comments

What Is a Robo Advisor? Is It Worth It for Investors?

If you’ve ever wanted professional investment management but balked at the high fees charged by traditional financial advisors, robo advisors have likely appeared on your radar. These digital platforms use algorithms to build and manage investment portfolios automatically, offering a middle ground between hands-off saving and expensive human guidance.

The short answer: Robo advisors are worth it for investors seeking low-cost, automated portfolio management, particularly those with straightforward financial situations. However, they may not suit those with complex tax strategies, significant wealth, or who desire holistic financial planning beyond investment management.

Understanding Robo Advisors: Definition and How They Work

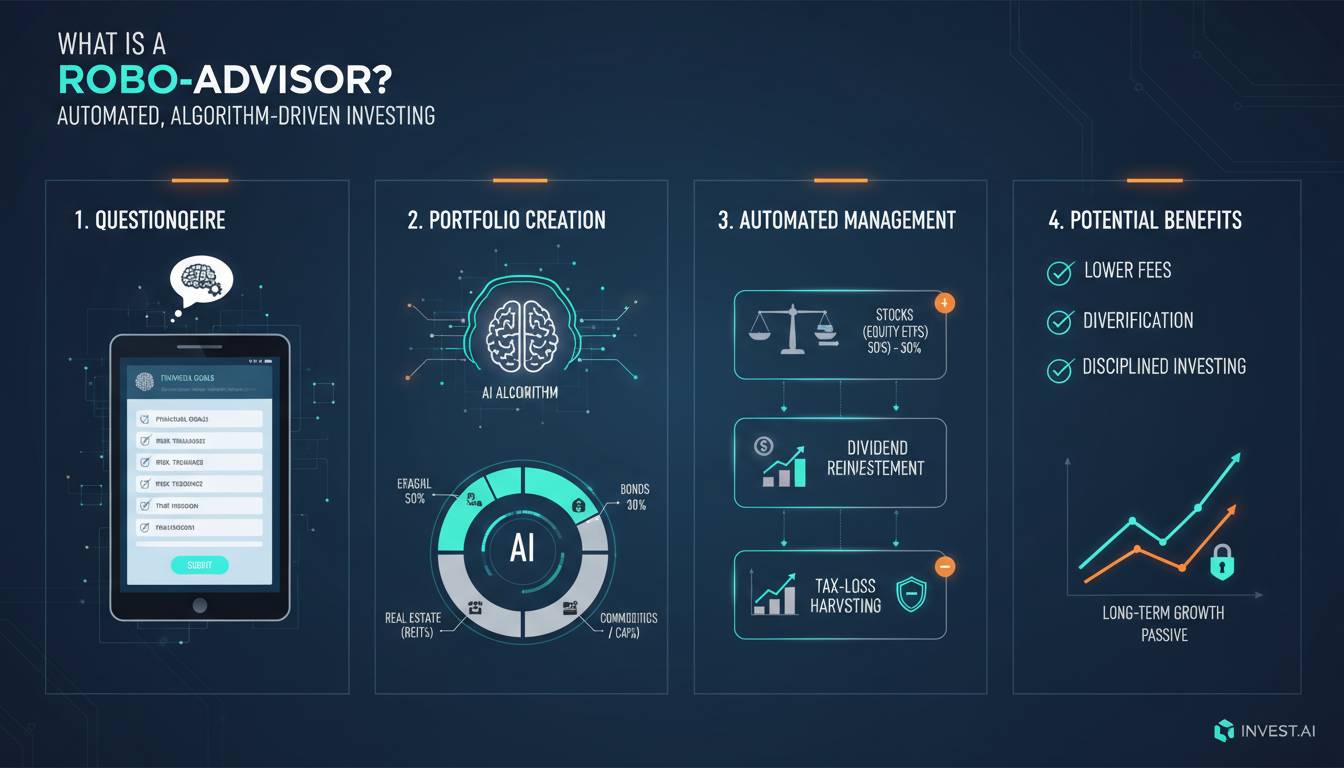

A robo advisor is a digital platform that provides automated, algorithm-driven financial planning services with minimal human intervention. These services include portfolio construction, automatic rebalancing, tax-loss harvesting, and ongoing portfolio management based on your risk tolerance and financial goals.

The Core Technology Behind Robo Advisory Services

Modern robo advisors operate on sophisticated investment frameworks that combine Modern Portfolio Theory (MPT) with behavioral finance principles. When you sign up, the platform typically guides you through a questionnaire assessing your:

- Risk tolerance – Your comfort level with portfolio volatility and potential losses

- Investment time horizon – When you plan to withdraw the funds

- Financial goals – Retirement, buying a home, education funding, or wealth building

- Income stability – Your ability to continue contributing during market downturns

Based on your responses, the algorithm constructs a diversified portfolio primarily using exchange-traded funds (ETFs) spanning various asset classes: domestic stocks, international stocks, bonds, real estate, and sometimes commodities or emerging markets.

The Automated Management Process

Once your portfolio is established, the robo advisor manages it continuously through several automated processes:

Automatic Rebalancing: Markets shift constantly, causing your asset allocation to drift from your target. Robo advisors automatically buy and sell assets to maintain your intended balance—typically quarterly or when allocation drifts beyond a predetermined threshold (often 5%).

Tax-Loss Harvesting: This strategy involves selling investments at a loss to offset capital gains taxes while maintaining your target allocation. Many robo advisors scan your portfolio for these opportunities, potentially saving you thousands in taxes annually.

Dividend Reinvestment: Instead of letting cash from dividends sit idle, robo advisors automatically reinvest distributions to keep your money working continuously.

Types of Robo Advisor Services: Finding the Right Fit

The robo advisory industry has evolved significantly since Betterment launched in 2008, creating distinct service tiers that cater to different investor needs.

Basic Robo Advisors ($0 to $0.25% AUM)

These platforms offer fully automated portfolio management at the lowest cost points. They’re ideal for hands-off investors who want simple, set-it-and-forget-it management.

| Provider | Management Fee | Minimum Investment | Best For |

|---|---|---|---|

| Fidelity Go | 0% to 0.35% | $10 | Fidelity customers |

| Schwab Intelligent Portfolios | 0% | $5 | Bank-style simplicity |

| SoFi Invest | 0% | $1 | Beginners |

| M1 Finance | 0% | $100 | Customization |

Premium Robo Advisors (0.25% to 0.50% AUM)

These hybrid services combine automated management with access to human financial advisors for financial planning questions.

| Provider | Management Fee | Minimum Investment | Key Feature |

|---|---|---|---|

| Betterment | 0.25% to 0.40% | $1 | Premium planning access |

| Wealthfront | 0.25% to 0.40% | $500 | Sophisticated tax strategies |

| Titan Invest | 0.50% | $100 | Active trading options |

| Personal Capital | 0.49% to 0.89% | $25,000 | Human advisor hybrid |

Human-Advisor Hybrid Platforms (0.50% to 1.00% AUM)

For investors seeking more comprehensive financial planning, these platforms provide dedicated human advisors alongside algorithm-driven portfolio management.

| Provider | All-In Fee | Minimum Investment | Included Services |

|---|---|---|---|

| Vanguard Personal Advisor | 0.30% | $50,000 | Holistic financial planning |

| Facet Wealth | 0.80% | $25,000 | Dedicated fiduciary advisor |

| Betterment Premium | 0.40% | $100,000 | Certified financial planner |

Key Benefits and Potential Drawbacks

Understanding the advantages and limitations helps determine whether robo advisors align with your financial situation.

Advantages That Matter

Lower Costs: Robo advisors typically charge 0.25% to 0.50% annually compared to 1% to 1.5% for traditional human advisors. On a $100,000 portfolio, this difference amounts to $500 to $1,000 in annual savings.

Accessibility: Many platforms require minimum investments of just $1 to $500, making professional portfolio management accessible to younger investors or those building wealth gradually.

Discipline Enforcement: Algorithms don’t experience fear during market crashes or greed during bull markets. This removes emotional decision-making that often undermines long-term returns.

Time Efficiency: The automated nature means you spend minutes rather than hours managing investments. For busy professionals, this convenience has significant value.

Tax Efficiency: Tax-loss harvesting and automated dividend reinvestment can enhance after-tax returns, though results vary based on market conditions.

Limitations to Consider

No Comprehensive Planning: Most robo advisors focus narrowly on investment management. They typically don’t address estate planning, insurance needs, tax strategy beyond harvesting, or major life transitions like career changes or divorce.

Limited Customization: Algorithms work within predefined parameters. If you have specific ethical investing preferences, concentrated stock positions, or complex portfolio needs, you may find robo advisor options restrictive.

Technology Risk: Platform failures, cybersecurity breaches, or algorithmic errors can occur. While rare, these events can disrupt portfolio management.

No Human Relationship: When facing major financial decisions, many investors prefer speaking with a knowledgeable human who understands their complete financial picture.

Robo Advisor vs Traditional Financial Advisor: Making the Comparison

The choice between robo advisors and human advisors depends on your financial complexity and personal preferences.

Direct Comparison

| Factor | Robo Advisor | Traditional Advisor |

|---|---|---|

| Average Cost | 0.25% – 0.50% | 1% – 1.5% |

| Minimum Investment | $1 – $50,000 | $100,000 – $1M+ |

| Time Commitment | Minutes annually | Hours annually |

| Human Interaction | Limited or none | Regular meetings |

| Scope | Investments | Full financial plan |

| Customization | Algorithm-constrained | Highly personalized |

| Complexity Handling | Basic | Advanced |

When Robo Advisors Make Sense

Robo advisors excel when your financial situation includes these characteristics:

- Straightforward investments – You have no complex tax situations, business ownership, or significant legacy planning needs

- Cost sensitivity – Fee savings matter significantly given your portfolio size

- Time constraints – You prefer automated management over active portfolio monitoring

- Long-term focus – You’re investing for goals decades away without needing immediate access to funds

- Disciplined approach – You won’t panic-sell during market downturns

When Traditional Advisors Add Value

Human advisors prove worthwhile when your situation involves:

- Complex tax situations – Business owners, executives with stock options, or those with significant unrealized gains

- Estate planning needs – Multi-generational wealth transfer, trust administration

- Major life transitions – Divorce, inheritance, business sale

- Comprehensive planning – Insurance analysis, retirement income strategy, education planning

- Behavioral coaching – You need someone to talk you off the ledge during market volatility

Who Should Consider a Robo Advisor?

Ideal Candidates

Young Investors Building Wealth: Beginning investors often lack the minimum assets required for traditional advisory relationships. Robo advisors provide professional management at price points that won’t consume early-stage returns.

Busy Professionals: Doctors, lawyers, executives, and entrepreneurs who generate significant income but lack time for investment management benefit from automated solutions.

Retirees Seeking Income Strategies: Those already retired or approaching retirement can use robo advisors for efficient drawdown strategies and portfolio maintenance.

Second-Income Investors: Those using investable assets as supplemental income rather than primary wealth accumulation often prefer the hands-off approach.

Who Might Look Elsewhere

High-Net-Worth Individuals: Investors with $1 million or more in investable assets often benefit from comprehensive wealth management services that robo platforms cannot provide.

Complex Financial Situations: Business owners, real estate investors, and those with multiple income streams typically need human expertise for tax optimization and planning.

Investors Who Want Hand-Holding: Some people genuinely prefer regular conversations about their finances and want an advisor available during major decisions.

Top Robo Advisors in the Market: A Closer Look

Best for Beginners: SoFi Invest

SoFi Invest offers completely free automated investing with no minimums, making it ideal for those just starting their investment journey. The platform includes access to human advisors at no additional cost for premium members.

Management Fee: 0% | Minimum: $1 | Key Feature: Free human advisory access

Best for Tax Optimization: Wealthfront

Wealthfront pioneered tax-loss harvesting at scale and offers sophisticated strategies including direct indexing for accounts over $100,000. The platform provides detailed tax impact analysis.

Management Fee: 0.25% | Minimum: $500 | Key Feature: Advanced tax strategies

Best for Comprehensive Planning: Vanguard Personal Advisor Services

Vanguard combines its renowned low-cost investment philosophy with human advisor access, offering holistic financial planning alongside algorithm-driven portfolio management.

Management Fee: 0.30% | Minimum: $50,000 | Key Feature: Human advisors + low fees

Best for Customization: M1 Finance

M1 Finance allows investors to build custom portfolios from thousands of stocks and ETFs while maintaining automated rebalancing—a unique combination of control and automation.

Management Fee: 0% | Minimum: $100 | Key Feature: Custom portfolio building

How to Choose the Right Robo Advisor

Selecting the appropriate platform requires evaluating several factors against your specific needs.

Step 1: Assess Your Requirements

Before comparing platforms, clarify what matters most:

- Budget: Calculate how much you can afford in annual fees

- Minimums: Determine your starting investment amount

- Goals: Identify whether you need investment-only management or broader planning

- Complexity: Consider if your tax situation or financial picture requires human expertise

Step 2: Compare Fee Structures

Look beyond the management fee to understand total costs:

- Advisory fee: The primary ongoing cost

- Expense ratios: The underlying ETF costs (typically 0.03% to 0.15%)

- Transfer fees: Costs for moving accounts

- Trading costs: Some platforms charge for frequent trading

Step 3: Evaluate Features

Consider which features provide meaningful value:

- Tax-loss harvesting: Most beneficial for taxable accounts

- Rebalancing frequency: Quarterly is standard; some offer more frequent adjustment

- Human advisor access: Worth paying for if you want planning support

- Account types: Ensure the platform supports IRAs, 401(k) rollovers, or other accounts you need

Step 4: Test the Experience

Sign up for free trials or low-minimum accounts to experience:

- Onboarding process quality

- Website and mobile app usability

- Customer service responsiveness

- Educational content quality

Frequently Asked Questions

What exactly does a robo advisor do?

A robo advisor is an automated investment platform that creates and manages a diversified portfolio based on your risk tolerance and financial goals. It handles portfolio construction using ETFs, automatically rebalances your holdings as markets shift, implements tax-loss harvesting strategies, and reinvests dividends—all with minimal human intervention.

Are robo advisors safe and trustworthy?

Robo advisors are registered investment advisors subject to SEC regulations, meaning they owe you fiduciary duty. Major platforms carry SIPC protection covering securities up to $500,000. However, no investment is completely risk-free, and you should research each platform’s track record, security measures, and fee structures before committing funds.

Can I lose money with a robo advisor?

Yes, robo advisors invest in securities that fluctuate in value, so you can lose money during market downturns. However, robo advisors typically construct diversified portfolios designed to minimize risk while achieving long-term growth. Your actual risk level depends on your chosen allocation—aggressive portfolios (more stocks) carry higher risk than conservative portfolios (more bonds).

Do robo advisors beat the market?

Most robo advisors do not aim to “beat the market.” Instead, they focus on achieving market-matching returns through diversified index investing while minimizing costs and taxes. This passive approach often outperforms actively managed funds over time, primarily due to lower fees rather than superior returns.

How much money do I need to start with a robo advisor?

Many robo advisors require no minimum investment at all, while others ask for $500 to $50,000. Providers like M1 Finance and SoFi Invest allow you to start with $1 or $100, making professional management accessible to investors at any wealth level.

Is a robo advisor better than investing on my own?

For most investors, robo advisors provide meaningful advantages over DIY investing: automated rebalancing ensures you maintain your target allocation, tax-loss harvesting can reduce your tax burden, and the algorithm prevents emotional decisions during market volatility. However, sophisticated investors who enjoy managing their own portfolios and understand tax optimization may not need robo advisor services.

Conclusion: Is a Robo Advisor Worth It?

Robo advisors represent a genuine innovation in democratizing professional investment management. For millions of Americans, these platforms provide sophisticated portfolio management at costs that would have been impossible a generation ago.

The verdict: Robo advisors are worth it for investors who want low-cost, automated portfolio management without the complexity of self-directed investing. They excel for young investors building wealth, busy professionals seeking convenience, and anyone wanting to avoid emotional investment decisions.

However, they aren’t universally superior. If you have complex financial situations requiring comprehensive planning, prefer human relationships for major decisions, or possess sufficient assets to justify traditional advisory fees, the hybrid approach or human advisors might serve you better.

The best approach? Honestly assess your financial complexity, time availability, and personal preferences. Many investors begin with robo advisors and transition to hybrid services as their wealth and needs evolve—there’s no single right answer, only the solution that fits your specific circumstances.