215Views 0Comments

How to Retire Early with Index Funds: Your Path to Financial Freedom

The average American couple retiring today will need approximately $315,000 in healthcare costs alone, separate from living expenses. Meanwhile, the FIRE (Financial Independence, Retire Early) movement has grown 500% since 2015, with practitioners achieving retirement 10-20 years earlier than traditional timelines. The common thread? Index funds. Research from Morningstar consistently shows that over 90% of actively managed funds underperform their benchmark indices over 15-year periods, making index funds not just a simple choice, but a mathematically superior one for building lasting wealth.

This guide provides a complete roadmap for retiring early using index funds—from understanding the fundamental calculations to executing advanced strategies that accelerate your timeline. Whether you’re starting with nothing or already on your path, you’ll find actionable frameworks to reach financial independence faster.

The Mathematics of Early Retirement with Index Funds

Defining Your FIRE Number

Early retirement begins with a single calculation: determining exactly how much you need to never work again. The foundation rests on the Trinity Study, updated regularly by financial researchers, which analyzed historical stock and bond returns to determine a safe withdrawal rate.

The Simple Formula:

Your FIRE Number = Annual Expenses × 25

This derives from the 4% safe withdrawal rate—the percentage you can theoretically withdraw annually without depleting your portfolio over a 30-year retirement. Using historical data, a diversified portfolio of 60% stocks and 40% bonds had a 95% success rate over 30 years using this withdrawal rate.

| Annual Expenses | FIRE Number Needed | Monthly Investment (10 years, 7% return) |

|---|---|---|

| $40,000 | $1,000,000 | $5,850 |

| $60,000 | $1,500,000 | $8,775 |

| $80,000 | $2,000,000 | $11,700 |

| $100,000 | $2,500,000 | $14,625 |

Why Index Funds Change the Math

Index funds don’t just simplify investing—they fundamentally improve your expected returns through reduced costs. The average actively managed equity fund charges 0.75-1.00% annually in fees, compared to just 0.03-0.08% for index funds. Over a 30-year career, this difference can cost you $200,000-$500,000 in lost compound growth on a $500,000 portfolio.

Vanguard’s founder Jack Bogle demonstrated this consistently: when you subtract fees from gross returns, index fund investors often outperform the majority of active investors who pay higher costs. The math is relentless—every percentage point in fees is a percentage point you’ll never recover.

Building Your Index Fund Portfolio for Early Retirement

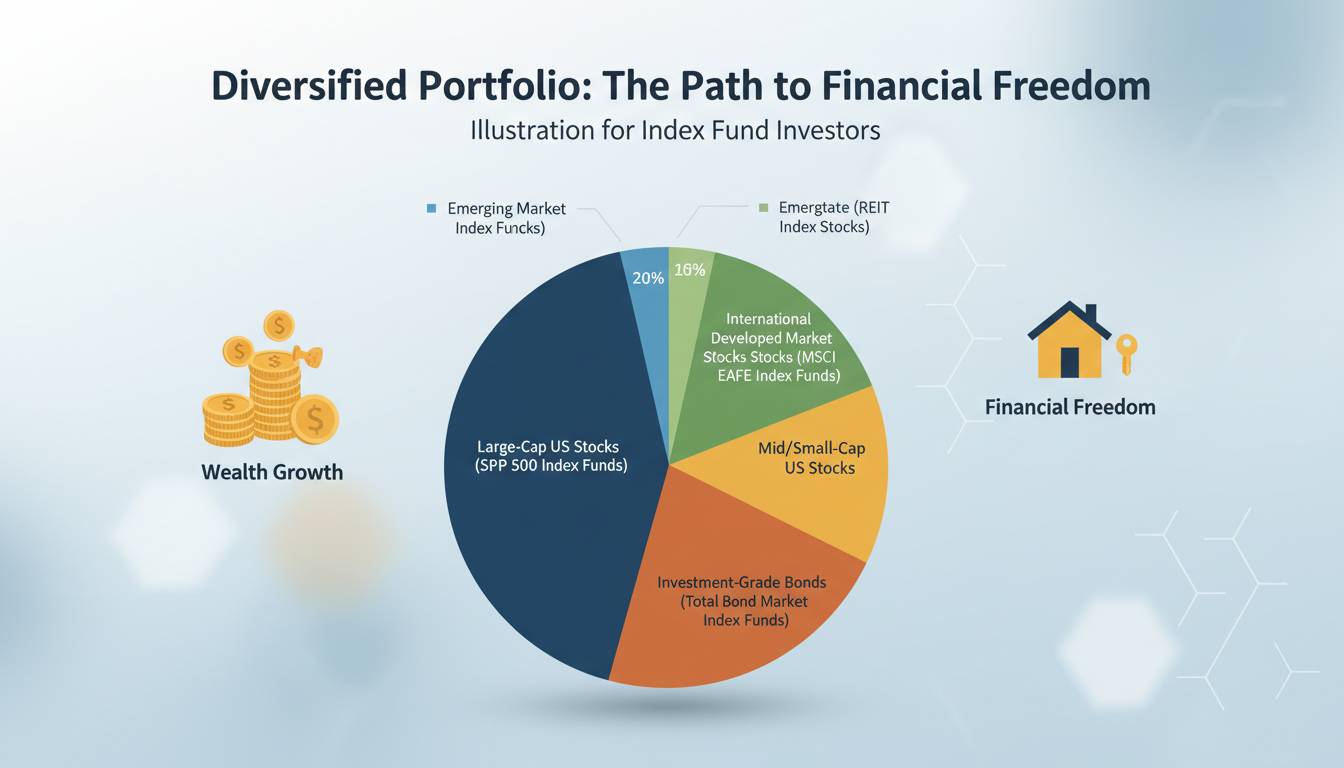

The Three-Fund Portfolio Foundation

The canonical approach for early retirement index fund investing uses three fund categories:

U.S. Total Stock Market Index Fund

This forms the growth engine of your portfolio. Funds like Vanguard Total Stock Market (VTSAX), Fidelity Total Market Index (FSKAX), or Schwab Total Stock Market (SWTSX) provide exposure to thousands of U.S. companies across all sectors and market capitalizations.

International Stock Market Index Fund

Diversification beyond U.S. borders reduces volatility and captures growth in emerging markets. Vanguard Total International (VTIAX), Fidelity International Index (FSPSX), or Schwab International Equity (SWISX) offer broad developed and emerging market exposure.

U.S. Bond Index Fund

Bonds provide stability and correlation inversely to stocks during market downturns. Vanguard Total Bond Market (VBTLX), Fidelity U.S. Bond Index (FXNAX), or Schwab U.S. Aggregate Bond (SWAGX) offer low-cost, diversified fixed income exposure.

Asset Allocation by Age and Risk Tolerance

| Age | Aggressive (Stocks/Bonds) | Moderate | Conservative |

|---|---|---|---|

| 25 | 90/10 | 80/20 | 70/30 |

| 35 | 85/15 | 75/25 | 60/40 |

| 45 | 80/20 | 70/30 | 50/50 |

| 55 | 70/30 | 60/40 | 40/60 |

| 60 (Early Retirement) | 60/40 | 50/50 | 40/60 |

Many early retirees actually increase stock allocation slightly in early retirement because their time horizon extends 30+ years. The key principle: hold enough stocks for growth while maintaining enough bonds to avoid selling during downturns.

Tax-Advantaged Accounts: Maximizing Every Dollar

The Account Priority Ladder

Strategic sequencing of tax-advantaged accounts dramatically accelerates your path to early retirement:

1. 401(k) with Employer Match

Contribute at minimum enough to capture your full employer match—this is an instant 50-100% return on that portion of your contribution. For 2024, you can contribute $23,000 ($30,500 if 50+).

2. Health Savings Account (HSA)

If you have a high-deductible health plan, HSA contributions triple-tax-advantage: tax-deductible going in, grows tax-free, and withdrawals for medical expenses are tax-free. After age 65, withdrawals for any purpose are taxed as ordinary income. This makes HSAs potentially the ultimate retirement account.

3. Roth IRA or Traditional IRA

For most early retirement seekers, a Roth IRA provides the best value—you pay taxes now at your current rate (likely lower than during retirement) and grow money tax-free forever. The income limits for 2024: $146,000 single, $230,000 married filing jointly for full contributions.

4. Taxable Brokerage Account

After maxing tax-advantaged accounts, taxable accounts offer flexibility without early withdrawal penalties. Index funds in taxable accounts are extremely tax-efficient, especially with qualified dividends taxed at lower rates.

The Roth Conversion Ladder

One of the most powerful strategies for early retirees involves converting traditional IRA or 401(k) funds to Roth gradually:

- Years 1-5: Live on taxable account funds and Roth contributions (principal only)

- Year 1: Convert $14,000 (standard deduction + lowest bracket) from traditional to Roth

- Year 2-5: Continue conversions, allowing each year’s conversion to grow tax-free for 5 years before withdrawal

- Year 6+: Withdraw conversions tax-free (the 5-year rule)

This strategy lets you manage your tax bracket in retirement while accessing funds penalty-free before age 59½.

The Compound Growth Engine: Time in the Market

How Compound Interest Amplifies Your Savings

Albert Einstein allegedly called compound interest the eighth wonder of the world. Whether he said it or not, the mathematics are undeniable. A 25-year-old investing $1,000 monthly with 7% average returns will have $2.4 million at age 65. Start at 35, and you’ll have only $1.1 million—less than half, despite investing for only 10 fewer years.

| Starting Age | Monthly Investment | 7% Annual Return | Total at Age 65 |

|---|---|---|---|

| 25 | $500 | 30 years | $609,000 |

| 25 | $1,000 | 30 years | $1,218,000 |

| 35 | $500 | 20 years | $243,000 |

| 35 | $1,000 | 20 years | $486,000 |

| 45 | $500 | 10 years | $87,000 |

| 45 | $1,000 | 10 years | $174,000 |

The gap between starting at 25 versus 35 on a $500 monthly investment: $366,000 in final portfolio value. That’s $60,000 in actual contributions difference, but $366,000 in compound growth difference—the true cost of waiting.

Dollar-Cost Averaging Through Volatility

Index fund investing during your accumulation phase naturally implements dollar-cost averaging—you invest fixed dollar amounts regularly, buying more shares when prices are low and fewer when prices are high. Over decades, this smooths out volatility and typically results in better average purchase prices than timing the market.

Research from Putnam Investments found that investors who stayed fully invested in the S&P 500 from 1963-2023 earned 10.1% annually, while those who missed just the 10 best days earned only 6.4%. Missing the 20 best days dropped returns to just 3.9%. Index funds keep you fully invested—always.

Advanced Strategies for Accelerating Early Retirement

Tax-Loss Harvesting

When your index fund investments decline, you can sell losing positions to offset capital gains elsewhere, reducing your tax bill. Simultaneously, you buy similar (but not identical) funds to maintain market exposure. For example:

- Sell Vanguard Total Stock Market (VTSAX) at a loss

- Buy iShares Core S&P Total U.S. Stock Market (ITOT)—similar exposure, different fund family

- Deduct up to $3,000 in net capital losses against ordinary income

- Carry forward excess losses to future years

This strategy can save $500-$3,000 annually in taxes for moderate earners, money that compounds into significant sums over decades.

The Bucket Strategy for Early Retirement Income

Rather than treating your portfolio as a single pool, sophisticated early retirees divide funds into three buckets:

Bucket 1 (Years 1-3): Cash and short-term bonds

– 2-3 years of expenses in cash, high-yield savings, and CDs

– Protects against sequence of returns risk in early retirement

Bucket 2 (Years 4-10): Intermediate bonds and stable stocks

– Bond funds and dividend-paying index funds

– Provides income while waiting for stock recovery if markets decline

Bucket 3 (Years 10+): Growth-oriented stock index funds

– Total stock market and international funds

– Designed for 20-30+ year growth horizon

This approach ensures you never need to sell stocks during a downturn to cover living expenses.

Common Mistakes That Derail Early Retirement

Mistake #1: Chasing Performance

Every year, investors pour money into last year’s top-performing funds, only to watch them underperform going forward. Research from DALBAR shows the average investor earns 3-4% less annually than the funds they invest in because of this timing behavior. Index funds cure this impulse—you accept market returns, which consistently beat the majority of active managers.

Mistake #2: Ignoring Expense Ratios

A 1% higher expense ratio doesn’t just cost you 1% annually—it compounds into massive opportunity cost. On a $500,000 portfolio over 25 years with 7% returns, a 0.05% expense ratio leaves you with $2.87 million versus $2.43 million with a 0.75% fee. That’s $440,000 lost to fees—money that should be in your pocket.

Mistake #3: Underestimating Healthcare Costs

Early retirees often forget that Medicare doesn’t start until 65. Between ages 50-65, you need to budget for private health insurance or ACA subsidies, which can cost $500-$1,500 monthly per person. Building this into your FIRE number prevents the painful scenario of early retirement derailed by healthcare costs.

Mistake #4: Failing to Account for Inflation

The Trinity Study used historical data, but future returns and inflation may differ. Building in a buffer—targeting a 3.5% or 3% withdrawal rate rather than 4%—provides insurance against uncertainty. Alternatively, plan for part-time work in early retirement to reduce withdrawal pressure.

Real Results: Early Retirement Success Stories

Case Study 1: The Software Engineer Path

John, a software engineer in Seattle, started investing at age 22 with $500 monthly into a 401(k) and Roth IRA. By age 35, he reached $300,000 in investments through consistent contributions and stock market growth. He increased contributions to $2,000 monthly after promotions. At age 45, his portfolio reached $1.2 million. He retired at 52 with annual expenses of $60,000—well below his $1.5 million FIRE number, providing a 25% safety buffer.

Key factors: Started early, maxed tax-advantaged accounts, maintained moderate expenses despite high income.

Case Study 2: The Dual-Income Family

Maria and Carlos, both teachers in Texas, earned combined income of $95,000. They invested 20% of income from age 28, maxing their 403(b)s and contributing to Roth IRAs. They lived modestly, driving used cars and cooking at home. By age 50, their $1.8 million portfolio supported their $60,000 annual expenses with a 3.3% withdrawal rate. They transitioned to part-time work for five years before fully retiring at 55.

Key factors: High savings rate (not high income), discipline in spending, dual tax-advantaged accounts.

Case Study 3: The Late Bloomer

Sarah didn’t start seriously investing until age 40 after paying off student loans. She invested $1,500 monthly into index funds and maximized catch-up contributions from age 50. Despite starting 15 years later than ideal, her $650,000 portfolio at 62, combined with reduced Social Security benefits, allowed her to retire at 62 with $40,000 in annual expenses.

Key factors: High savings rate, catch-up contributions, realistic expense expectations.

Your Roadmap to Financial Freedom

Early retirement with index funds isn’t a pipe dream—it’s a mathematical certainty when you apply consistent effort over time. The formula is simple: save aggressively, invest in low-cost index funds, minimize fees, and maintain discipline through market volatility.

The path requires sacrifice in the short term—living below your means, avoiding lifestyle inflation, and patient compounding. But the freedom gained far outweighs the temporary constraints. Whether you reach FIRE at 40, 50, or 60, you’ll have something priceless: control over your time.

Your immediate action steps:

- Calculate your FIRE number using annual expenses × 25

- Open or max out tax-advantaged accounts (401k, IRA)

- Choose a three-fund portfolio with lowest expense ratios

- Set up automatic monthly investments

- Review and adjust annually

The journey of a thousand miles begins with a single step. Start today.

Frequently Asked Questions

How much money do I need to retire early with index funds?

Your FIRE number equals your annual expenses multiplied by 25, based on the 4% safe withdrawal rate. For example, if you spend $50,000 annually, you need $1,250,000 invested. However, many financial planners recommend targeting a 3-3.5% withdrawal rate ($1.43-$1.67 million) for additional safety in early retirement, which lasts longer than 30 years.

Can I retire early with just $500,000?

Yes, but it requires significantly reducing your annual expenses. On a $500,000 portfolio with a 3% withdrawal rate, you could spend $15,000 annually. This typically means living in a low-cost area, minimizing housing costs, and potentially maintaining some part-time income for healthcare and living expenses before Medicare eligibility at 65.

What is the safest withdrawal rate for early retirement?

For early retirement extending 30-40 years, research suggests a 3-3.5% withdrawal rate provides near-100% success rates historically. The traditional 4% rule works well for 30-year retirements but carries more risk when retiring at 45 or 50. Using a variable withdrawal rate that adjusts based on portfolio performance adds additional safety.

Do index funds pay dividends?

Yes, many index funds include dividend-paying stocks and distribute dividends to shareholders quarterly or annually. Total market index funds typically yield 1.3-1.8% currently. You can choose to reinvest dividends (DRIP) to accelerate compounding or take them as cash flow during retirement.

How do I handle healthcare before Medicare?

For early retirees between 50-65, options include: ACA marketplace coverage with income-based subsidies (requires managing your withdrawal rate), spousal coverage through a working partner’s employer, part-time work with benefits, or high-deductible health plans paired with HSA investments. Healthcare is often the largest expense to budget for in early retirement.

Can I use index funds in a Roth IRA for early retirement?

Absolutely, and this is often ideal for early retirement. Roth IRA contributions (not earnings) can be withdrawn tax-free at any time without penalty. By contributing to a Roth IRA during your working years, you can access your principal in early retirement while your earnings grow tax-free. This makes Roth accounts excellent for funding the gap between retirement and traditional retirement account access age 59½.