301Views 0Comments

DeFi Explained: Simple Beginner’s Guide to Decentralized Finance

Decentralized Finance, commonly called DeFi, represents a fundamental shift in how people access financial services. Instead of relying on traditional banks, brokerages, or insurance companies, DeFi uses blockchain technology to enable peer-to-peer financial transactions—anyone with an internet connection can lend, borrow, trade, or earn interest on their assets without middlemen.

Key Insights

– DeFi eliminates intermediaries by using smart contracts on blockchains like Ethereum

– The total value locked in DeFi protocols exceeded $50 billion at peak markets

– Average DeFi transaction settlement takes seconds to minutes versus days for traditional finance

– Most DeFi platforms operate 24/7/365 with no geographic restrictions

– Yield farming and liquidity mining offer returns that dwarf traditional savings accounts

This guide breaks down DeFi into clear, digestible concepts so you can understand how it’s reshaping the financial landscape and what it means for your money.

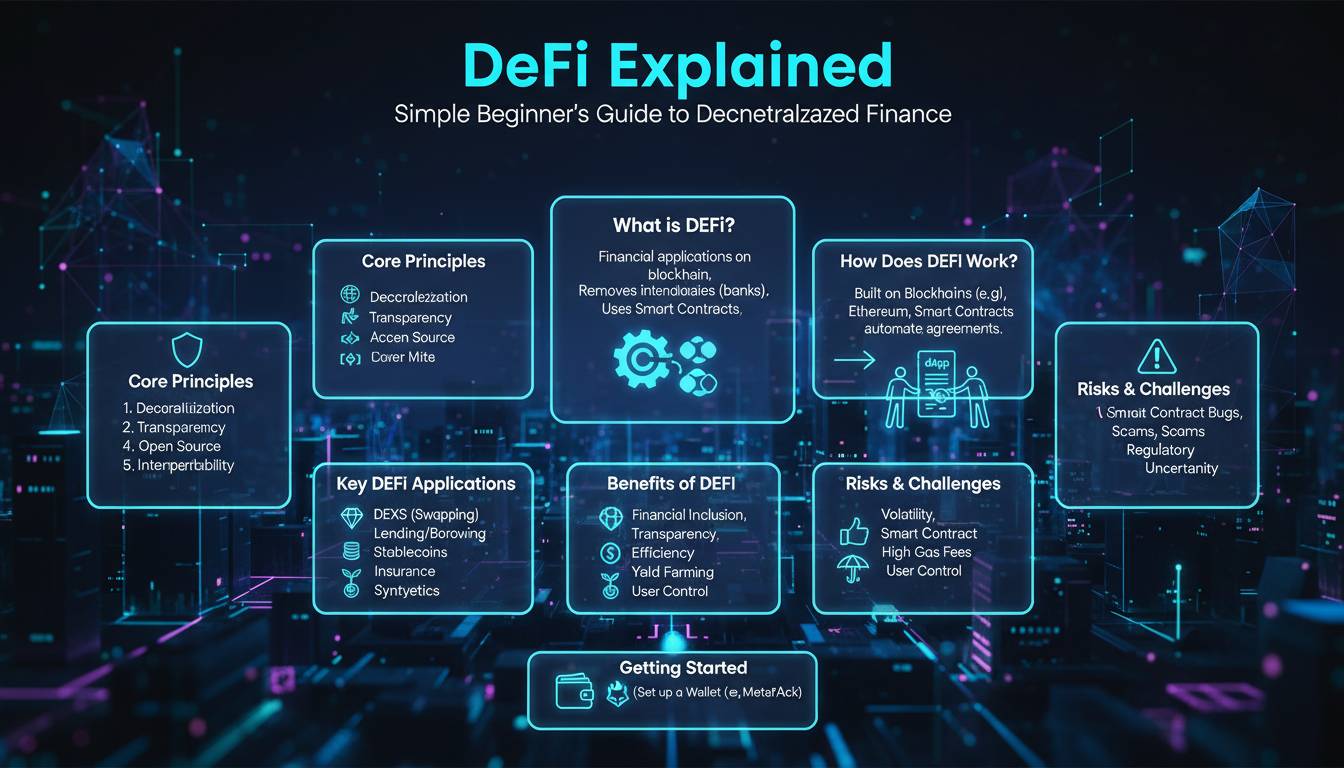

What Exactly is DeFi?

DeFi refers to financial applications built on decentralized blockchain networks that operate without traditional financial intermediaries. These applications—called protocols—replicate conventional financial services such as lending, borrowing, trading, and earning interest, but they do so automatically through lines of computer code called smart contracts.

The fundamental difference between DeFi and traditional finance lies in the removal of trust. In a conventional bank, you trust that institution to hold your money, process transactions, and honor agreements. In DeFi, you trust code. When you deposit funds into a DeFi lending protocol, a smart contract automatically allocates those funds to borrowers, calculates interest, and distributes returns—no human employees involved.

This architecture transforms financial services into publicly accessible infrastructure. Anyone can build on top of existing DeFi protocols, creating an ecosystem where financial products assemble and recombine like digital Lego blocks. A developer can take a lending protocol, add an exchange, and create an entirely new financial product within hours.

The movement gained significant momentum starting in 2020, when the combination of high cryptocurrency prices and pandemic-era stimulus payments drove massive capital inflows into DeFi protocols. While the market has experienced volatility, the underlying technology and user adoption have continued advancing.

How DeFi Actually Works

Understanding DeFi requires grasping three interconnected concepts: blockchain technology, smart contracts, and decentralized applications (dApps).

Blockchain as the Foundation

Blockchains serve as transparent, immutable ledgers that record all financial transactions. When you send cryptocurrency to another wallet, that transaction gets grouped with thousands of others into a “block,” then added to a permanent “chain” of previous blocks. Every participant can verify these transactions, eliminating the need for a central authority to confirm accuracy.

Ethereum, the second-largest blockchain by market capitalization, hosts the majority of DeFi activity. Its flexible programming language allows developers to write complex smart contracts that execute automatically when predetermined conditions are met.

Smart Contracts Execute Logic

A smart contract functions like a vending machine: insert the correct inputs, and you automatically receive the outputs without needing anyone to facilitate the exchange. In DeFi lending, for example, a smart contract might work like this:

- User deposits cryptocurrency as collateral

- Contract immediately calculates available borrowing power (typically 50-75% of collateral value)

- Another user borrows those funds, posting different cryptocurrency as collateral

- Smart contract automatically calculates interest for both parties

- When the borrower repays, funds transfer automatically to the lender

This automation happens in seconds or minutes rather than the days typically required for bank transfers. The code is visible to everyone—if anyone discovers a vulnerability, they can exploit it before developers patch it, which has led to significant security incidents in DeFi history.

Decentralized Applications Connect Users

A decentralized application (dApp) provides the user interface that connects people to smart contracts. Rather than downloading software, users typically access dApps through web browsers or mobile apps. The front-end looks similar to traditional websites, but behind the scenes, transactions interact directly with blockchain smart contracts rather than company servers.

Popular DeFi dApps include Uniswap (decentralized exchange), Aave (lending protocol), and Compound (interest-earning platform). These applications have facilitated billions of dollars in transactions, though users must remain vigilant about security and smart contract risks.

Core DeFi Concepts You Need to Understand

Several key concepts form the building blocks of the DeFi ecosystem. Understanding these terms helps you navigate the space confidently.

Yield and Interest Generation

Traditional savings accounts offer minimal interest—often less than 0.5% annually in the United States. DeFi protocols frequently offer substantially higher yields, sometimes exceeding 10-20% annually, though these rates fluctuate based on market conditions and token incentives.

When you supply cryptocurrency to a DeFi lending protocol, other users borrow your funds and pay interest. You receive a share of that interest minus any protocol fees. The rates adjust dynamically based on supply and demand for particular assets.

Liquidity Pools and Trading

Traditional stock exchanges match buyers with sellers—your order waits until someone accepts your price. DeFi uses a different model called automated market making (AMM), where traders swap directly from liquidity pools.

These pools contain pairs of tokens (like ETH and USDC) that traders can exchange against. Liquidity providers deposit both tokens into the pool and earn a portion of trading fees. This system operates continuously without requiring a traditional order book or market maker.

Tokenomics and Governance Tokens

Many DeFi protocols issue their own tokens that serve specific purposes within the ecosystem. Governance tokens typically grant holders voting rights on protocol upgrades and parameter changes. Some tokens provide fee discounts, while others offer yield farming rewards.

The economic design of these tokens varies significantly across projects, and understanding tokenomics requires examining each protocol’s specific token utility, supply distribution, and incentive structures.

Collateral and Undercollateralization

DeFi loans require超额抵押— borrowers must deposit more value than they borrow. If the collateral’s value drops significantly, smart contracts automatically liquidate the position to protect lenders. This mechanism maintains system stability without credit checks or identity verification.

Some newer protocols experiment with undercollateralized loans using oracle data, reputation systems, or identity verification, but these approaches remain less common than overcollateralized models.

Major DeFi Use Cases

DeFi protocols have evolved beyond experiments into genuine financial infrastructure serving millions of users. Here are the primary use cases driving adoption.

Lending and Borrowing

Platforms like Aave, Compound, and MakerDAO enable instant lending and borrowing without credit applications or approval processes. Users deposit supported cryptocurrencies as collateral and can immediately borrow other assets. Interest rates adjust algorithmically based on utilization—the more people borrow against a particular asset, the higher the rate climbs.

This accessibility matters particularly in regions where traditional banking remains limited. Anyone with cryptocurrency can participate in these markets regardless of location or banking status.

Decentralized Exchanges

Uniswap, Curve, and Balancer facilitate cryptocurrency trades directly from users’ wallets without centralized order books. These platforms processed over $150 billion in monthly trading volume at their peak (Uniswap data, 2021-2024). Slippage—the difference between expected and actual trade prices—remains a consideration, especially for large trades.

Stablecoins

DeFi relies heavily on stablecoins cryptocurrencies designed to maintain fixed values, typically pegged to the US dollar. Tether (USDT), USD Coin (USDC), and Dai provide price stability essential for lending, borrowing, and trading. Without stablecoins, the volatility of assets like Bitcoin or Ethereum would make most DeFi activities impractical.

Derivatives and Insurance

Protocols like Synthetix enable synthetic asset creation—tokenized representations of real-world assets like stocks, commodities, or currencies. Insurance protocols like Nexus Mutual cover smart contract failures, providing protection against code exploits that have historically caused significant losses.

The Risks You Should Know

DeFi offers substantial opportunities but comes with significant risks that traditional finance investors rarely encounter.

Smart Contract Vulnerabilities

Code bugs have led to billions of dollars in losses across DeFi history. The Ronin network hack resulted in approximately $620 million stolen . While security auditing firms review major protocols, vulnerabilities sometimes emerge years after deployment. Never invest more than you can afford to lose completely.

Impermanent Loss

When providing liquidity to AMM pools, you may experience impermanent loss—your funds could be worth less than simply holding the original tokens. This occurs when token price ratios shift significantly during your liquidity provision period. Understanding this risk is essential before supplying liquidity to trading pools.

Regulatory Uncertainty

DeFi operates in a regulatory gray area that could shift dramatically. Securities regulations, money transmitter laws, and tax reporting requirements may apply to DeFi activities in ways that remain unsettled. Building compliance into your DeFi strategy makes sense as regulatory frameworks develop.

Scams and Fraud

Rug pulls—where developers abandon projects after collecting investor funds—have plagued the space. Even legitimate projects may incentivize behavior that harms users. Thorough research, called due diligence, helps distinguish genuine opportunities from scams.

Getting Started with DeFi

If you’re considering exploring DeFi, approach it systematically and conservatively.

First, obtain a self-custody wallet like MetaMask or Rabby. This software allows you to interact directly with blockchain applications while maintaining control of your private keys. NEVER share your seed phrase with anyone—anyone requesting it is attempting to steal your funds.

Start with tiny amounts—perhaps $50-100 worth of cryptocurrency—to familiarize yourself with the process. Connect your wallet to a reputable decentralized exchange, purchase a small amount of a stablecoin like USDC, and experiment with a lending protocol that offers straightforward deposits and withdrawals.

Track your transactions meticulously. DeFi generates numerous interactions that create tax implications in many jurisdictions. Professional crypto tax software can help organize this complexity.

The Future of Decentralized Finance

DeFi continues evolving rapidly as developers address current limitations. Layer 2 scaling solutions like Arbitrum and Optimism reduce transaction costs and increase speed, making DeFi more practical for everyday use. Cross-chain bridges increasingly connect previously isolated blockchain ecosystems.

Institutional participation has grown substantially, with major financial firms exploring DeFi infrastructure for settlement, tokenization, and payments. Whether these institutions embrace fully decentralized models or adapt DeFi concepts to permissioned systems remains uncertain.

The convergence of DeFi with real-world assets—tokenized treasuries, real estate, and commodities—represents a significant expansion vector. This development could bridge traditional finance with decentralized systems, potentially bringing billions of dollars in traditional assets on-chain.

Frequently Asked Questions

Is DeFi legal in the United States?

DeFi occupies an uncertain legal position. US regulations require money transmitters and those offering securities to comply with specific registration and disclosure requirements. Some DeFi protocols have restricted access from US IP addresses, while others operate globally with varied compliance approaches. Consult a qualified attorney familiar with cryptocurrency regulations before participating.

How do I protect my DeFi investments from hackers?

Security measures include using hardware wallets for significant holdings, connecting only to verified dApps (check URLs carefully for phishing attempts), revoking unnecessary token approvals after transactions, using separate wallets for different protocols, and maintaining backup copies of seed phrases in secure locations. No security measure eliminates risk entirely.

What’s the difference between DeFi and centralized crypto exchanges?

Centralized exchanges like Coinbase hold your funds and process transactions on your behalf—they’re essentially traditional banks for cryptocurrency. DeFi protocols give you direct control of your assets through your wallet. You interact with smart contracts rather than company accounts. Both approaches offer different tradeoffs regarding convenience, security, and self-sovereignty.

Can I lose money in DeFi?

Absolutely. DeFi investments can lose value through asset price decline, smart contract hacks, rug pulls, impermanent loss, or regulatory actions. The high yields often reflect these risks. Never invest money you cannot afford to lose entirely, and only allocate a small portion of your portfolio to DeFi until you understand the risks thoroughly.

Do I need a lot of money to start with DeFi?

No. Many protocols have minimal requirements, and some transactions cost only a few dollars in network fees. However, network congestion can increase transaction costs substantially, so starting during low-traffic periods makes sense. Some platforms require minimum deposits, so research specific protocol requirements before transferring funds.

How are DeFi interest rates determined?

DeFi lending rates work algorithmically based on supply and demand. When many people want to borrow an asset, rates rise to attract more lenders. When supply exceeds demand, rates fall. These rates adjust continuously, sometimes multiple times per day, unlike traditional finance interest rates that typically change far less frequently.