302Views 0Comments

How Does Blockchain Work? Simple Guide for Beginners

Blockchain technology has become one of the most discussed innovations of the 21st century, yet many people still find it confusing or intimidating. At its core, blockchain is a revolutionary way to store and share information—one that promises greater transparency, security, and efficiency than traditional systems. Whether you’re a business owner exploring new technologies, a student curious about digital systems, or simply someone who wants to understand the buzzword, this guide will walk you through blockchain fundamentals in plain English.

Unlike conventional databases controlled by a single entity, blockchain operates across a network of computers, making it nearly impossible to alter past records without detection. This unique architecture has implications far beyond cryptocurrencies, touching industries from healthcare to supply chain management. By the end of this article, you’ll have a solid understanding of how blockchain works, why it matters, and how it’s being applied in the real world.

What Exactly Is Blockchain?

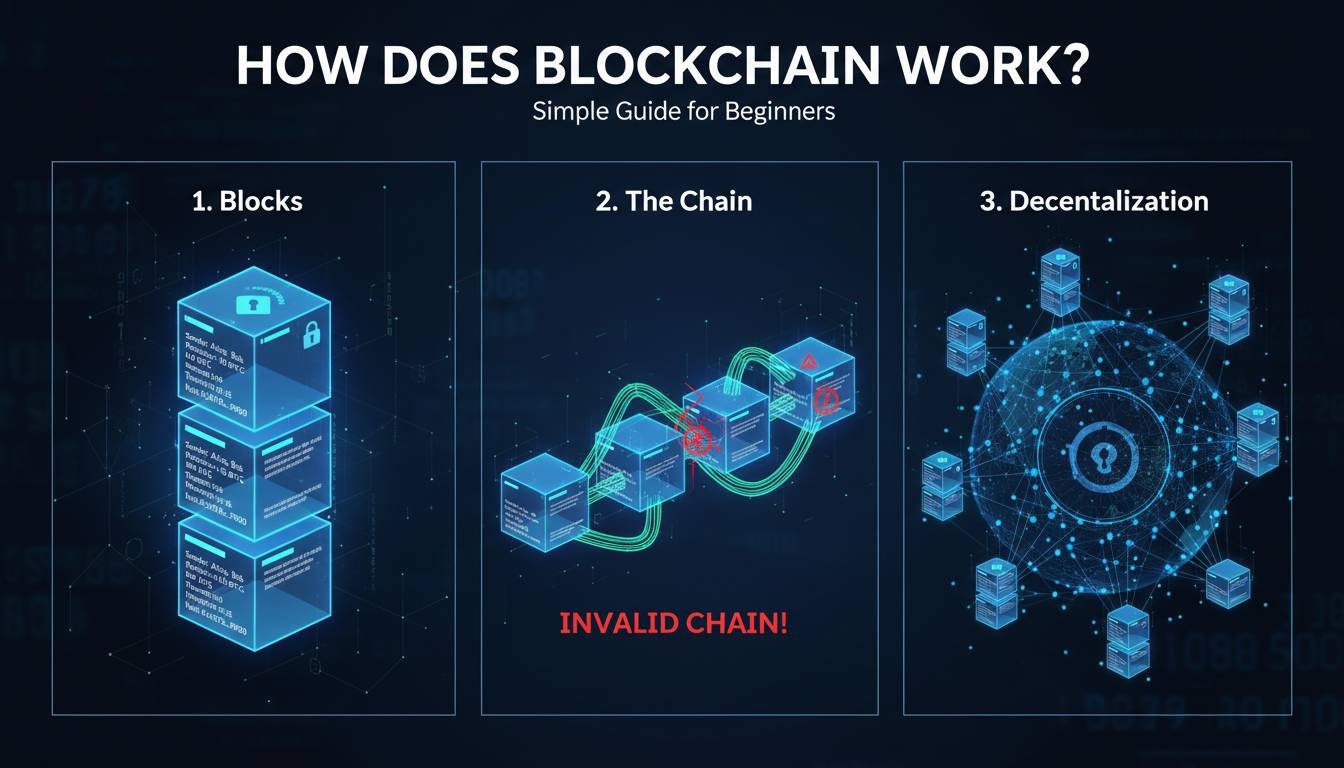

Blockchain is a distributed digital ledger that records transactions across multiple computers in a way that makes the records extremely difficult to change retroactively. Think of it as a shared spreadsheet that thousands of people can view and update, but where every change is permanently recorded and visible to everyone in the network.

The term “blockchain” comes from how the technology stores data: individual records, called “blocks,” are linked together in a chronological chain. Each block contains three key elements: data, a hash (a unique digital fingerprint), and the hash of the previous block. This interconnected structure is what makes blockchain so secure—tampering with any single block would invalidate every subsequent block in the chain.

Why “Distributed” Matters

Traditional databases store information on centralized servers controlled by one organization. If hackers compromise that server, they can alter or delete data. Blockchain distributes identical copies of the ledger across thousands of computers, called “nodes,” worldwide. For any change to be considered valid, the majority of nodes must agree on it. This decentralization means there’s no single point of failure—a feature that dramatically increases security and reliability.

How Blockchain Works: A Step-by-Step Breakdown

Understanding blockchain requires following a transaction from initiation to confirmation. Here’s how the process unfolds in practice.

1. Transaction Initiation

When someone wants to transfer value or record information on a blockchain, they create a transaction request. This could be sending cryptocurrency, verifying a diploma, or tracking a shipping container. The transaction includes details about what information is being recorded and who it’s coming from—secured through cryptographic keys that prove ownership.

2. Transaction Broadcasting

Once created, the transaction is broadcast to a network of nodes (computers) scattered around the world. Unlike banks that operate during business hours, blockchain networks run 24/7. The transaction enters a “mempool”—a waiting area where unconfirmed transactions accumulate. Network congestion can sometimes cause delays during peak periods.

3. Validation and Consensus

Nodes in the network examine the transaction to ensure it’s legitimate. They verify that the sender actually has what they’re sending and that the transaction follows the network’s rules. This process, called “consensus,” varies by blockchain. The two most common mechanisms are:

| Consensus Mechanism | How It Works | Examples |

|---|---|---|

| Proof of Work (PoW) | Miners compete to solve complex mathematical puzzles; winner adds the block | Bitcoin, Dogecoin |

| Proof of Stake (PoS) | Validators put up cryptocurrency as collateral; selected randomly to confirm blocks | Ethereum, Cardano |

Proof of Stake consumes approximately 99.9% less energy than Proof of Work, according to the Ethereum Foundation (2023).

4. Block Creation

Once consensus is reached, the transaction is grouped with other pending transactions into a new block. This block includes a timestamp, transaction data, the previous block’s hash, and its own unique hash. The block is then added to the existing chain—permanently.

5. Permanent Recording

After a block is added to the blockchain, it’s replicated across all nodes in the network. Each node updates its copy of the ledger to include the new block. This synchronization ensures everyone has the same version of history. Once recorded, information becomes practically immutable—altering historical data would require controlling the majority of the network’s computing power, which is economically and practically infeasible for major blockchains.

The Building Blocks of Blockchain Technology

Understanding blockchain requires familiarity with several key components that work together to create a secure, transparent system.

Cryptographic Hashing

Hashing is the process of converting input data into a fixed-size string of characters. Each block’s hash is unique—similar to a digital fingerprint. If you change even a single character in the block’s data, the hash changes completely. This makes it easy to detect tampering, as any modification would break the chain’s link to the next block.

Public and Private Keys

Blockchain users possess two cryptographic keys: a public key (like an account number anyone can see) and a private key (like a password that must be kept secret). Transactions are signed with private keys, proving authenticity without revealing the key itself. Losing your private key means losing access to your assets permanently—there’s no “forgot password” option.

Smart Contracts

Smart contracts are self-executing programs stored on the blockchain that automatically enforce agreement terms when conditions are met. If you rent an apartment through a smart contract, for instance, the digital key could automatically transfer to the tenant once payment is received—no middleman required. This automation removes the need for trusted intermediaries in many business scenarios.

Types of Blockchain Networks

Not all blockchains operate the same way. Understanding the different types helps explain how the technology adapts to various use cases.

| Type | Accessibility | Speed | Best Use Cases |

|---|---|---|---|

| Public | Anyone can participate | Slower | Cryptocurrencies, decentralized apps |

| Private | Invitation-only | Faster | Enterprise internal systems |

| Consortium | Multiple organizations | Balanced | Banking, supply chains |

| Hybrid | Mix of public/private | Variable | Gaming, regulated industries |

Public blockchains like Bitcoin and Ethereum offer maximum decentralization and security but sacrifice some speed. Private blockchains sacrifice decentralization for speed and control—suitable for internal enterprise operations where trust is established among known participants.

Real-World Applications Beyond Cryptocurrency

While cryptocurrency remains blockchain’s most famous application, the technology is transforming numerous industries.

Supply Chain Management

Walmart uses blockchain to track food products from farm to shelf, reducing the time it takes to trace the source of contaminated produce from 7 days to 2.2 seconds. This transparency helps identify problems faster and holds suppliers accountable for quality.

Healthcare

Medical records stored on blockchain can be securely shared between hospitals, specialists, and patients while maintaining privacy. Patients gain control over who accesses their health information, and healthcare providers get a complete, unchangeable medical history.

Voting Systems

Several countries, including Estonia and Sierra Leone, have experimented with blockchain-based voting. The technology can prevent vote tampering while maintaining voter anonymity, potentially revolutionizing democratic processes.

Digital Identity

Self-sovereign identity systems allow individuals to control their personal information rather than relying on centralized databases that can be breached. Blockchain provides verifiable credentials without exposing underlying data—a crucial advancement for privacy.

Common Misconceptions About Blockchain

Despite growing awareness, several myths persist about blockchain technology.

Myth #1: Blockchain is the same as Bitcoin.

Bitcoin is just one application of blockchain technology—a cryptocurrency using a blockchain ledger. Blockchain is the underlying infrastructure; Bitcoin is one of thousands of applications built upon it.

Myth #2: Blockchain is completely unchangeable.

While blockchain records are extremely difficult to alter, it’s not technically impossible. A “51% attack” could theoretically allow bad actors to rewrite history—but executing this on major networks like Bitcoin would cost billions and require controlling more than half the network’s computing power.

Myth #3: Blockchain is always slow and energy-inefficient.

Earlier blockchains like Bitcoin consume significant energy, but newer systems like Proof of Stake blockchains are dramatically more efficient. Layer 2 solutions also address speed limitations, enabling thousands of transactions per second.

The Future of Blockchain Technology

The blockchain landscape continues evolving rapidly. Enterprise adoption is accelerating, with major corporations including IBM, Microsoft, and Amazon offering blockchain-based services. The global blockchain market is projected to reach $1.4 trillion by 2030, according to Grand View Research (2023).

Interoperability—the ability for different blockchains to communicate—is becoming a major focus. Just as the internet connected isolated computer networks, projects like Polkadot and Cosmos aim to connect previously siloed blockchains.

Regulation is also maturing. The European Union’s MiCA framework provides clear cryptocurrency rules, while the US continues developing its regulatory approach. Clearer regulations will likely accelerate institutional adoption.

Frequently Asked Questions

How long does it take to confirm a blockchain transaction?

Transaction times vary significantly by blockchain. Bitcoin typically takes 10-60 minutes for confirmation, while Ethereum often confirms in seconds to minutes during normal network conditions. Factors include network congestion, transaction fees paid, and the specific blockchain’s design.

Can blockchain transactions be reversed?

Generally, no—one of blockchain’s core features is immutability. Once a transaction is confirmed and added to the blockchain, it cannot be reversed. This is why verifying transaction details before sending is critical. Some blockchain networks have emergency recovery mechanisms, but these are rare exceptions.

Do I need technical expertise to use blockchain?

No. User-friendly wallets and exchanges make cryptocurrency accessible to non-technical users. Services like Coinbase and Cash App abstract much of the complexity. However, understanding basic concepts like private keys and transaction verification helps prevent costly mistakes.

Is blockchain secure?

Yes, blockchain provides strong security through decentralization, cryptography, and consensus mechanisms. No system is entirely invulnerable, but altering data on a well-established blockchain would require controlling most of the network—making it economically impractical. Major blockchains like Bitcoin have never been successfully hacked.

How is blockchain different from a regular database?

Databases typically allow authorized users to create, read, update, and delete records. Blockchain only allows creating and reading—once data is written, it cannot be modified or deleted. Additionally, databases are usually controlled by single entities while blockchain distributes control across networks.

What programming languages are used in blockchain development?

Solidity (for Ethereum smart contracts), Rust, Go, C++, and Python are commonly used. Solidity dominates for decentralized application development, while Rust has gained popularity for its performance and memory safety in blockchain contexts.

Conclusion

Blockchain technology represents a fundamental shift in how we store, verify, and share information. By combining decentralization, cryptographic security, and consensus mechanisms, it creates systems that are more transparent, resilient, and trustworthy than traditional alternatives. While still evolving, blockchain has moved beyond theoretical potential to practical, real-world applications transforming industries from finance to healthcare.

Understanding blockchain basics—the concepts of blocks, nodes, consensus mechanisms, and immutability—provides a foundation for evaluating how this technology might impact your business or personal life. Whether you eventually invest in cryptocurrency, implement blockchain solutions for your organization, or simply engage with digital systems, the principles outlined in this guide will help you navigate an increasingly blockchain-integrated world.

The key takeaway: blockchain isn’t just about digital money. It’s about establishing trust in a digital world where intermediaries have traditionally been necessary—and finding new ways to verify truth without relying on single points of control.