214Views 0Comments

How to Calculate Net Worth: Simple Step-by-Step Method

Net worth represents the most comprehensive snapshot of your financial health. It calculates the difference between everything you own (your assets) and everything you owe (your liabilities). Understanding how to calculate net worth is the foundation of personal financial literacy, yet millions of Americans have never computed this critical number.

Key Insights

– Only 32% of Americans regularly track their net worth

– The median net worth for U.S. households is approximately $192,700

– Net worth calculation reveals financial progress more accurately than income alone

– Knowing your number is the first step toward building wealth

This guide provides a complete, beginner-friendly method for calculating your net worth, explains each component in detail, and shows you how to interpret the results to improve your financial trajectory.

What Exactly Is Net Worth?

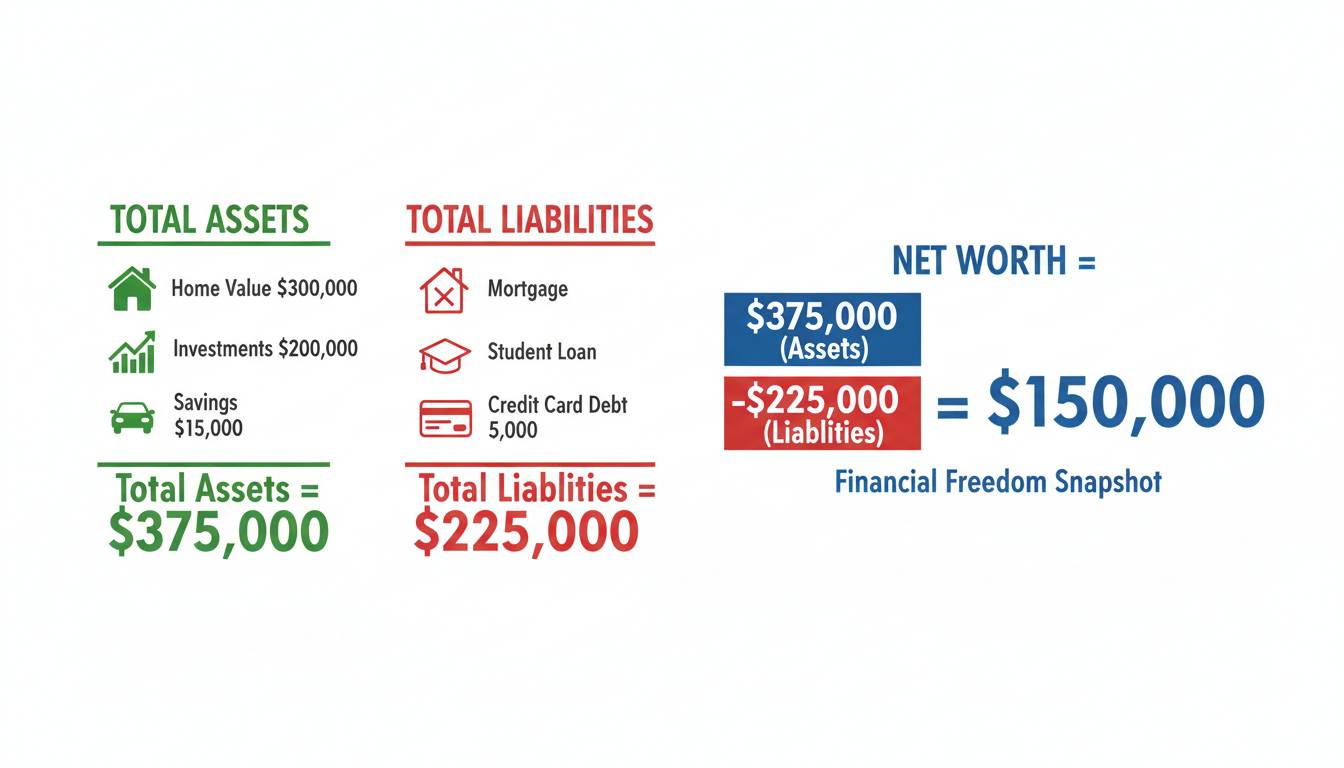

Net worth is a financial metric that quantifies your overall wealth by subtracting your total liabilities from your total assets. The formula is straightforward:

Net Worth = Total Assets – Total Liabilities

A positive net worth means your assets exceed your debts—you own more than you owe. A negative net worth indicates your liabilities exceed your assets, meaning you’re technically “underwater” financially.

The Federal Reserve’s Survey of Consumer Finances reports that the median net worth for American families varies dramatically by age, education, and income level. Younger families under 35 have a median net worth of approximately $39,000, while those aged 65-74 see a median of approximately $409,900. These figures illustrate why net worth serves as a better indicator of financial security than annual income alone.

Your net worth accounts for all financial facets: savings, investments, property, debts, and obligations. Unlike a simple bank balance, it presents the complete picture of where you stand financially.

Understanding Your Assets

Assets encompass everything you own that holds monetary value. These divide into two primary categories: liquid assets and illiquid assets.

Liquid Assets

Liquid assets are funds you can access quickly without significant penalties or time delays. These include:

- Checking accounts: Immediate access funds for daily expenses

- Savings accounts: Emergency funds and short-term savings

- Money market accounts: Slightly higher-yielding liquid accounts

- Certificates of deposit (CDs): Time deposits (though early withdrawal penalties apply)

- Cash on hand: Physical currency available immediately

The general financial recommendation suggests maintaining 3-6 months of living expenses in liquid assets. According to Bankrate’s 2024 survey, only 44% of Americans have sufficient emergency savings to cover a $1,000 unexpected expense.

Investment Accounts

Investment accounts represent assets that grow over time through appreciation, interest, or dividends:

- 401(k) balances: Employer-sponsored retirement accounts

- Individual retirement accounts (IRAs): Traditional and Roth retirement savings

- Brokerage accounts: Taxable investment accounts for non-retirement goals

- College savings plans (529 plans): Education-specific investment accounts

- HSA balances: Health savings accounts that function as triple-tax-advantaged investment accounts

Vanguard’s How America Saves 2024 report indicates the average 401(k) balance for participants is approximately $112,000, though median balances tell a different story at roughly $30,000—highlighting how averages can mislead.

Property and Physical Assets

Real estate and tangible possessions constitute significant asset categories:

- Primary residence: The market value of your home minus any mortgage debt

- Investment properties: Rental properties and vacation homes

- Vehicles: Cars, trucks, and motorcycles (typically depreciating assets)

- Valuables: Jewelry, art, collectibles, and luxury items

The National Association of Realtors reports the median existing home price reached approximately $407,100 in late 2024, making real estate the largest single asset for most American homeowners.

How to Value Your Assets

Assigning accurate values requires different approaches depending on the asset type:

| Asset Type | Valuation Method | Data Source |

|---|---|---|

| Bank accounts | Current balance | Online banking |

| Investments | Current market value | Brokerage statements |

| Real estate | Estimated market value | Zillow, Redfin, or professional appraisal |

| Vehicles | Kelley Blue Book value | kbb.com |

| Personal property | Estimated resale value | Research comparable sales |

Understanding Your Liabilities

Liabilities represent debts and financial obligations you owe to others. Properly accounting for all debts ensures an accurate net worth calculation.

Secured Liabilities

Secured debts are tied to specific assets as collateral:

- Mortgage: Loans secured by real estate, typically spanning 15-30 years

- Auto loans: Vehicle financing agreements

- Home equity loans/lines of credit: Borrowed against home equity

The Federal Reserve reports the total mortgage debt outstanding in the United States exceeds $12 trillion, making mortgages the largest liability category for most households.

Unsecured Liabilities

Unsecured debts lack collateral backing:

- Credit card balances: Revolving credit balances

- Student loans: Education financing

- Personal loans: Unsecured borrowing for various purposes

- Medical debt: Outstanding medical bills

- Child support/alimony: Court-ordered payment obligations

TransUnion reports the average American carries approximately $6,300 in credit card debt, with an average interest rate exceeding 24%—a significant drain on wealth building.

Accrued Expenses

Don’t overlook smaller ongoing obligations:

- Property taxes owed: If not escrowed

- Income taxes owed: If you underwithheld

- Utility deposits: Money held by service providers

- Pending legal judgments: Outstanding court-ordered payments

The Step-by-Step Calculation Method

Now that you understand the components, here’s how to calculate your net worth accurately:

Step 1: Gather All Financial Statements

Collect documentation for every account:

- Bank statements (all accounts)

- Investment account statements (401k, IRA, brokerage)

- Loan statements (mortgage, auto, student)

- Credit card statements

- Property records and vehicle titles

- Any other financial obligations

CFPB research shows 41% of Americans have “shadow financial accounts” they forget to track, making comprehensive documentation essential for accuracy.

Step 2: List All Assets with Values

Create a comprehensive asset list:

- Cash and checking: $8,500

- Savings account: $15,000

- 401(k) balance: $45,000

- Roth IRA: $12,000

- Brokerage account: $7,500

- Vehicle (2019 Honda Civic): $14,000

- Home value (estimated): $350,000

Total Assets: $452,000

Step 3: List All Liabilities with Balances

Document every debt:

- Mortgage balance: $280,000

- Auto loan balance: $8,500

- Credit card balance: $2,100

- Student loans: $22,000

Total Liabilities: $312,600

Step 4: Subtract Liabilities from Assets

Net Worth = Total Assets – Total Liabilities

Net Worth = $452,000 – $312,600 = $139,400

This positive net worth of $139,400 indicates the individual has accumulated meaningful wealth despite ongoing debt obligations.

Why Your Net Worth Matters More Than Income

Financial advisors consistently emphasize net worth over income for several compelling reasons:

It Reveals True Financial Health

Income tells you nothing about spending habits, debt loads, or savings rates. Two households earning $100,000 annually can have radically different net worths—one might have $200,000 saved while another lives paycheck to paycheck with no savings.

A 2024 GOBankingRates survey found 56% of Americans couldn’t cover a $1,000 emergency with savings, despite many earning comfortable incomes. This disconnect between income and financial security underscores why net worth matters.

It Tracks Progress Over Time

Net worth provides a longitudinal metric for measuring financial improvement. Comparing your net worth annually reveals whether you’re building wealth or falling behind, regardless of income changes.

The S&P 500 has historically returned approximately 10% annually, but personal net worth depends on savings behavior, debt management, and asset allocation—not just investment returns.

It Enables Better Financial Decisions

Understanding your net worth helps with major life decisions:

- Retirement planning: Knowing your current position helps estimate if you’re on track

- Major purchases: Evaluating how buying a car or home affects your overall position

- Career changes: Assessing whether taking a lower salary makes sense with equity compensation

- Estate planning: Understanding what you’re passing to heirs

Common Mistakes in Net Worth Calculations

Avoid these errors that lead to inaccurate calculations:

Mistake #1: Including Retirement Contributions as Expenses

When calculating net worth, remember that 401(k) contributions are assets, not expenses. You’re shifting money from one asset form (cash) to another (investments). Your net worth doesn’t decrease—you’ve simply reallocated wealth.

Mistake #2: Overlooking Small Debts

Credit card balances, medical debt, and small personal loans often get forgotten. These “micro-debts” add up quickly. A $500 credit card balance might seem insignificant but represents real liability that affects your true position.

Mistake #3: Using Purchase Price Instead of Market Value

Your home, vehicle, and other assets should be valued at current market prices, not what you paid. A home purchased for $250,000 now worth $350,000 adds $100,000 to your assets despite the original purchase price.

Mistake #4: Ignoring Unfunded Liabilities

Future obligations like upcoming tuition payments, expected tax bills, or pending legal settlements deserve consideration. While not all can be precisely quantified, acknowledging them provides realistic expectations.

Mistake #5: Forgetting About Taxes

Many assets have tax implications. 401(k) and traditional IRA balances represent pre-tax money—you’ll owe income taxes when withdrawing. Net worth calculations typically use the gross balance, though some prefer calculating “after-tax net worth” for precision.

Interpreting Your Net Worth Number

Understanding what your net worth means requires context:

Net Worth Benchmarks by Age

| Age Range | Median Net Worth | Average Net Worth |

|---|---|---|

| Under 35 | $39,000 | $183,500 |

| 35-44 | $135,600 | $549,600 |

| 45-54 | $212,500 | $975,800 |

| 55-64 | $364,500 | $1,566,900 |

| 65-74 | $409,900 | $1,794,600 |

| 75+ | $335,600 | $1,624,100 |

Source: Federal Reserve Survey of Consumer Finances, 2023

These figures reveal that most Americans accumulate wealth gradually, with significant acceleration in peak earning years.

Negative Net Worth Is Common (Temporarily)

According to Federal Reserve data, approximately 13% of American households have negative net worth. This often occurs early in careers when student loans exceed accumulated assets, or after major life events like divorce or illness. The key is trending positive over time.

Strategies to Increase Your Net Worth

Once you’ve calculated your number, these proven approaches help improve it:

Accelerate Debt Paydown

Target high-interest debt first—typically credit cards carrying 20%+ interest rates. The “avalanche method” (highest interest first) saves the most money, while the “snowball method” (smallest balance first) provides psychological wins.

Maximize Retirement Contributions

Employer 401(k) matches represent immediate 100% returns. Maxing out 401(k) contributions ($23,000 in 2024 for those under 50) significantly accelerates wealth building through tax advantages and compound growth.

Build Emergency Savings

Three to six months of expenses in high-yield savings accounts prevents retirement account withdrawals during crises—avoiding the 10% penalty and maintaining compound growth.

Invest Beyond Retirement Accounts

Taxable brokerage accounts provide flexibility and additional growth opportunities beyond retirement account limits.

Tracking Your Net Worth Over Time

Calculating net worth once provides limited value. Regular tracking reveals trends:

- Monthly: Useful during major financial transitions

- Quarterly: Good for active wealth builders

- Annually: Sufficient for stable financial situations

Many free tools simplify tracking:

- Personal capital provides free net worth tracking

- Mint (though discontinued) alternatives like Monarch Money

- Simple spreadsheet tracking

- Manual calculations with calendar reminders

Frequently Asked Questions

How often should I calculate my net worth?

Most financial experts recommend calculating your net worth at least annually, though quarterly reviews can help if you’re actively working to increase it. The most important habit is calculating it consistently so you can track meaningful trends over time.

Does my net worth include my home?

Yes, your primary residence counts as an asset in net worth calculations. However, remember that your mortgage liability subtracts from that asset value. Many first-time homeowners are surprised to find their home equity (home value minus mortgage balance) represents a significant portion of their total net worth.

What is a good net worth for my age?

While comparisons can be useful benchmarks, “good” net worth depends entirely on your individual circumstances. A more useful measure is whether your net worth is growing consistently through savings, investments, and debt reduction regardless of your starting point.

Should I include my car in net worth calculations?

Yes, vehicles count as assets, though they typically depreciate over time. Use current market value (not purchase price) when calculating. Remember that auto loans subtract from this value—if you owe more on your car than it’s worth, that portion counts as negative net worth.

Does net worth include future Social Security benefits?

No, Social Security benefits aren’t included in net worth calculations because they’re not currently owned assets. However, understanding your expected Social Security income helps plan retirement financial needs alongside your net worth.

What’s the difference between net worth and liquid net worth?

Liquid net worth excludes illiquid assets like real estate, retirement accounts with penalties, and personal property. It represents funds you could access immediately in an emergency. Many financial planners consider both numbers—liquid net worth for emergency planning, total net worth for long-term wealth assessment.

Conclusion

Calculating your net worth isn’t just an accounting exercise—it’s a powerful tool for understanding your complete financial picture. By subtracting everything you owe from everything you own, you gain clarity about your true financial position.

The method is simple: gather documentation, list all assets at current market values, list all liabilities at current balances, then subtract. Yet this straightforward calculation reveals insights that income figures alone never could.

Whether your number is positive, negative, or zero, knowing where you stand enables intentional progress. The wealthy understand their net worth precisely because it measures what actually matters—the gap between your resources and your obligations.

Start with today’s calculation, commit to annual reviews, and watch your financial trajectory improve as you make informed decisions aligned with your true wealth position.