7Views 0Comments

Best Retirement Accounts for Beginners to Build Wealth

Retirement accounts represent the most powerful wealth-building tools available to American workers, offering tax advantages that can transform modest contributions into substantial nest eggs over decades. Choosing the right account type—401(k), IRA, or both—can mean the difference of hundreds of thousands of dollars in retirement savings.

📊 KEY STATS

- $1.47 million was the average 401(k) balance in 2023 for participants aged 65-74

- $293,200 was the average IRA balance for households approaching retirement

- Workers who receive employer matching contributions see 50% higher 401(k) balances than those without (T. Rowe Price, 2023)

- Only 36% of working-age Americans have calculated how much they need for retirement

Key Insights

- Employer-sponsored 401(k) plans with matching funds offer immediate 100% returns on your contributions

- Roth accounts provide tax-free growth and withdrawals, ideal for younger earners in lower tax brackets

- Traditional accounts offer upfront tax deductions but taxed upon withdrawal

- Most beginners should prioritize 401(k) matching before contributing to IRAs

- Starting early matters more than maximizing contributions—time in the market beats timing the market

This guide breaks down each retirement account type, explains who benefits most from each option, and provides a clear roadmap for beginners ready to start building long-term wealth.

Why Retirement Accounts Matter More Than Regular Investment Accounts

Before exploring specific account types, understanding the fundamental advantage of retirement accounts is essential. The US tax code provides substantial incentives for saving for retirement specifically rather than general investing.

Tax advantages fall into three primary categories:

- Tax-deductible contributions reduce your taxable income in the contribution year

- Tax-deferred growth allows your investments to compound without annual capital gains taxes

- Tax-free withdrawals in retirement mean you never pay taxes on investment gains

A regular brokerage account lacks all three benefits. If you invest $10,000 annually in a taxable account earning 7% average returns, you might lose 15-20% of your gains annually to taxes. Over 30 years, this tax drag can reduce your final balance by 40% or more compared to a tax-advantaged retirement account.

The power of tax-free compounding explains why retirement accounts consistently outperform taxable investing for long-term goals. A $10,000 contribution at age 25 growing at 7% annually becomes approximately $76,000 by age 65. The same contribution in a taxable account after accounting for annual capital gains taxes might yield only $45,000-$50,000.

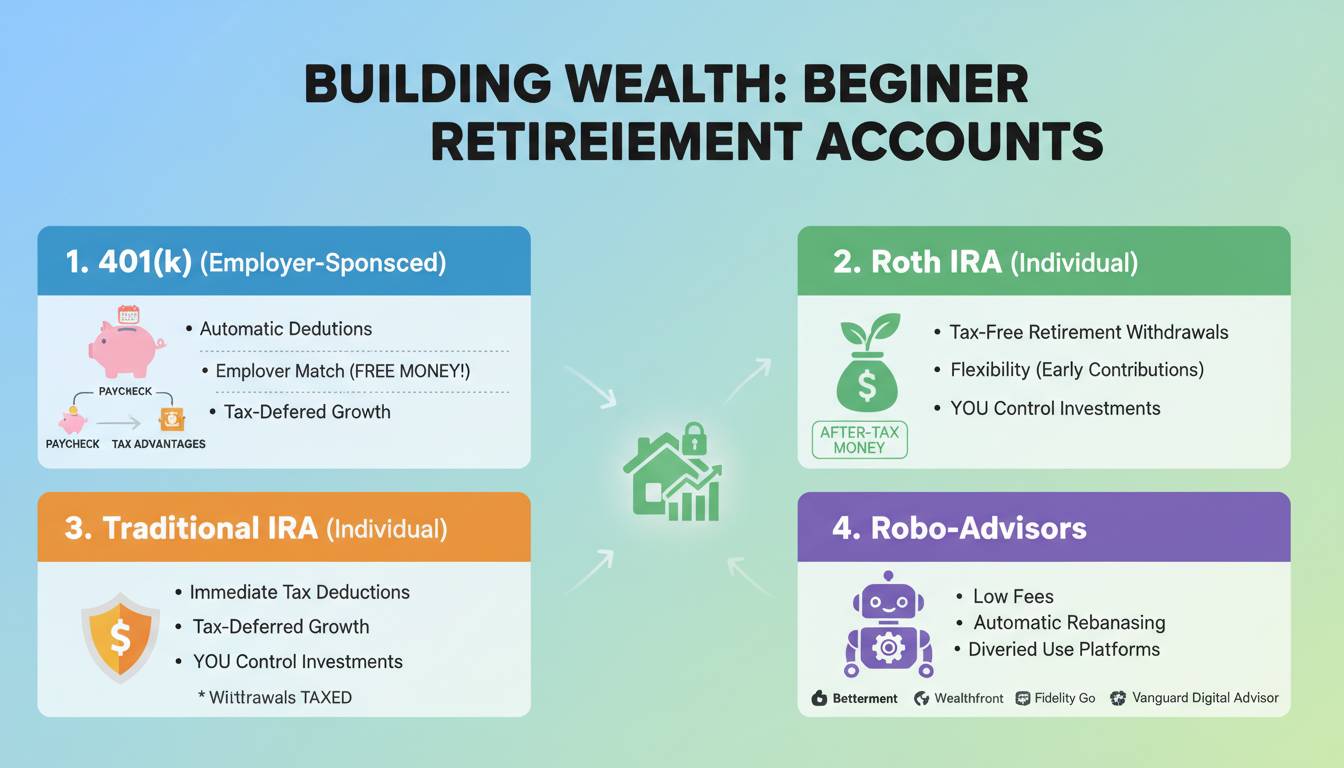

Employer-Sponsored Retirement Accounts: 401(k) Plans

The 401(k) remains the most accessible retirement vehicle for working Americans, particularly for those employed by companies offering retirement benefits. Named after the Internal Revenue Code section that created them, these employer-sponsored plans have become the backbone of American retirement savings.

How 401(k) Plans Work

Employees contribute a portion of their paycheck directly to their 401(k) account before taxes are withdrawn. This immediately reduces your taxable income—if you earn $50,000 and contribute $5,000 to your 401(k), you only pay taxes on $45,000 of income.

Most employers offer matching contributions, agreeing to contribute a certain amount (typically 3-6% of your salary) when you contribute to the plan. This represents free money. If your employer matches 50% of contributions up to 6% of your salary and you earn $50,000, contributing just $3,000 (6% of your salary) earns an additional $1,500 from your employer.

2024 contribution limits:

- Employees under 50: $23,000 annually

- Employees 50 and older: $30,500 annually (includes catch-up contribution)

Types of 401(k) Investments

Most 401(k) plans offer a selection of investment options, typically including:

- Target-date funds that automatically adjust allocation as you approach retirement

- Index funds tracking broad market indices like S&P 500

- Company stock (often available but risky to concentrate in)

- Bond funds for conservative allocation

- International funds for global diversification

For beginners, target-date funds provide the simplest approach—choose the fund matching your expected retirement year and let professional managers handle asset allocation.

Pros and Cons of 401(k) Plans

| Aspect | Advantages | Disadvantages |

|---|---|---|

| Contributions | Pre-tax, lowers taxable income | Limits on how much you can contribute |

| Employer match | Free money, immediate returns | Only available if employer offers it |

| Investment options | Limited selection predetermined by employer | May have high fees |

| Flexibility | Loans possible, hardship withdrawals exist | Early withdrawal penalties before 59½ |

| Portability | Can roll over when changing jobs | May lose employer match if you leave |

Best for: Employees with access to employer matching, especially those in higher tax brackets who benefit from immediate tax deductions.

Individual Retirement Accounts: IRA Options

Individual Retirement Accounts (IRAs) provide retirement savings options for those without employer-sponsored plans, those wanting to save beyond 401(k) limits, or those seeking different tax advantages. Two primary types exist: Traditional and Roth.

Traditional IRA

A Traditional IRA offers tax-deductible contributions in the year you make them, growing tax-deferred until withdrawal. When you retire and withdraw funds, those contributions and all investment gains are taxed as ordinary income.

Key features:

- 2024 contribution limit: $7,000 ($8,000 if 50 or older)

- Contributions may be tax-deductible depending on income and workplace retirement plan access

- Withdrawals must begin at age 73 (required minimum distributions)

- Early withdrawals before 59½ generally incur 10% penalty plus income taxes

Deductibility phases out for individuals covered by workplace retirement plans at incomes above $77,000 (single) or $123,000 (married filing jointly) in 2024.

Roth IRA

The Roth IRA flips the Traditional IRA tax structure—contributions are made with after-tax dollars (not deductible), but qualified withdrawals in retirement are completely tax-free. This includes both your original contributions and all investment growth.

Key features:

- 2024 contribution limit: $7,000 ($8,000 if 50 or older)

- Contributions are never tax-deductible

- No required minimum distributions during your lifetime

- Early withdrawals of contributions (not earnings) are penalty-free

- Earnings withdrawn before 59½ incur taxes and 10% penalty (with some exceptions)

Income limits apply—Roth IRA contributions phase out for single filers above $146,000 and married filers above $230,000 in 2024. High earners can use a “backdoor Roth” strategy, contributing to a non-deductible Traditional IRA and converting to Roth.

Traditional vs. Roth: Which Is Better?

| Factor | Traditional IRA | Roth IRA |

|---|---|---|

| Tax on contributions | Deductible now | Not deductible |

| Tax on withdrawals | Ordinary income | Tax-free |

| Required distributions | Yes, at 73 | None |

| Best for | Higher tax brackets now | Lower tax brackets now |

| Flexibility | More restricted | More flexible access |

General guidance: If you expect to be in a lower tax bracket in retirement than you are now, Roth accounts make more sense. If you’re currently in a high tax bracket, Traditional accounts provide more valuable upfront deductions.

The Power of Combining Accounts

Many Americans can and should utilize both 401(k) and IRA accounts simultaneously, maximizing their annual contribution capacity and tax advantages.

Recommended priority order:

- 401(k) up to employer match — This guarantees an immediate 100% return on your money

- Pay off high-interest debt — Credit card interest typically exceeds investment returns

- Maximize Roth IRA — Especially valuable for beginners in lower tax brackets

- Maximize 401(k) beyond match — Continue until you hit annual limits

- Consider taxable accounts — After maxing all retirement accounts

For example, a 25-year-old earning $50,000 with employer matching 50% up to 6% should first contribute at least $3,000 (6% of salary) to get the full $1,500 match. Next, contribute up to $7,000 to a Roth IRA. Then return to the 401(k) to maximize contributions beyond the match level.

Common Retirement Account Mistakes to Avoid

👤 Megan, 34, Marketing Manager, Chicago

“I started my career not contributing to my 401(k) because I wanted to pay off student loans faster. By the time I started at 28, I’d missed out on over $30,000 in employer matches and six years of compound growth. If I’d started with just 3% at 22, I’d have over $100,000 more today.”

Many beginners make similar mistakes that significantly impact their retirement readiness:

Mistake #1: Not starting because contributions feel too small

Even $50 monthly contributions matter enormously over decades. Starting at 22 with $50 monthly at 7% returns creates $115,000 by age 65. Waiting ten years to start requires $125 monthly to reach the same amount.

Mistake #2: Ignoring employer 401(k) matching

Employer matches are not optional benefits—they represent immediate returns that dwarf most investment performance. Always contribute at least enough to capture the full match.

Mistake #3: Investing too conservatively when young

Younger investors often make the mistake of choosing bond funds or stable value funds over stock funds. With decades until retirement, you can afford market volatility. Target-date funds automatically adjust risk as you age.

Mistake #4: Taking early withdrawals

Accessing retirement funds before 59½ typically triggers 10% penalties plus income taxes. While loans against 401(k) balances are sometimes necessary, they reduce your retirement savings and create repayment obligations.

Mistake #5: Not rebalancing periodically

Your ideal asset allocation changes as you age. Annual rebalancing ensures your portfolio maintains appropriate risk levels.

How to Open and Fund Your First Retirement Account

Getting started requires just a few steps:

For 401(k):

- Enroll during your employer’s open enrollment or upon hire

- Select your contribution percentage (aim for at least the full employer match)

- Choose your investments (target-date funds simplify this)

- Set up automatic contributions from each paycheck

For IRA:

- Open an account with a broker (Fidelity, Vanguard, Charles Schwab, and E*TRADE all offer IRAs)

- Fund the account (can transfer from bank account)

- Select investments (low-cost index funds recommended)

- Set up recurring contributions

Recommended starting contributions:

- Minimum: Enough to capture full employer 401(k) match

- Better: 10-15% of income toward retirement

- Ideal: Max out contribution limits ($23,000 for 401(k), $7,000 for IRA in 2024)

Expert Insights on Building Retirement Wealth

👤 Catherine McBride, CFP®, Partner at Carson Wealth Management

“New investors dramatically overestimate what they need to start. The biggest obstacle isn’t money—it’s getting started. Opening an account with $100 and setting up $25 monthly contributions builds the habit and gets your foot in the door. The contribution amounts can increase as income grows.”

👤 Derek H. Hanson, Professor of Personal Finance at Texas Tech University

“Compound interest works best over long time horizons. Someone who starts at 25 and stops at 35 will have more at 65 than someone who starts at 35 and contributes the same amount through age 65. Time in the market matters extraordinarily.”

Conclusion

Building retirement wealth begins with understanding your options and taking action. Employer-sponsored 401(k) plans with matching contributions provide the highest guaranteed return available—essentially free money that accelerates your savings trajectory. IRA accounts, particularly Roth IRAs for younger earners, offer flexibility and tax-free growth that taxable accounts cannot match.

The most important decision is simply to start. Whether you can contribute $50 monthly or $1,500 monthly, beginning now leverages time and compound interest in ways that waiting simply cannot replicate. As your career advances and income grows, increasing your contributions ensures your retirement savings keep pace with your lifestyle.

Future financial security is built in small, consistent steps taken today. Your older self will thank you for starting now.

Frequently Asked Questions

What is the best retirement account for a beginner with no employer plan?

If your employer doesn’t offer a 401(k) or matching, a Roth IRA is typically the best starting point. You can open one directly with any major brokerage, contributions are flexible, and the tax-free growth benefit is particularly valuable for beginners who expect higher future earnings.

Can I have both a 401(k) and an IRA?

Yes, you can and often should contribute to both. You can have one 401(k) through your employer plus one or more IRAs. Just be aware that Roth IRA contributions may be limited at higher income levels if you’re also contributing to a 401(k).

How much should I contribute to my retirement account as a beginner?

Start with whatever amount captures your full employer 401(k) match—this is non-negotiable. Then aim to contribute 10-15% of your income overall toward retirement. If that’s not possible, even small amounts like $50-100 monthly build the habit and compound significantly over time.

What happens if I withdraw money early from my retirement account?

Generally, withdrawals before age 59½ incur a 10% penalty plus income taxes. Exceptions exist for certain hardships, first-time home purchases (up to $10,000), and qualified education expenses. Roth IRA contributions can be withdrawn anytime tax-free, though earnings may be penalized.

Should I choose a Traditional or Roth 401(k)?

If you’re in a higher tax bracket now and expect lower taxes in retirement, Traditional 401(k) contributions make more sense. If you’re in a lower tax bracket now and expect higher taxes later, Roth 401(k) contributions provide better long-term value. Many plans now offer both options.