10Views 0Comments

Beginner Guide to Budget Personal Finance That Works

Personal finance doesn’t have to be complicated. Whether you’re trying to pay off debt, build an emergency fund, or simply understand where your money goes each month, a solid budget is the foundation of financial health. This guide breaks down everything you need to know to create a budget that actually works—without complicated spreadsheets or restrictive deprivation.

Why Budgeting Matters More Than You Think

Budgeting isn’t about restricting yourself from spending money. It’s about making intentional choices with the money you already earn. According to a 2023 survey by Bankrate, only 41% of Americans maintain a monthly budget, yet those who do report significantly lower financial stress and higher savings rates than those who don’t.

The reality is simple: without a budget, you likely have no clear picture of your spending habits. You might feel like you “should” be saving more, but without tracking expenses, you’re essentially guessing. A budget provides clarity, control, and the ability to work toward specific financial goals—whether that’s buying a home, retiring early, or simply having enough cushion to handle unexpected expenses.

Here’s what makes budgeting essential for Americans specifically. The median American household income was approximately $75,000 in 2023, according to the U.S. Census Bureau. Yet, Federal Reserve data shows that nearly 40% of adults couldn’t cover a $400 emergency expense with cash or its equivalent. This gap between income and financial security exists largely because many people haven’t developed a budgeting system that works for their lifestyle.

Understanding the Core Budgeting Methods

Not all budgeting approaches work for everyone. The best method depends on your income stability, spending habits, and personal preferences. Here are the most effective systems to consider.

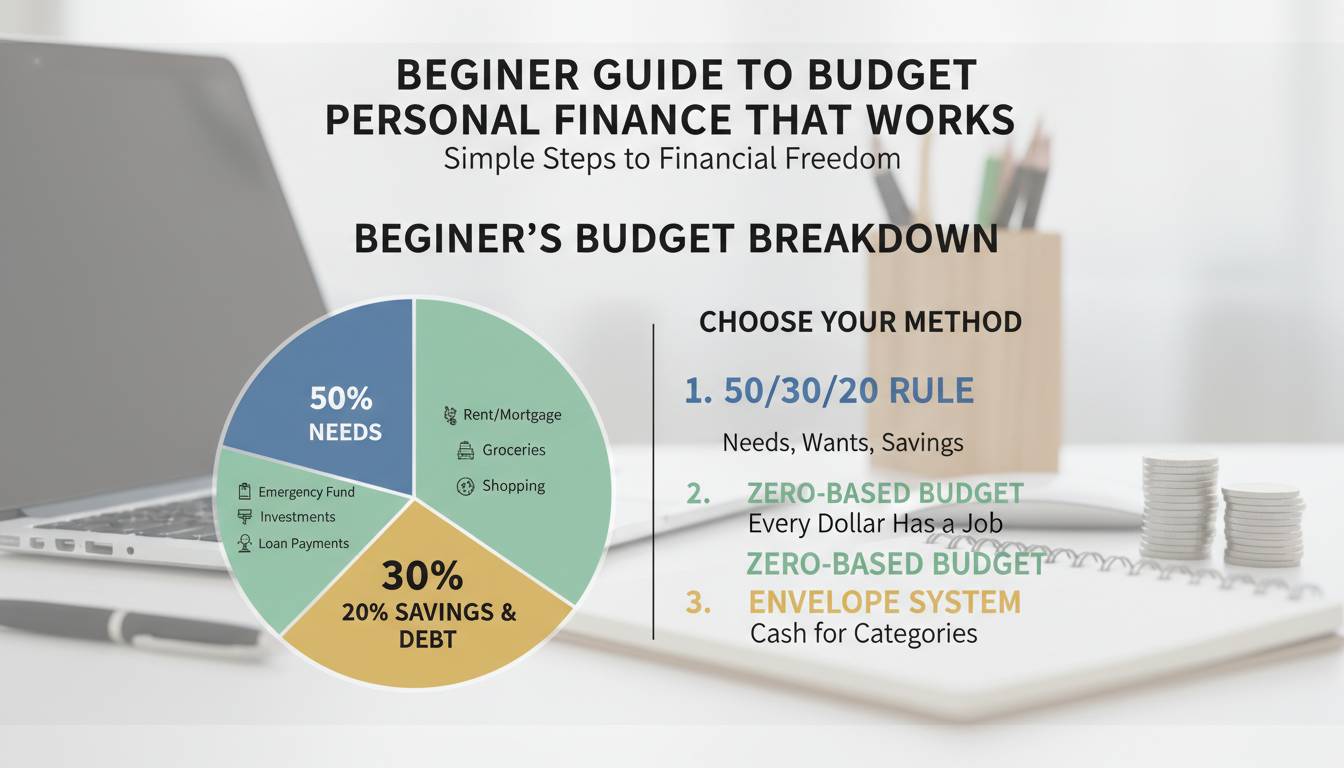

The 50/30/20 Rule

This method divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment.

- Needs include housing, utilities, groceries, insurance, minimum debt payments, and transportation to work.

- Wants encompass dining out, entertainment, hobbies, subscriptions, and non-essential purchases.

- Savings and debt covers emergency fund contributions, retirement account deposits, extra debt payments, and investment contributions.

The 50/30/20 rule provides flexibility while ensuring you’re consistently directing money toward your future. It’s particularly effective for beginners because it doesn’t require detailed tracking of every single purchase.

Zero-Based Budgeting

Zero-based budgeting gives every dollar a job. You start with your income and subtract all expenses, savings, and investments until you reach zero. This method gained popularity through Dave Ramsey’s financial philosophy and forces you to account for every single dollar before the month begins.

The process works like this: list your income, then allocate money to each category until you have $0 remaining. The key is that “savings” is an expense category, not an afterthought. If you have $3,000 in monthly income and allocate $1,500 to needs, $900 to wants, and $600 to savings, you’ve reached zero.

This approach works exceptionally well for people who tend to spend whatever is available in their account. It requires more time and attention initially—typically 30-60 minutes per month—but creates strong financial awareness.

The Envelope System

This cash-based method involves dividing money into physical envelopes labeled with spending categories. You take cash from the appropriate envelope when making purchases, and when an envelope is empty, you stop spending in that category.

While digital alternatives exist, the physical envelope system works because it makes spending tangible. Watching cash disappear from an envelope creates a psychological impact that swiping a debit card doesn’t replicate. According to research from the Journal of Consumer Research, people spend 12-18% less when using cash versus credit cards.

Step-by-Step: How to Create Your First Budget

Creating a budget from scratch can feel overwhelming. Breaking it into manageable steps makes the process achievable.

Step 1: Calculate Your True Monthly Income

Start with your net income—the amount you actually take home after taxes and deductions. If you’re salaried, this is straightforward. If you’re hourly or have variable income, use your lowest-earning month from the past year as your baseline, then budget conservatively.

Include all income sources: primary salary, side hustles, rental income, alimony, or any regular payments you receive. Don’t forget annual or quarterly payments—break these down into monthly amounts.

Step 2: List Fixed Expenses

Fixed expenses remain constant each month. Write down:

- Rent or mortgage payment

- Car payment

- Insurance premiums (auto, health, life)

- Student loan payments

- Child support or alimony

- Subscription services

- Phone and internet bills

Add these up. This is your baseline monthly commitment.

Step 3: Track Variable Expenses for One Month

Before allocating money to variable categories like groceries, gas, and entertainment, actually track what you spend for 30 days. Use your bank’s app, a spreadsheet, or apps like Mint, YNAB, or Personal Capital.

After one month, you’ll have accurate data about your actual spending. Most people are surprised by how much they spend on dining out, coffee, or streaming services.

Step 4: Categorize and Set Limits

Group your variable expenses into categories and set realistic limits. Be honest about your habits. If you currently spend $400 monthly on groceries, setting a $200 limit will likely fail. Start with a slightly reduced number—say $350—and adjust gradually.

Step 5: Choose Your Allocation Method

Decide how you’ll distribute money to each category. The methods discussed earlier (50/30/20, zero-based, or envelope system) all work. Choose the one that matches your personality and lifestyle.

Step 6: Review and Adjust Monthly

Your first budget won’t be perfect. That’s normal. Review your spending at the end of each month. Did you overspend in some categories? Did you underestimate others? Adjust for the following month.

Essential Budget Categories Every Beginner Needs

Certain categories appear in nearly every successful personal budget. Don’t skip these when setting up your system.

Emergency Fund

Financial experts recommend saving three to six months of living expenses in an easily accessible account. Start with a smaller goal—$1,000—then build toward the full recommendation. This fund protects you from going into debt when unexpected expenses arise.

Retirement Contributions

If your employer offers a 401(k) match, contribute at least enough to capture the full match—it’s free money. For 2024, you can contribute up to $23,000 to a 401(k) and $7,000 to an Individual Retirement Account (IRA). Starting early matters enormously due to compound interest.

Debt Payments

Beyond minimum payments, allocate extra money toward high-interest debt. Credit card debt averaging 20%+ interest should be prioritized. After paying off one card, roll that payment to the next card—the “debt snowball” method works because it creates momentum.

Healthcare and Insurance

Don’t budget for healthcare based on your current health. Include insurance premiums, out-of-pocket maximums, and regular expenses like prescriptions or glasses. Health insurance deductibles can range from $500 to $6,000 or more—budget accordingly.

Common Budgeting Mistakes to Avoid

New budgeters frequently make the same errors. Learning about these pitfalls now saves time and frustration.

Setting Unrealistic Goals

Budgeting for $50 monthly groceries when you currently spend $600 will fail. Make incremental changes. Reduce spending by 10-15% initially, then adjust as habits shift.

Forgetting Irregular Expenses

Annual subscriptions, car registration fees, and holiday gifts don’t happen monthly. Create “sinking funds”—separate savings accounts for irregular expenses. Save $50 monthly for holiday gifts instead of scrambling in December.

Treating Budget as Restriction

If your budget feels punishing, you won’t stick with it. Build in flexibility. Allow categories for entertainment and dining out. The goal is sustainable change, not temporary deprivation.

Not Budgeting for Fun

A budget that eliminates all pleasure spending is unsustainable. Allocate money for things you enjoy. This prevents “budget burnout” and reduces the likelihood of abandoning your plan entirely.

Ignoring the Numbers

Simply opening a banking app isn’t budgeting. You need active engagement—reviewing categories, adjusting allocations, and making conscious decisions about spending.

The Best Budgeting Tools and Resources

Technology makes budgeting easier than ever. Here are tools that work well for beginners.

YNAB (You Need A Budget)

This popular zero-based budgeting app costs $14.99 monthly or $109 annually. It emphasizes assigning every dollar a job and offers extensive educational resources. YNAB users report saving an average of $600 in their first two months, according to the company.

Mint

Free to use, Mint automatically categorizes transactions from linked accounts. It’s excellent for tracking spending without manual entry. The app displays your net worth, tracks bill payments, and sends alerts for unusual activity.

Personal Capital

Best for those interested in investment tracking, Personal Capital provides tools for budgeting alongside investment analysis. The budgeting features are free, while wealth management services carry fees.

Spreadsheets

Many people succeed with simple spreadsheet budgets. Create columns for income, categories, budgeted amounts, actual amounts, and variance. Update weekly. This hands-on approach builds strong financial awareness.

Building Long-Term Financial Habits

Budgeting succeeds when it becomes habitual. These strategies help maintain momentum.

Automate Everything

Set up automatic transfers to savings accounts and automatic bill payments. When saving happens automatically, you remove the decision to skip it.

Use the 24-Hour Rule

Before non-essential purchases over a certain amount (say, $50), wait 24 hours. This cooling-off period reduces impulse buying.

Celebrate Small Wins

Reached your savings goal for the month? Acknowledge it. Financial progress takes time—recognize milestones along the way.

Adjust Annually and During Life Changes

Review your budget when circumstances change—new job, marriage, having children, or moving. Your budget should evolve with your life.

Frequently Asked Questions

How much money should I save each month?

Financial experts recommend saving 20% of your income if possible, but starting with even 5% builds the habit. If you’re new to budgeting, begin with whatever amount feels manageable—even $25 per paycheck—and increase gradually. The key is consistency rather than perfection.

What if my income is irregular?

Base your budget on your lowest monthly income. For variable income earners, create a “floor” income figure and only budget that amount. When you earn more, treat the excess as bonus savings rather than spending money. This approach prevents overspending during high-earning months followed by hardship during low-earning periods.

Should I pay off debt or save first?

Prioritize building a small $1,000 emergency fund before aggressive debt payoff. This prevents adding new debt when unexpected expenses arise. After establishing this mini-emergency fund, focus extra money on high-interest debt while maintaining minimum payments on all other debts.

How long does it take to see results from budgeting?

Many people see immediate benefits within the first month—reduced stress, clearer financial direction, and awareness of spending habits. Significant financial milestones like building a full emergency fund or paying off credit cards take longer, typically six months to several years depending on your situation and income.

Is it okay to change my budget method?

Absolutely. Your first budgeting system probably won’t be your last. If a method feels restrictive or complicated, try another approach. The best budget is one you can actually follow consistently. Experiment during your first three to six months to find what works for your personality and lifestyle.

Conclusion

Budget personal finance comes down to one principle: know where your money goes and decide intentionally where you want it to go. The method you choose matters less than your commitment to following it consistently.

Start simple. Calculate your income, track your expenses for one month, and choose one budgeting method to try. You don’t need perfect finances—you need a starting point and willingness to adjust.

The best time to start budgeting was yesterday. The second-best time is today. Your future self will thank you for the financial clarity and security you’re building right now.