9Views 0Comments

Interest Rates Rising? Here’s What Happens to Stocks

When the Federal Reserve raises interest rates, stock markets typically experience turbulence. Understanding this relationship is crucial for any investor navigating changing monetary policy. This guide explains the mechanics behind rate changes and their effects on different sectors of the stock market.

The Basic Relationship Between Interest Rates and Stocks

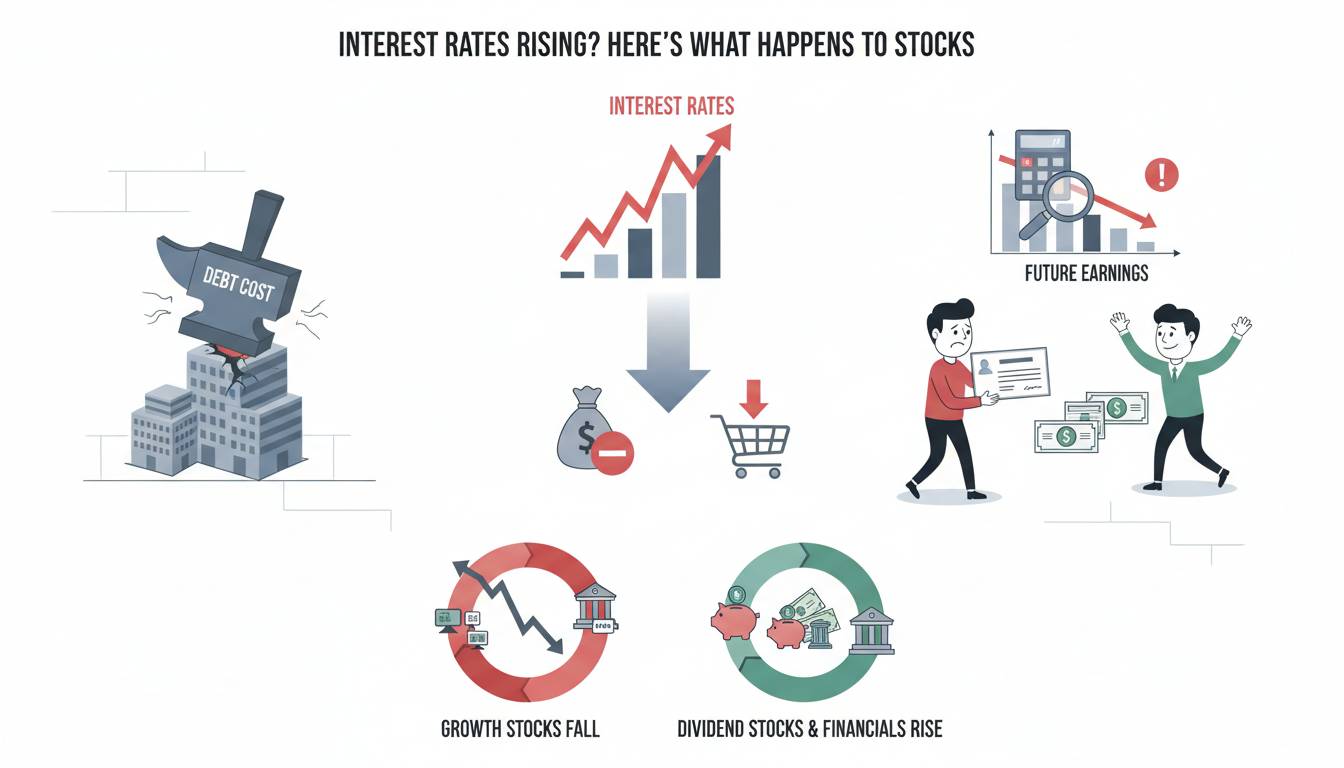

Interest rates and stock prices generally move in opposite directions. When the Federal Reserve raises the federal funds rate, it becomes more expensive for companies to borrow money and more attractive for investors to put money in savings accounts and bonds. This shift in the investment landscape causes stock prices to adjust, often downward.

The fundamental reason lies in how stocks are valued. Investors price stocks based on expected future earnings, discounted back to present value using an interest rate. When interest rates rise, the discount rate increases, making those future earnings worth less today. This mathematical relationship means that rate hikes directly reduce the present value of stocks, particularly those valued for their growth potential rather than current profits.

Additionally, higher interest rates increase borrowing costs for businesses. Companies carrying debt—most large corporations do—face higher interest payments on their loans. These increased costs compress profit margins and can slow growth plans, which investors typically penalize by lowering stock valuations.

Which Sectors Suffer Most When Rates Rise

Not all stocks respond equally to interest rate increases. Growth stocks and interest-sensitive sectors typically feel the harshest impact.

Technology and growth stocks often decline sharply because their valuations rely heavily on earnings expected years in the future. When discount rates rise, those distant earnings become significantly less valuable. The NASDAQ Composite historically experiences larger percentage drops than the broader market during rate hike cycles.

Real estate investment trusts (REITs) suffer because higher rates increase the cost of financing property acquisitions while making dividend-paying real estate less attractive compared to bonds offering higher yields. Real estate stocks consistently underperform during tightening cycles.

Utilities face similar pressures. These companies typically carry significant debt to fund infrastructure and depend on steady, predictable earnings that become less attractive when risk-free returns increase. The utilities sector frequently ranks among the worst performers during rate hike periods.

Financial stocks present a more complex picture. Banks and financial institutions benefit from higher rates because they can charge more for loans while the interest they pay on deposits increases less dramatically. This net interest margin expansion can boost bank profitability, though market uncertainty often tempers initial gains.

Historical Examples of Rate Hikes and Stock Performance

Examining past Federal Reserve tightening cycles reveals consistent patterns, though every situation differs.

During the 2018 rate hike cycle under Federal Reserve Chair Jerome Powell, the S&P 500 experienced a 20% decline from its peak before recovering. The technology sector dropped significantly as growth concerns intensified.

The 2004-2006 hiking cycle saw more modest market reactions, with the S&P 500 actually gaining ground despite multiple rate increases. This period demonstrated that stock performance depends on multiple factors beyond just interest rates, including economic growth and corporate earnings.

The aggressive 2022 rate hikes—the most aggressive in decades—saw the S&P 500 decline approximately 19% for the year. Technology stocks bore the brunt, with the NASDAQ falling roughly 33%. However, financial stocks showed resilience as net interest margins expanded.

These examples illustrate that while rate hikes typically create headwinds, the magnitude and duration of market impact depend on broader economic conditions and whether the economy achieves a “soft landing.”

How Bond Yields Compete With Stocks

When interest rates rise, bond yields typically increase as well. This creates direct competition for investor dollars between stocks and fixed-income securities.

Treasury bonds, considered risk-free investments, become more attractive as their yields climb. When 10-year Treasury yields rise above 4% or 5%, dividend-paying stocks become less appealing by comparison. Income-focused investors often rotate from stocks into bonds, particularly during periods of economic uncertainty.

Corporate bonds also become more expensive to issue during rate hikes, forcing companies to delay or reduce bond offerings. This constrained financing can slow mergers, acquisitions, and expansion plans, further impacting stock valuations.

The yield spread between stocks and bonds—often measured through the equity risk premium—narrows during rate hike cycles. When bonds offer competitive returns with less volatility, rational investors often reduce stock allocations, creating selling pressure that drives prices lower.

The Role of Investor Psychology and Expectations

Markets are forward-looking, which means investor expectations often matter more than actual rate changes themselves. The Federal Reserve’s communications about future policy intentions can move markets more than the rate decisions themselves.

Stocks frequently decline in anticipation of rate hikes rather than after them. When the Fed signals tightening, investors adjust portfolios preemptively. This phenomenon, known as “pricing in” rate increases, explains why markets sometimes rise after a rate hike announcement—the bad news has already been absorbed.

Conversely, markets can rally during rate cut cycles well before the cuts actually occur. This expectation-driven behavior means that timing investments around Fed communications requires careful attention to Federal Reserve statements and meeting minutes.

Volatility typically increases during rate transition periods. The uncertainty about how high rates will go and how long they’ll stay elevated creates unpredictable trading patterns. The Cboe Volatility Index (VIX) often spikes during active Fed policy meetings.

Strategies for Investors During Rising Rate Environments

Investors can take several approaches to navigate rising interest rate environments.

Focus on quality becomes essential. Companies with strong balance sheets, low debt levels, and consistent cash flows tend to outperform during tightening cycles. These businesses can weather higher borrowing costs without compromising their operations.

Consider value stocks over growth stocks. Value companies that generate profits today rather than promising future earnings become relatively more attractive when discount rates rise. Sectors like healthcare, consumer staples, and energy often provide defensive characteristics.

Review fixed-income allocations. While bond prices fall during rate increases, holding bonds to maturity ensures you receive your principal back. Longer-duration bonds experience larger price declines than short-term securities.

Maintain diversification across sectors and asset classes. While some sectors suffer, others benefit from higher rates. A diversified portfolio can smooth returns during volatile periods.

Dollar-cost averaging remains prudent during uncertain periods. Rather than timing market movements, consistently investing over time reduces the risk of making poor timing decisions.

The Long-Term Perspective on Rates and Stocks

Despite short-term turbulence, stocks have historically generated positive returns over longer periods, even through multiple rate cycle transitions.

The Federal Reserve has raised rates numerous times since the 1950s, yet the S&P 500 has produced roughly 10% average annual returns over many decades. This long-term upward trajectory reflects the ability of successful companies to grow earnings and adapt to changing financial conditions.

What’s crucial is understanding that rate changes are one of many factors affecting stock prices. Economic growth, corporate earnings, geopolitical events, and technological change all influence market movements. Focusing exclusively on interest rates provides an incomplete picture of the complex forces driving stock valuations.

Frequently Asked Questions

Do stocks always go down when interest rates rise?

No, stocks do not always decline when interest rates rise. While there’s generally an inverse relationship, stocks can rise during or after rate hikes if corporate earnings remain strong, economic growth continues, or if the rate increases are perceived as signs of a healthy economy. The 2004-2006 period is an example where stocks advanced despite multiple rate increases.

How long do stocks typically decline after interest rate increases?

There’s no set timeline for market recovery after rate increases. Some markets recover within months if the economy adapts successfully. In other cases, declines can persist for a year or longer, particularly if the Fed maintains restrictive policy to combat inflation. Historical examples show significant variation in recovery times.

Should I sell stocks when interest rates are rising?

Selling stocks during rate increases depends on your individual circumstances, risk tolerance, and investment timeline. Short-term traders might reduce exposure to interest-sensitive sectors, while long-term investors often benefit from staying invested and weather short-term volatility. Consider consulting a financial advisor for personalized guidance.

Which stocks perform best during rising interest rates?

Financial stocks, particularly large banks, often benefit from rising rates through expanded net interest margins. Consumer staples companies tend to be relatively resilient because people continue purchasing essential goods regardless of rate conditions. Energy companies with strong cash flows can also perform relatively well.

How do expected rate changes affect stocks compared to actual rate changes?

Expected or anticipated rate changes typically have larger market impacts than the actual rate decisions themselves. Markets “price in” anticipated changes gradually, while the actual announcement often creates less movement because expectations have already been incorporated. Federal Reserve forward guidance and economic projections often move markets more than the rate decision itself.

What’s the equity risk premium and why does it matter during rate changes?

The equity risk premium represents the additional return investors expect to earn by holding stocks rather than risk-free assets like Treasury bonds. When interest rates rise, this premium typically shrinks, making stocks less attractive relative to bonds. Investors demand higher stock prices to compensate for the increased risk, which can pressure valuations during rate hike cycles.