4Views 0Comments

What Happens to Unclaimed Money in Bank Accounts | Full Guide

Every year, millions of dollars in bank accounts go unclaimed across the United States. Accounts become inactive for numerous reasons—account holders relocate without forwarding addresses, pass away without estate planning, or simply forget about old accounts. When financial institutions cannot locate account owners or their heirs, these funds undergo a legal process called escheatment. Understanding what happens to unclaimed money in bank accounts helps you protect your own assets and potentially recover funds you didn’t know you were owed.

What Qualifies as an Unclaimed Bank Account

An unclaimed bank account typically refers to any deposit account that has had no owner activity or contact for a specified period, usually one to five years depending on the type of account and state regulations. This inactivity period triggers the dormancy classification, but it doesn’t immediately result in the account being turned over to the state.

Several scenarios lead to accounts becoming unclaimed. A common example involves account holders who move and never update their contact information with their bank. When statements become undeliverable and the bank cannot reach the customer through reasonable efforts, the account enters dormancy. Another frequent occurrence happens when account holders pass away without designating beneficiaries or leaving clear estate instructions. Family members may be unaware of the account’s existence, and without proper estate administration, the funds can eventually escheat to the state.

The definition of “inactivity” varies by financial institution and account type. Generally, any of the following actions can reset the dormancy clock: logging into online banking, making a transaction, updating contact information, or responding to bank communications. Checking accounts, savings accounts, money market accounts, certificates of deposit (CDs), and even safe deposit boxes can become unclaimed if left untouched beyond the dormancy period.

The Escheatment Process Explained

Escheatment is the legal process through which unclaimed property transfers from private institutions to state government custody. This process exists to protect abandoned funds and ensure they remain available for rightful owners or their heirs to claim. While the specific procedures vary by state, the fundamental framework follows federal guidelines established under the Uniform Unclaimed Property Act.

When an account reaches the statutory dormancy period, the financial institution is legally required to attempt to locate the owner before transferring the funds. Banks must conduct diligent searches, which typically include sending written notices to the last known address, searching internal records for alternative contact information, and cross-referencing against other customer databases. Only after these efforts fail does the institution remit the funds to the state where the account was held.

The timeline for escheatment varies significantly across states. Some states require accounts to be dormant for just two years, while others mandate five years or longer. Certain account types, such as CDs or trust accounts, may have different dormancy periods than regular checking or savings accounts. The financial institution reports and remits unclaimed funds to the appropriate state usually within 30 to 60 days following the dormancy period’s expiration.

Interestingly, escheatment does not mean the bank or state permanently keeps the money. The funds remain claimable indefinitely in most states, and rightful owners can recover their property at any time by proving their identity and relationship to the account. The state holds these funds in trust, using them for various purposes in some states while the money awaits legitimate claims.

State Unclaimed Property Programs

Each state maintains an unclaimed property division, typically housed within the state treasury or comptroller’s office. These programs serve as centralized repositories for all unclaimed funds transferred from financial institutions, businesses, and other entities within state boundaries. The National Association of Unclaimed Property Administrators (NAUPA) coordinates efforts between states and maintains the database accessible through Unclaimed.org.

The amount of money held in state unclaimed property programs is substantial. According to estimates from various state treasurers, collectively state programs hold over $100 billion in unclaimed funds. This figure represents decades of accumulated dormant accounts, forgotten utility deposits, uncashed checks, and unclaimed insurance benefits. California, New York, Texas, and Florida typically lead in total unclaimed funds due to their large populations and diverse economies.

State programs differ in how they use unclaimed funds. Some states deposit the money into their general funds and use it for governmental operations, treating unclaimed property as legitimate revenue. Other states maintain separate funds and only use the interest earned on these balances for operations, keeping the principal available for claims. When legitimate owners file claims, the state pays from the fund regardless of how many years have passed or how the money has been used in the interim—this is a legal obligation that states must honor.

The transparency of state programs also varies. Most states provide online searchable databases where citizens can check if they have unclaimed property. However, the frequency of database updates, the types of property covered, and the ease of filing claims differ substantially between states. Some states require notarized claims, extensive documentation, or even in-person appearances, while others offer streamlined online processes.

How to Find Unclaimed Money

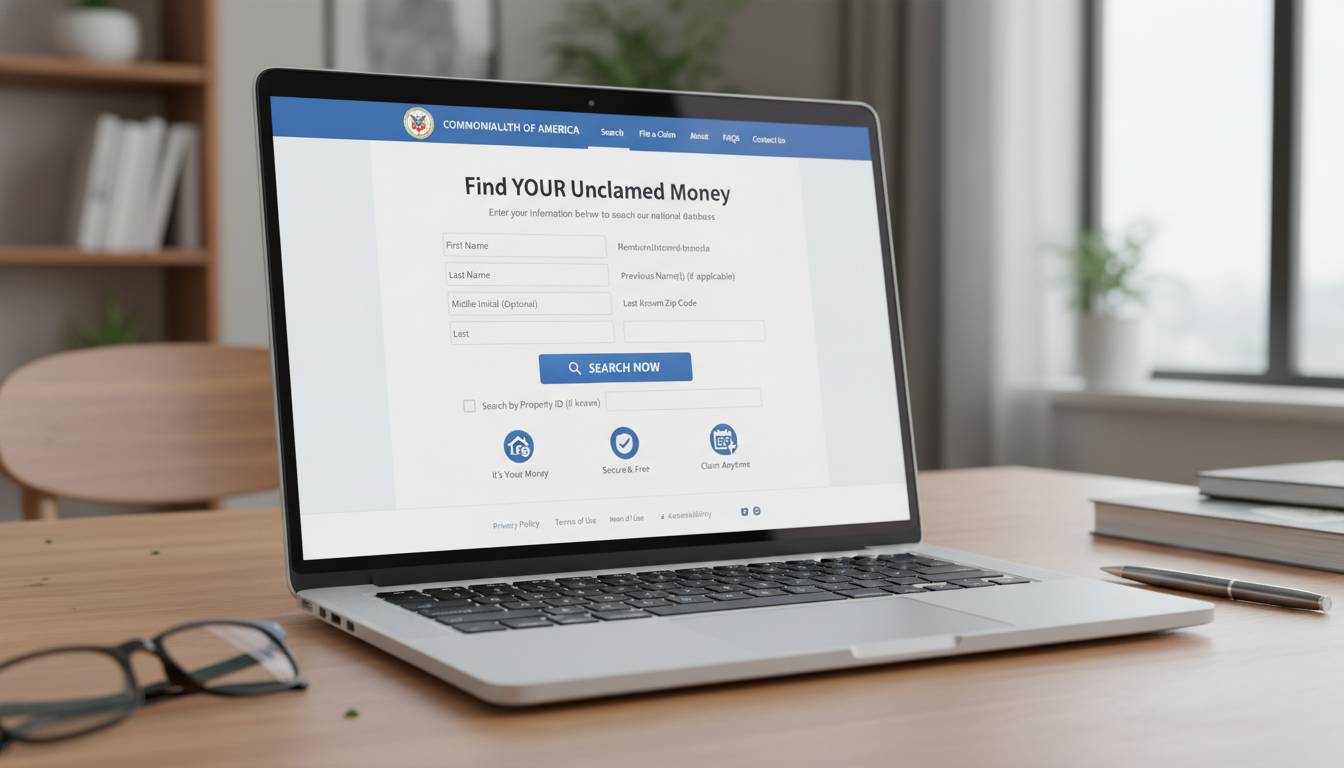

Finding unclaimed money requires searching multiple databases and resources, as no single source contains all unclaimed funds. The most effective approach begins with the state’s unclaimed property database where you reside, then expands to other states where you have lived, worked, or owned property.

The website Unclaimed.org serves as the official portal for state unclaimed property programs. Managed by NAUPA, this site provides links to each state’s official unclaimed property database. You can search by your name, and some states offer searches by business name or other identifiers. Be thorough in your search—try variations of your name, including maiden names or previous legal names, as records may be filed under different variations.

Beyond state programs, other valuable resources exist. The Internal Revenue Service maintains a database of unclaimed tax refunds, accessible through the “Where’s My Refund?” tool or by contacting the IRS directly. The Department of Labor’s database includes unclaimed pension benefits from terminated retirement plans. The National Association of Insurance Commissioners hosts a policy locator service for unclaimed life insurance benefits. Additionally, the FDIC maintains records of failed bank accounts, though most of these funds have been transferred to state programs.

When searching, cast a wide net. Search for common misspellings of your name, as clerical errors frequently occur in record-keeping. Search for old addresses where you previously lived. If you have deceased family members, search for their names as well—you may be entitled to inherit unclaimed funds from their accounts. Consider searching for any businesses you have owned, as business accounts can also become unclaimed.

How to Claim Unclaimed Funds

Successfully claiming unclaimed money requires providing documentation that proves your identity and your right to the funds. The specific requirements vary by state and by the type of property being claimed, but certain elements remain consistent across most programs.

The initial claim process typically begins with verifying your identity. Most states require a copy of a valid government-issued photo ID, such as a driver’s license or passport. For property belonging to deceased individuals, you must document your relationship to the deceased and your authority to claim on their behalf. This may require death certificates, wills, probate court documents, or letters of administration from the estate.

Supporting documentation for the claim itself varies based on the property type. If claiming a bank account, you might need to provide the account number (if known), approximate dates of the account, the bank name, and any other identifying information. Supporting documents could include old bank statements, correspondence with the financial institution, or affidavits from family members who recall the account.

Most states now offer online claim submission, though some still require paper forms. The processing time varies widely—some states process claims within weeks, while others may take several months. Complex claims involving estates, businesses, or multiple parties typically take longer to verify. Once approved, payment methods include check, direct deposit, or in some cases, electronic transfer to a designated account.

Be cautious of third-party companies that offer to find and claim your unclaimed money for a fee. While some legitimate businesses provide this service, many charge unnecessary fees ranging from 10% to 50% of the recovered funds. The state programs themselves are free to use, and the claim process, while sometimes cumbersome, does not require professional assistance in most straightforward cases.

Protecting Your Own Accounts from Escheatment

Preventing your accounts from becoming unclaimed requires maintaining regular contact with your financial institutions and keeping your information current. Simple habits can ensure your hard-earned money remains accessible and doesn’t end up in state custody.

Always keep your contact information updated with your bank. This includes your mailing address, email address, and phone number. Most banks now offer online banking where you can verify and update your information at any time. When you move, notify all your financial institutions immediately—don’t wait for problems to arise.

Engage with your accounts regularly. Even minimal activity prevents an account from becoming dormant. Set up automatic transfers between accounts, schedule recurring payments, or simply log into your online banking periodically. Even checking your balance and then logging out counts as activity in most institutions’ systems.

Maintain beneficiary designations on accounts that allow them. Payable-on-death (POD) designations on bank accounts and transfer-on-death (TOD) registrations on investment accounts allow funds to pass directly to designated individuals without going through probate. This not only simplifies estate administration but also ensures your money goes where you intend rather than becoming unclaimed.

Finally, maintain records of all your financial accounts. Keep a secure document listing your bank accounts, investment accounts, insurance policies, and other financial assets. Share this information with a trusted family member or store it in a secure location accessible to your executor. This ensures someone knows where to find your accounts if something happens to you.

Frequently Asked Questions

How long does it take for a bank account to become unclaimed?

The time period varies by state and account type, but most states require three to five years of inactivity before an account is considered abandoned. Some states have shorter periods for certain account types, while others may have longer requirements. Contact your specific state’s unclaimed property office for exact timeframes.

Can I lose my money if it escheats to the state?

No, you cannot permanently lose your money. Once funds escheat to the state, they remain claimable indefinitely in most jurisdictions. You can file a claim at any time to recover your property, provided you can prove your identity and ownership. Some states may have limitations on interest or may have used the funds, but the principal amount remains recoverable.

Does the bank notify me before escheatment?

Federal regulations require banks to make reasonable efforts to contact account holders before escheating funds. This typically includes sending notices to the last known address. However, if you have moved without updating your address, you may not receive these notices. This is why keeping your contact information current with your bank is essential.

Are there fees to claim unclaimed money from the state?

State unclaimed property programs are free to use. You should never pay fees to search for or claim your own money through official state programs. Be wary of third-party companies charging upfront fees—these are often unnecessary and may be scams. File your own claim directly through your state’s unclaimed property office.

What happens to unclaimed money if no one claims it?

In most states, unclaimed funds remain in the state unclaimed property fund indefinitely until claimed. Some states use the funds for government operations after a certain period, but they maintain a legal obligation to pay legitimate claims. The money doesn’t disappear—it stays available for rightful owners or heirs to claim.

How can I prevent my accounts from being escheated?

Keep your contact information current with your bank, maintain regular account activity, ensure beneficiary designations are up to date, and keep personal records of all financial accounts. Even small transactions or logins prevent accounts from becoming dormant.

Conclusion

Unclaimed money in bank accounts represents a significant issue affecting millions of Americans each year. While the escheatment process ensures these funds are protected rather than simply lost, navigating the recovery process can be time-consuming and confusing. The good news is that recovering unclaimed funds is free, straightforward in most cases, and available regardless of how much time has passed.

The most important steps you can take are proactive: keep your banking information current, maintain regular account activity, and maintain records of your financial accounts. These simple habits protect your assets from becoming unclaimed in the first place. Equally important, take time to search state unclaimed property databases—you may be pleasantly surprised to find forgotten funds waiting for you. With billions of dollars sitting in state unclaimed property offices, the chances of finding unclaimed money are better than you might think.