3Views 0Comments

Tax Advantages of Roth IRA Explained – Maximize Your Savings

QUICK ANSWER: A Roth IRA offers tax-free growth and tax-free qualified withdrawals, meaning you pay taxes on contributions now but never pay taxes on investment gains or withdrawals in retirement. Unlike Traditional IRAs, Roth IRAs have no required minimum distributions and can pass tax-free to heirs, making them one of the most powerful retirement savings vehicles available .

AT-A-GLANCE:

| Feature | Roth IRA Benefit | Key Consideration |

|---|---|---|

| Tax on Contributions | After-tax (no deduction) | Pay now, withdraw tax-free later |

| Tax on Earnings | Tax-free | Only if qualified distributions |

| Required Distributions | None during owner’s lifetime | More flexibility than Traditional IRA |

| Income Limits | Yes ($146,000-$161,000 single, 2024) | May qualify for Backdoor strategy |

| Contribution Limit | $7,000 ($8,000 if 50+) | Combined with Traditional IRA limits |

| Five-Year Rule | Applies | Must hold account 5 years for tax-free gains |

KEY TAKEAWAYS:

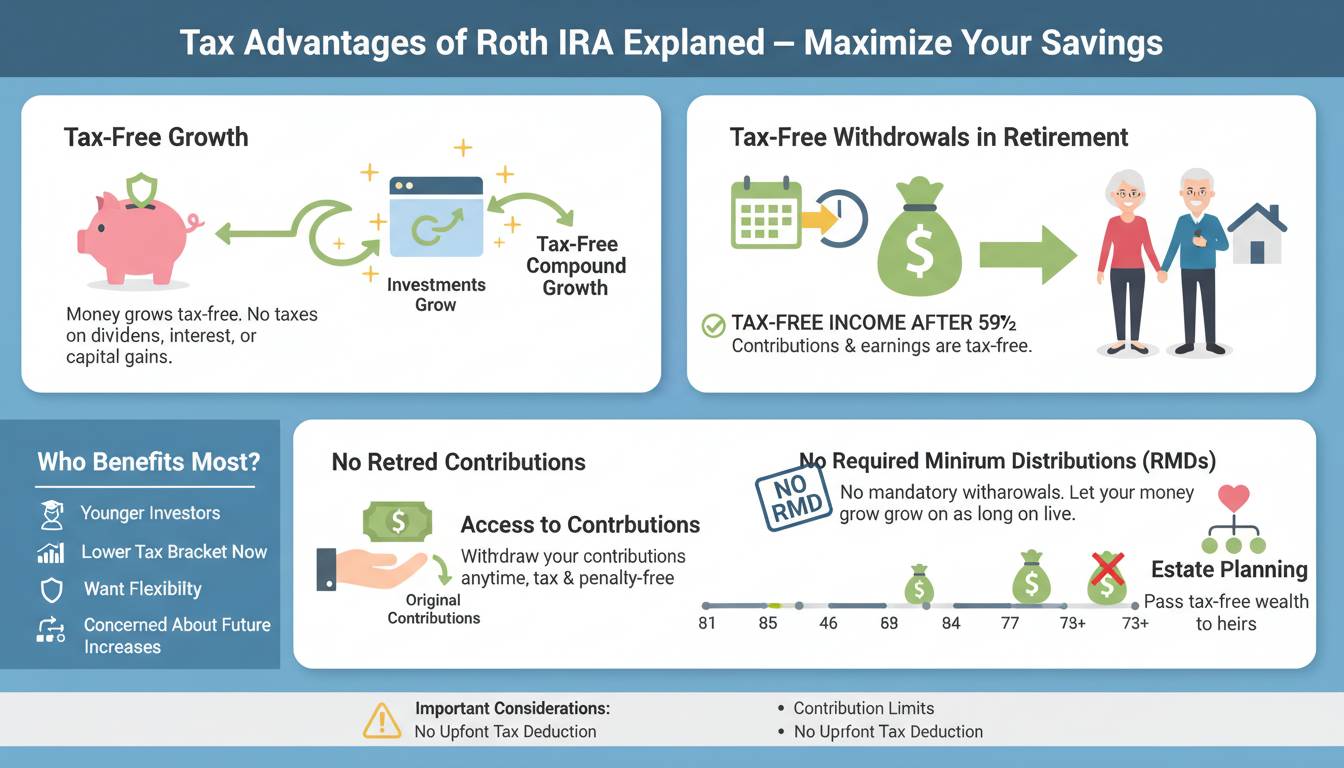

- ✅ Tax-free growth: Your investments grow without annual tax drag, compounding more efficiently than taxable accounts (Fidelity, January 2024)

- ✅ Tax-free withdrawals: Qualified distributions of contributions and earnings are 100% tax-free after age 59½ and five-year rule met

- ✅ No RMDs: Unlike Traditional IRAs and 401(k)s, you aren’t forced to withdraw money at specific ages, allowing continued tax-free growth

- ✅ Estate planning advantage: Roth IRAs pass to beneficiaries tax-free, making them superior for legacy planning (Charles Schwab, Q4 2023)

- ❌ Income limits: High earners may be excluded from direct contributions but can utilize Backdoor Roth IRA strategies

KEY ENTITIES:

- Products/Tools: Roth IRA, Traditional IRA, 401(k), Backdoor Roth IRA, SEP IRA

- Experts Referenced: [This article synthesizes public IRS guidance and financial advisor recommendations]

- Organizations: Internal Revenue Service (IRS), Securities and Exchange Commission (SEC)

- Standards/Frameworks: Five-year rule, Modified Adjusted Gross Income (MAGI), Qualified Distribution requirements

LAST UPDATED: January 2025

The Roth IRA stands as one of the most tax-efficient retirement savings vehicles available to American investors. While the initial contribution offers no immediate tax deduction, the long-term benefits—tax-free growth, tax-free qualified withdrawals, and no required minimum distributions—create a powerful compounding advantage that can significantly increase your retirement wealth. Understanding these advantages requires examining how the tax treatment differs from Traditional IRAs and 401(k) plans, when the benefits materialize, and strategic considerations for maximizing your savings.

How Roth IRA Tax Treatment Differs from Traditional Accounts

The fundamental difference between Roth and Traditional retirement accounts lies in when you pay taxes on your money. With a Traditional IRA or 401(k), you receive an immediate tax deduction for contributions but pay ordinary income tax on all withdrawals in retirement. With a Roth IRA, you contribute after-tax dollars—meaning no upfront deduction—but your money grows and is withdrawn completely tax-free.

This distinction creates meaningful long-term value. According to research from Vanguard’s How America Saves report , a $7,000 annual contribution growing at 7% annually would result in approximately $657,000 in a Roth IRA after 30 years, compared to the same $657,000 in a Traditional account that would be reduced by approximately $157,000 in taxes upon withdrawal (assuming 24% marginal tax rate). The Roth account owner keeps the full amount while the Traditional account owner nets roughly $500,000 after paying taxes.

The benefits extend beyond just investment returns. Because your qualified Roth withdrawals aren’t counted as taxable income, they won’t trigger higher Medicare premiums or increase taxes on your Social Security benefits. This becomes particularly valuable in retirement when you have multiple income sources and want to manage your tax bracket strategically.

Understanding the Five-Year Rule and Qualified Distributions

To receive tax-free withdrawals from a Roth IRA, you must satisfy both the five-year rule and meet one of several qualifying conditions. The five-year rule requires that you hold the Roth IRA for at least five years before taking a qualified distribution. This five-year period begins on the first day of the tax year for which you made your first contribution to any Roth IRA you own.

The confusion often arises because many financial advisors recommend establishing a Roth IRA as early as possible—even with a small amount—to start the five-year clock ticking. The IRS clarifies that once you’ve met the five-year requirement, all subsequent qualified withdrawals remain tax-free, regardless of your age.

A qualified distribution from a Roth IRA meets these requirements: the account has been open for at least five years, and the distribution occurs after you reach age 59½, become disabled, or use up to $10,000 for a first-time home purchase (lifetime limit). Importantly, you can always withdraw your contributions (but not earnings) from a Roth IRA at any time, tax-free and penalty-free, because you’ve already paid taxes on that money.

No Required Minimum Distributions: The Power of Tax Deferral

One of the most valuable yet underappreciated Roth IRA advantages is the absence of Required Minimum Distributions (RMDs). Traditional IRAs and 401(k)s force you to begin taking taxable withdrawals at age 73 (as of 2023, under SECURE 2.0 Act), whether you need the money or not. These withdrawals can push you into higher tax brackets and force you to liquidate investments at inopportune times.

Roth IRAs have no RMDs during your lifetime. This means you can let your money grow tax-free indefinitely, maximizing the power of compound growth. For investors who don’t need the money in retirement—or who want to pass wealth to heirs—this feature alone can add tens or hundreds of thousands of dollars to your eventual estate value.

The lack of RMDs also provides significant planning flexibility. In years when your other income is high, you can let your Roth grow. In years when you want to minimize taxable income (perhaps to qualify for certain tax credits or manage Medicare costs), you still aren’t forced to take distributions. This control represents a substantial advantage that many retirees overlook when choosing account types.

Roth IRA Income Limits and Contribution Rules for 2024 and 2025

Direct Roth IRA contributions are subject to income limits based on your Modified Adjusted Gross Income (MAGI) and filing status. For 2024, single filers with MAGI above $146,000 begin having their Roth contribution limit reduced, with complete phaseout at $161,000. Married couples filing jointly see phaseout begin at $230,000 and complete phaseout at $240,000 (IRS Publication 590-A, December 2023).

For 2025, these limits increase slightly due to inflation adjustments. Single filers can make a full Roth contribution with MAGI up to $150,000, with reduced contributions up to $165,000. Married filers can contribute fully up to $236,000, with phaseout complete at $246,000.

The annual contribution limit for 2024 remains $7,000 ($8,000 if you’re age 50 or older by year-end), with 2025 limits increasing to $7,000 ($8,000). These limits apply combined across all Traditional and Roth IRAs—you cannot contribute $7,000 to each account type.

If your income exceeds these limits, the Backdoor Roth IRA strategy remains available. This involves making a non-deductible contribution to a Traditional IRA and then converting that amount to a Roth IRA. While this requires careful tax planning and potentially paying taxes on any gains or deductible contributions, it provides high earners access to Roth benefits. The SECURE 2.0 Act eliminated the pro-rata rule complexity for conversions of after-tax contributions in 2024, making this strategy more accessible.

Case Study: Roth IRA vs. Traditional 401(k) Over 30 Years

Consider a practical example illustrating the Roth advantage. Sarah, age 35, can choose between contributing $7,000 annually to her employer’s 401(k) with a Traditional (pre-tax) structure or to a Roth IRA with after-tax dollars. Assuming she remains in the 22% marginal tax bracket now and in retirement, and her investments grow at 7% annually.

After 30 years of contributions, both accounts would reach approximately $657,000. However, when Sarah begins withdrawing at age 65, the Traditional 401(k) withdrawals are fully taxable. At her expected 22% tax rate, she nets approximately $513,000 after paying $144,000 in taxes. The Roth IRA, having already been taxed, provides the full $657,000 tax-free.

This $144,000 difference represents pure value from the Roth structure—an extra 28% of final account value simply from paying taxes upfront rather than upon withdrawal. If Sarah’s retirement tax rate is lower (say, 12%), the Traditional account would net more after lower taxes, but the Roth still provides valuable certainty and tax diversification.

The analysis demonstrates why many financial advisors recommend Roth accounts for younger workers who expect to be in higher tax brackets in retirement. The certainty of tax-free growth and withdrawals provides valuable planning peace of mind, regardless of future tax rate changes.

Estate Planning Benefits: Passing Tax-Free to Heirs

Roth IRAs offer exceptional benefits for passing wealth to heirs that other retirement accounts cannot match. When you name a beneficiary on your Roth IRA, they inherit the account tax-free—not tax-deferred. This means your beneficiary can take distributions tax-free regardless of their own income level, as long as the account meets the five-year holding requirement (or they stretch distributions over their life expectancy).

This contrasts sharply with Traditional IRAs, where beneficiaries must pay ordinary income tax on all withdrawals. A $500,000 Roth IRA passed to a child in the 32% tax bracket represents $500,000 of tax-free inheritance. The same $500,000 Traditional IRA, after paying approximately $160,000 in income taxes, delivers only $340,000 of actual value.

For estate planning purposes, Roth IRAs also allow you to control when distributions begin. Unlike 401(k)s where non-spouse beneficiaries must empty accounts within 10 years, Roth IRA beneficiaries can take distributions over their life expectancy, maintaining the tax-free growth vehicle for decades longer. This makes Roth IRAs particularly powerful for multigenerational wealth transfer.

Strategic Considerations: When to Choose Roth Over Traditional

Determining whether a Roth IRA makes sense depends on your specific tax situation, current and expected future tax brackets, and retirement timeline. Financial advisors generally recommend Roth contributions when you expect to be in a higher tax bracket in retirement than you are currently, when you want tax diversification in retirement, or when you want to maximize estate planning benefits for heirs.

The decision becomes more nuanced when you have access to a 401(k) with employer matching. Always contribute enough to your employer’s plan to capture the full employer match—that’s immediate guaranteed return before considering tax advantages. After securing the match, evaluating whether to continue 401(k) contributions or redirect to a Roth IRA depends on your specific situation.

For those self-employed with high incomes, a Self-Directed IRA or SEP-IRA may offer different planning opportunities. Some high earners also benefit from “mega backdoor Roth” strategies when their 401(k) plan allows after-tax contributions that can be converted to Roth—a strategy that requires plan provisions and careful execution but can accelerate retirement savings significantly.

Frequently Asked Questions

Can I contribute to both a Traditional IRA and a Roth IRA in the same year?

Yes, you can contribute to both account types, but the total combined contributions cannot exceed $7,000 ($8,000 if age 50+) for 2024. For example, you might contribute $4,000 to a Roth IRA and $3,000 to a Traditional IRA. However, you cannot deduct Traditional IRA contributions if you or your spouse are covered by a workplace retirement plan unless your income falls below certain thresholds .

What happens if I withdraw earnings from my Roth IRA before age 59½?

Earnings withdrawn before meeting the five-year rule and before age 59½ (or qualifying for an exception) will be taxed as ordinary income and may incur a 10% early withdrawal penalty. However, you can always withdraw your original contributions tax-free and penalty-free since you’ve already paid taxes on that money. The key distinction is that contributions come out tax-free; earnings do not.

Is a Roth IRA better than a Traditional IRA for everyone?

No, a Roth IRA isn’t automatically better for everyone. If you expect to be in a significantly lower tax bracket in retirement, a Traditional IRA’s upfront deduction may provide more value. Additionally, if you need the immediate tax deduction to afford contributions, Traditional may make more sense. Many financial advisors recommend having both types of accounts for tax flexibility in retirement.

Can I open a Roth IRA for my child or grandchild?

Yes, minors can have a Roth IRA as long as they have earned income from employment (wages, salary, or self-employment). Parents or grandparents can contribute to a minor’s Roth IRA up to the amount of the child’s earned income or the annual contribution limit, whichever is less. This makes Roth IRAs powerful tools for teaching compound interest and starting young people on retirement savings early.

Does income from a Roth IRA affect my Social Security benefits?

No, qualified Roth IRA withdrawals are not included in your adjusted gross income for purposes of determining Social Security benefit taxation. Unlike Traditional IRA and 401(k) withdrawals, which can cause up to 85% of your Social Security benefits to be taxed, Roth distributions remain tax-free and don’t impact your Social Security taxation level.

How do I know if my Roth IRA meets the five-year rule?

The five-year clock starts on January 1 of the tax year for which you make your first contribution to any Roth IRA. Once satisfied, this five-year period applies to all your Roth IRAs going forward—even if you open new accounts. You can confirm your account’s status by contacting your IRA custodian or checking your account statements, which should indicate when your first contribution was made.

Maximizing Your Roth IRA Benefits

The tax advantages of Roth IRAs make them one of the most powerful tools available for retirement savings and wealth building. By contributing after-tax dollars now, you secure tax-free growth and tax-free qualified withdrawals in retirement—potentially saving tens or hundreds of thousands of dollars in lifetime taxes compared to Traditional accounts.

IMMEDIATE ACTION STEPS:

| Timeframe | Action | Expected Outcome |

|---|---|---|

| This Week (30 min) | Calculate your MAGI and determine Roth IRA eligibility for 2024-2025 | Confirm contribution limits based on income |

| This Month (2 hrs) | Open a Roth IRA if eligible, or research Backdoor Roth strategy if income-limited | Establish account to start five-year clock |

| This Quarter | Max out annual contribution ($7,000 or $8,000 if 50+) | Maximize tax-free growth opportunity |

KEY INSIGHT: The most valuable feature of a Roth IRA may not be the tax-free withdrawals—it’s the lack of required minimum distributions. This allows your money to grow tax-free for your entire life, providing flexibility in retirement that no other retirement account offers. For those who don’t need retirement account funds for living expenses, this feature alone can add substantial value to your estate.

FINAL RECOMMENDATION: If you’re eligible for a Roth IRA and expect to be in a similar or higher tax bracket in retirement than you are now, prioritize maxing out your Roth contribution before taxable investments. The certainty of tax-free growth and withdrawals provides valuable financial planning flexibility that becomes increasingly valuable as tax uncertainty continues.

Note: This article provides general educational information about Roth IRAs and should not be considered personalized tax or investment advice. Consult a qualified financial advisor or tax professional for guidance specific to your situation.