12Views 0Comments

Is Crypto Taxable Income? The Complete Guide

Cryptocurrency has become a significant part of the financial landscape, with millions of Americans holding, trading, or mining digital assets. Yet the tax implications remain confusing for many investors. The Internal Revenue Service (IRS) has clarified its position over the years, but understanding what triggers a taxable event—and what doesn’t—requires careful attention to the rules. This guide breaks down everything you need to know about how the IRS treats cryptocurrency for tax purposes.

Understanding the IRS Position on Cryptocurrency

The IRS treats cryptocurrency as property, not as currency. This fundamental distinction, established in IRS Notice 2014-21, means that general tax principles applicable to property transactions apply to cryptocurrency transactions. When you sell, trade, or dispose of cryptocurrency, you may realize a capital gain or loss that must be reported on your tax return.

The IRS position has evolved significantly since 2014. In 2020, the agency added a specific question to Form 1040 asking taxpayers whether they received, sold, exchanged, or otherwise disposed of any financial interest in virtual currency. This yes-or-no question applies to all taxpayers and signals the IRS’s increased focus on cryptocurrency compliance.

For tax purposes, cryptocurrency falls into two categories: capital assets and ordinary income property. How you acquire or use your cryptocurrency determines which category applies and how it will be taxed.

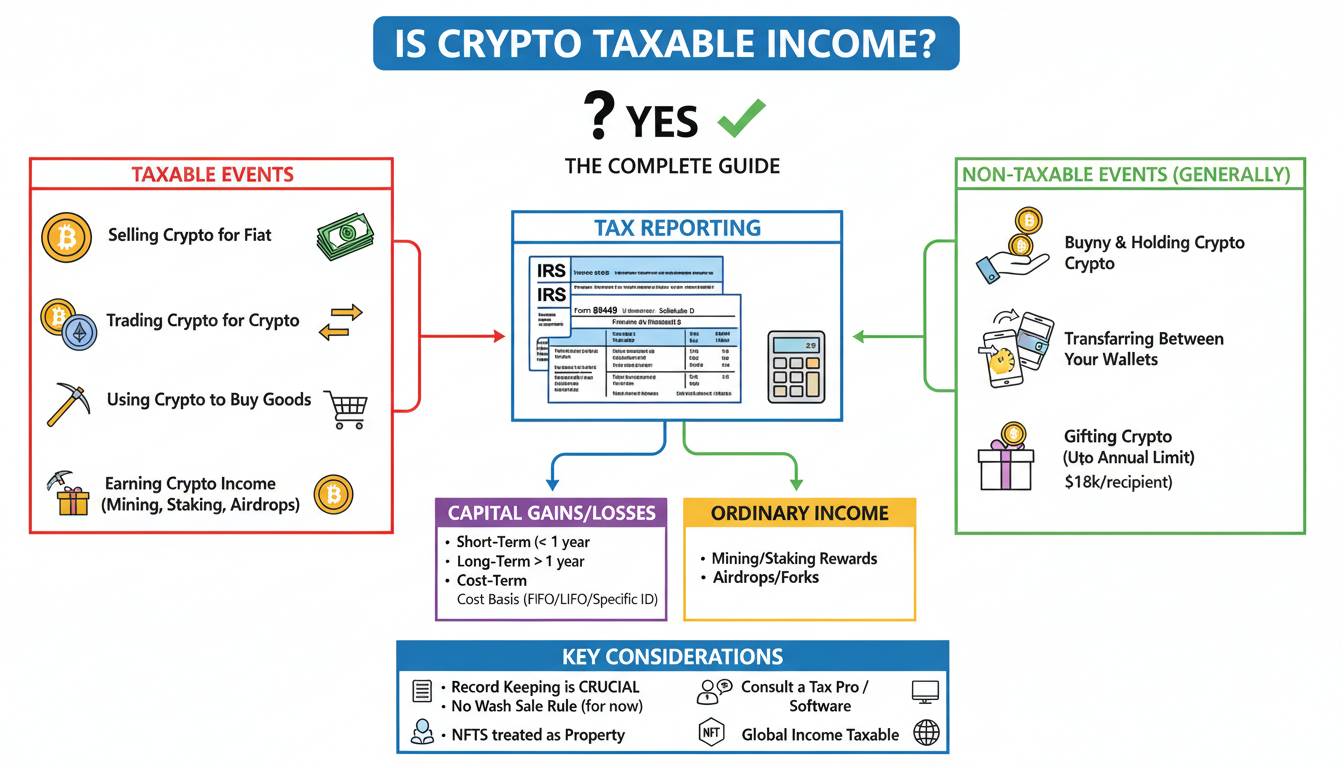

What Triggers a Taxable Event

A taxable event occurs when you dispose of cryptocurrency in a way that triggers a capital gain or when you receive cryptocurrency as ordinary income. Understanding these triggers helps you plan your transactions and maintain accurate records.

Selling cryptocurrency for fiat currency (dollars, euros, etc.) is a taxable event. If you bought Bitcoin for $30,000 and sold it for $50,000, you have a $20,000 capital gain that must be reported. Conversely, if you sold at a loss, you have a capital loss that can offset other gains or up to $3,000 of ordinary income annually.

Trading one cryptocurrency for another is also taxable. The IRS views this as two separate transactions: selling the first cryptocurrency and buying the second. For example, trading Ethereum for Solana triggers a taxable event on the Ethereum position, even though you never touched fiat currency.

Using cryptocurrency to purchase goods or services constitutes a taxable event. If you bought a car with Bitcoin that had appreciated in value, you must report the capital gain on that transaction. The gain is calculated as the difference between your cost basis in the Bitcoin and its fair market value at the time of the purchase.

Mining and Staking Income

If you mine cryptocurrency or participate in staking pools, the rewards you receive are treated as ordinary income. The fair market value of the cryptocurrency on the day you receive it becomes your cost basis. This means the entire reward amount is taxable as income, regardless of whether you sell it immediately or hold it.

When you later sell the mined or staked cryptocurrency, you’ll also potentially realize a capital gain or loss based on the difference between your cost basis (the income value you originally reported) and the sale price. This creates a two-tier tax situation: ordinary income at receipt, then potential capital gains treatment on any appreciation above that basis.

The IRS has indicated in FAQs that cryptocurrency received from mining is gross income to the recipient. If you mine cryptocurrency as a business, you’ll report these rewards on Schedule C as self-employment income, which subjects you to both income tax and self-employment tax.

Airdrops, Forks, and Gifts

Airdrops present a unique tax situation. When you receive free cryptocurrency through an airdrop, the IRS generally considers this ordinary income equal to the fair market value of the tokens at the time of receipt. This income must be reported on your tax return.

However, the tax treatment can vary depending on circumstances. If you receive airdropped tokens as compensation for services or as payment for something, it’s clearly ordinary income. Some tax practitioners argue that purely voluntary airdrops (where no action is required beyond holding an existing cryptocurrency) might be treated differently, but the IRS has not issued specific guidance clarifying this distinction.

Cryptocurrency hard forks can also create taxable events. When a blockchain splits and you receive new tokens, the IRS typically views this as taxable income equal to the fair market value of the new tokens at the time you gain control over them. The original cryptocurrency’s cost basis typically carries over to the new tokens, meaning you’re taxed on the full value received without any corresponding increase in cost basis.

Gifting cryptocurrency has different implications depending on the amount and recipient. You can gift up to $18,000 per recipient in 2024 without triggering gift tax reporting (this amount adjusts annually for inflation). If you gift more than that, you must file a gift tax return, but the gift tax itself may be covered by your lifetime exemption. The recipient generally receives your cost basis in the cryptocurrency (carryover basis), not a stepped-up basis like gifts of appreciated stock.

Capital Gains vs. Ordinary Income

The distinction between capital gains and ordinary income significantly affects your tax rate. Capital gains are divided into short-term and long-term categories. Short-term capital gains apply to assets held for one year or less and are taxed at your ordinary income tax rate, which can be as high as 37% for federal taxes. Long-term capital gains apply to assets held more than one year and receive preferential tax rates of 0%, 15%, or 20% depending on your income level.

Most cryptocurrency transactions result in capital gains or losses. This includes selling cryptocurrency, trading one crypto for another, and using crypto to make purchases. The holding period matters enormously for tax planning. If you hold for more than a year before selling, you could cut your tax rate substantially.

Ordinary income treatment applies in specific situations: mining rewards, staking rewards, airdrops (in most cases), cryptocurrency earned as wages or payment for services, and interest earned on crypto lending platforms. This income is taxed at your marginal income tax rate and is subject to ordinary income tax rules.

Reporting Requirements and Forms

Reporting cryptocurrency transactions requires several forms depending on your situation. For most individual taxpayers, Form 8949 (Sales and Other Dispositions of Capital Assets) is used to report capital gains and losses. This form feeds into Schedule D on your tax return, where you summarize your overall capital gains and losses for the year.

If you receive cryptocurrency as ordinary income from mining or staking, this goes directly on your Form 1040 as part of your total income. If you operate a cryptocurrency mining business, you’ll use Schedule C to report business income and expenses.

The IRS has increased its focus on cryptocurrency compliance. Cryptocurrency exchanges are required to report certain transactions to the IRS using Form 1099-DA (Digital Asset Transactions), starting in tax year 2026 for most brokers. This parallels the 1099-K reporting that payment platforms like PayPal and Venmo use. Even before this requirement, many exchanges were issuing 1099 forms to customers with reportable transactions.

Failing to report cryptocurrency income can result in penalties, interest, and in egregious cases, criminal prosecution. The IRS has stated that cryptocurrency non-compliance is an area of focus for its examination division.

Frequently Asked Questions

Do I have to pay taxes on cryptocurrency if I just hold it?

No. Simply holding cryptocurrency in your wallet does not trigger a taxable event. You only owe taxes when you sell, trade, or dispose of the cryptocurrency in a way that realizes gains or creates income. The act of purchasing cryptocurrency and holding it indefinitely is not taxable.

What happens if I sell cryptocurrency at a loss?

You can claim capital losses from cryptocurrency sales to offset capital gains from other investments. If your losses exceed your gains, you can offset up to $3,000 of ordinary income per year, with any remaining losses carried forward to future tax years. This makes tax-loss harvesting a legitimate strategy for managing your overall tax liability.

Do I need to report my cryptocurrency on my tax return if I didn’t sell anything?

You should still answer “yes” to the virtual currency question on Form 1040 if you held cryptocurrency at any point during the year, even if you didn’t sell it. The question asks whether you had any financial interest in virtual currency, which includes simply holding it. Answering honestly ensures you remain in compliance with IRS requirements.

Can the IRS track my cryptocurrency transactions?

Yes. The IRS has significant visibility into cryptocurrency transactions. Exchanges report customer transactions to the IRS, and the agency has been actively working to identify taxpayers who fail to report cryptocurrency income. Using blockchain analysis tools, the IRS can often trace transactions even when taxpayers attempt to remain anonymous.

What records should I keep for cryptocurrency taxes?

Maintain records of every transaction including the date, amount, fair market value in dollars at the time, the purpose of the transaction, and the counterparty (when available). Keep records of your original purchase price (cost basis) for all cryptocurrency acquired. These records are essential for calculating gains and losses accurately and defending your tax position if examined.

Understanding cryptocurrency taxation requires attention to detail and consistent record-keeping. While the rules continue to evolve, the fundamental principle remains: disposing of cryptocurrency in a way that creates profit typically triggers a taxable event. Consult with a qualified tax professional who understands cryptocurrency if you have significant transactions or complex situations. The cost of professional guidance is typically far less than the potential penalties for non-compliance.