2Views 0Comments

Compound Interest vs Simple Interest: What’s the Difference?

Understanding the difference between compound interest and simple interest is one of the most important financial literacy skills you can develop. These two methods of calculating interest affect everything from your savings accounts to your mortgage payments, yet many people don’t fully grasp how each one works—or how dramatically they can differ over time.

This guide breaks down both concepts with clear examples, formulas, and real-world applications so you can make smarter decisions about your money.

What Is Simple Interest?

Simple interest is calculated only on the original principal amount—the money you initially deposit or borrow. The interest earned or paid does not itself earn interest over time. This makes simple interest the most straightforward method of calculating interest.

The simple interest formula is:

Simple Interest = Principal × Rate × Time

For example, if you deposit $10,000 in an account that pays 5% simple interest annually, you would earn $500 in interest each year, regardless of how much your balance grows. After three years, you would have earned $1,500 in total interest, bringing your balance to $11,500.

Simple interest is commonly used for:

- Short-term loans

- Auto loans

- Some mortgages

- Treasury bills and bonds

- Promissory notes

The key characteristic of simple interest is that the interest amount remains constant throughout the entire term. You never earn interest on interest, which makes predictions straightforward but often means less growth for savers.

What Is Compound Interest?

Compound interest is calculated on the principal plus all previously earned interest. This creates a snowball effect where your money grows exponentially over time—the interest itself starts earning interest. This is often called “interest on interest.”

The compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

– A = the future value of the investment

– P = the principal (initial deposit)

– r = annual interest rate (decimal)

– n = number of times interest compounds per year

– t = time in years

Using the same example—$10,000 at 5% interest compounded annually for three years:

- Year 1: $10,000 × 1.05 = $10,500

- Year 2: $10,500 × 1.05 = $11,025

- Year 3: $11,025 × 1.05 = $11,576.25

With compound interest, you would have $11,576.25 after three years—$76.25 more than with simple interest. That difference seems small now, but it grows dramatically over longer periods.

Most savings accounts, certificates of deposit (CDs), and investment accounts use compound interest. It’s also how credit card balances and most loans accumulate interest.

Side-by-Side Comparison

| Feature | Simple Interest | Compound Interest |

|---|---|---|

| Calculation Base | Principal only | Principal + accumulated interest |

| Interest Earned | Fixed each period | Increases over time |

| Growth Pattern | Linear | Exponential |

| Typical Use Cases | Short-term loans, some bonds | Savings accounts, investments, mortgages |

| Long-term Effect | Predictable but slower | Accelerated growth |

| Formula Complexity | Simple multiplication | Exponents required |

The Power of Compounding Over Time

The true difference between these two methods becomes striking over extended periods. Let’s compare what happens when you invest $10,000 at a 7% annual interest rate over 30 years:

Simple Interest Calculation:

– Annual interest: $10,000 × 0.07 = $700

– Total over 30 years: $700 × 30 = $21,000

– Final balance: $31,000

Compound Interest Calculation:

– Using the formula: $10,000 × (1.07)^30 = $76,122.55

– Total interest earned: $66,122.55

– Final balance: $76,122.55

The compound interest balance is more than 2.4 times larger than the simple interest balance. This $45,122.55 difference illustrates why Albert Einstein reportedly called compound interest the “eighth wonder of the world.”

The longer your money has to compound, the more dramatic the results. This is why financial advisors emphasize starting to save and invest as early as possible.

How Compounding Frequency Affects Returns

Compound interest doesn’t compound only once per year. The frequency of compounding significantly impacts your final balance. Common compounding periods include:

- Annually: Once per year (n=1)

- Semi-annually: Twice per year (n=2)

- Quarterly: Four times per year (n=4)

- Monthly: Twelve times per year (n=12)

- Daily: 365 times per year (n=365)

Using our $10,000 at 5% for one year example:

| Compounding Frequency | Final Balance | Total Interest |

|---|---|---|

| Annually | $10,500.00 | $500.00 |

| Semi-annually | $10,506.25 | $506.25 |

| Quarterly | $10,509.45 | $509.45 |

| Monthly | $10,511.62 | $511.62 |

| Daily | $10,512.67 | $512.67 |

More frequent compounding yields slightly higher returns. However, the difference becomes more meaningful with larger principal amounts and longer time horizons.

Simple Interest in Everyday Finance

While compound interest dominates most savings and investment products, simple interest still appears in several common financial situations.

Auto loans typically use simple interest, calculated on the outstanding principal each month. Your monthly payment stays the same, but the portion going toward interest decreases over time while the portion going toward principal increases.

Treasury bills (T-bills) and some corporate bonds pay simple interest. You receive fixed interest payments periodically, then get your principal back at maturity.

Some mortgages calculate interest using a simple interest method, though most use amortization that effectively creates compound interest. It’s worth checking your loan documents to understand how your mortgage interest is calculated.

When borrowing money with simple interest, you’ll typically pay less interest over the life of the loan compared to compound interest. However, the distinction matters less for short-term loans where the difference is minimal.

Compound Interest in Everyday Finance

Compound interest works against you when you’re borrowing money but works for you when you’re saving or investing.

Savings accounts at banks and credit unions compound interest, typically daily or monthly. Your deposits earn interest, and that interest earns additional interest.

Investment accounts, including 401(k)s, IRAs, and brokerage accounts, benefit from compound growth. Reinvested dividends and capital gains create exponential growth over decades.

Credit cards are perhaps the most notorious example of compound interest working against consumers. When you carry a balance, interest accrues on your balance, then that interest itself accrues additional interest—quickly growing debt if left unpaid.

Student loans and mortgages typically use amortization schedules where interest compounds, though the monthly payment remains fixed. In the early years, most of your payment goes toward interest rather than reducing the principal.

Understanding how compound interest affects your debts helps you prioritize paying off high-interest balances faster.

Which Type Should You Seek?

For building wealth, you want compound interest working in your favor. Look for:

- High-yield savings accounts with daily compounding

- Certificates of deposit (CDs) with competitive rates

- Index funds and ETFs that compound through reinvested earnings

- Retirement accounts with decades to grow

For borrowing, simple interest generally costs you less than compound interest. When shopping for loans, look for:

- Simple interest auto loans (which most already are)

- Loans with no origination fees

- Payday loan alternatives (which often have extreme compound interest)

The key principle: earn compound interest on your assets, avoid compound interest on your debts whenever possible.

The Rule of 72

A quick mental math shortcut helps estimate how long it takes for compound interest to double your money: divide 72 by your interest rate.

At 6% annual interest: 72 ÷ 6 = 12 years to double

At 8% annual interest: 72 ÷ 8 = 9 years to double

At 4% annual interest: 72 ÷ 4 = 18 years to double

This rule provides a useful approximation for understanding the power of different interest rates over time. It’s particularly striking when you consider that doubling your money twice (quadrupling) at 8% takes only 18 years.

Frequently Asked Questions

Q: Is compound interest always better than simple interest?

A: It depends on whether you’re earning or paying interest. For savings and investments, compound interest is better because it accelerates your returns. For borrowing, simple interest is typically better because it results in less total interest paid over the loan term.

Q: How do I calculate compound interest manually?

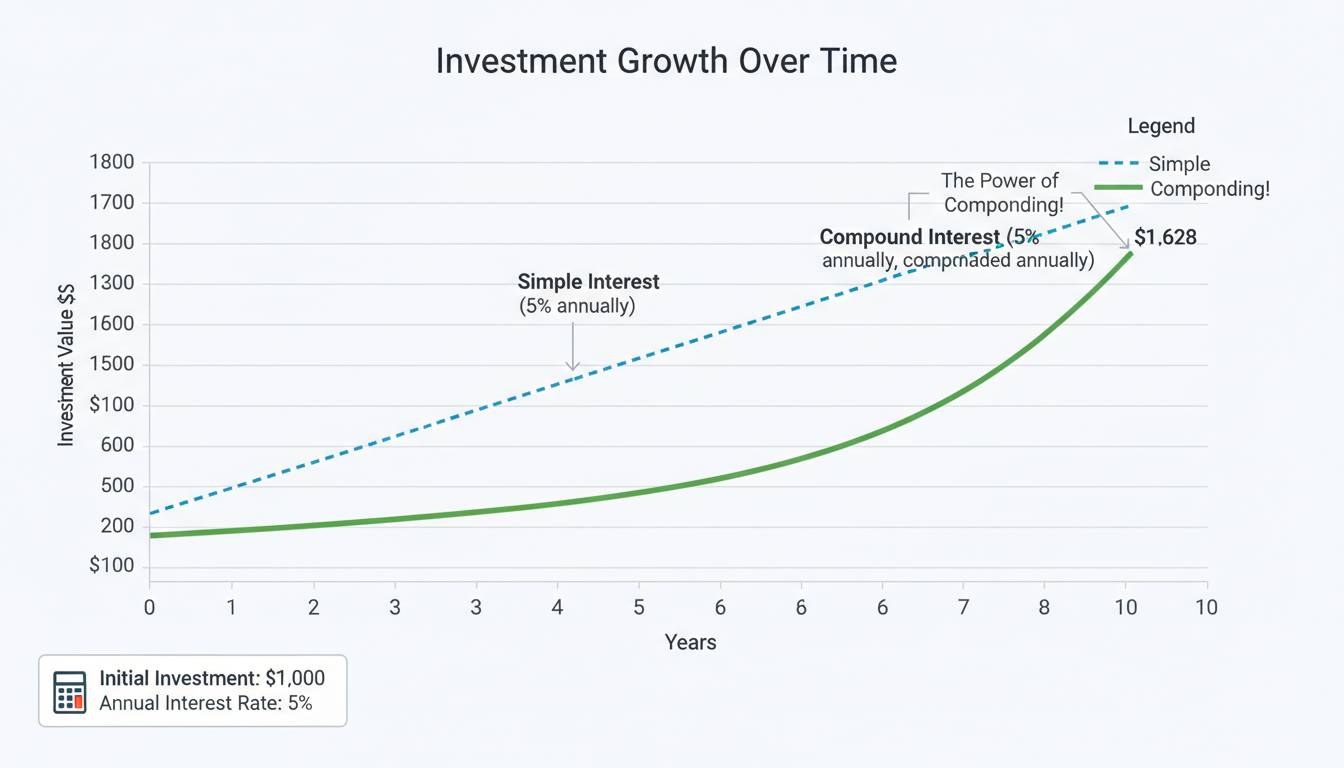

A: Use the formula A = P(1 + r/n)^(nt). For annual compounding at 5% on $1,000 for 10 years: $1,000 × (1 + 0.05)^10 = $1,628.89. Many online calculators can handle more complex scenarios with different compounding frequencies.

Q: What’s the main difference between simple and compound interest?

A: Simple interest is calculated only on the original principal amount. Compound interest is calculated on the principal plus all accumulated interest. This fundamental difference causes compound interest to grow much faster over time.

Q: Do banks use simple interest or compound interest?

A: Most deposit accounts (savings accounts, checking accounts, CDs) use compound interest. Most loans (mortgages, auto loans, personal loans) also effectively use compound interest through amortization. Pure simple interest loans are less common but exist, particularly for some auto loans and short-term financing.

Q: How does compound interest help with retirement savings?

A: When you invest in retirement accounts like 401(k)s or IRAs, your returns are reinvested and compound over decades. A $10,000 investment at 7% average annual return grows to over $76,000 in 30 years—all from compound growth on your contributions and their earnings.

Q: Can simple interest ever beat compound interest?

A: Over the same time period with the same rate, simple interest will always result in less total money than compound interest for savers and less total owed for borrowers. The only scenario where simple interest might seem “better” is if you withdraw interest earnings frequently and never reinvest them—but that’s a behavior choice, not an inherent advantage of the interest type.

Conclusion

The distinction between simple interest and compound interest is foundational to financial literacy. Simple interest offers predictable, linear growth or costs—you know exactly what you’ll earn or pay. Compound interest delivers exponential growth by earning interest on your interest, making it the superior choice for long-term wealth building.

The key takeaway: maximize compound interest working for you through savings and investments, while minimizing compound interest working against you through debt. Time is your greatest ally when compounding is on your side—the earlier you start, the more dramatically your money can grow.

Use the formulas and examples in this guide to calculate potential returns on any savings or investment opportunity, and always verify whether loans use simple or compound interest before signing. This single understanding can translate into thousands—or even hundreds of thousands—of dollars over your lifetime.