15Views 0Comments

Dollar Cost Averaging Explained: Beginner’s Complete Guide

Dollar cost averaging is an investment strategy that involves investing a fixed amount of money at regular intervals, regardless of market conditions, rather than trying to time the market by making lump sum investments. This approach removes emotional decision-making from investing and can significantly reduce the risk of buying assets at unfavorable prices. By spreading purchases over time, investors automatically buy more shares when prices are low and fewer shares when prices are high, potentially lowering their average cost per share over the long term.

For beginner investors, dollar cost averaging offers a structured, low-stress way to build wealth through consistent contributions to retirement accounts like 401(k)s or individual brokerage accounts. The strategy has gained widespread adoption because it aligns with how most people earn income—through regular paychecks—making it one of the most accessible investment approaches available.

What Is Dollar Cost Averaging?

Dollar cost averaging is an investment technique where you divide the total amount you want to invest into equal portions and invest those portions at regular intervals, typically monthly or biweekly. Rather than investing $12,000 all at once, for example, you would invest $1,000 per month over one year. This systematic approach ensures that you purchase shares at various price points throughout the investment period, smoothing out the effects of market volatility.

The fundamental principle behind dollar cost averaging rests on a simple mathematical reality: markets fluctuate. No one can consistently predict whether prices will rise or fall in the short term. By committing to regular investments regardless of market conditions, you avoid the dangerous trap of trying to time the market—a strategy that even professional investors struggle to execute successfully.

Key Components of Dollar Cost Averaging:

- Fixed Investment Amount: You invest the same dollar amount each time, whether markets are soaring or plummeting

- Regular Intervals: Purchases occur on a consistent schedule you establish in advance

- Automatic Contributions: Most investors set up automatic transfers to remove decision fatigue

- Long-Term Focus: The strategy works best over extended periods, typically five years or more

Research from Morningstar has consistently shown that attempting to time the market rarely produces superior results. A landmark study by Dalbar Associates found that the average investor underperformed the S&P 500 by a significant margin over 20-year periods, largely due to emotional reactions to market fluctuations. Dollar cost averaging provides a systematic solution to this pervasive problem.

How Dollar Cost Averaging Works in Practice

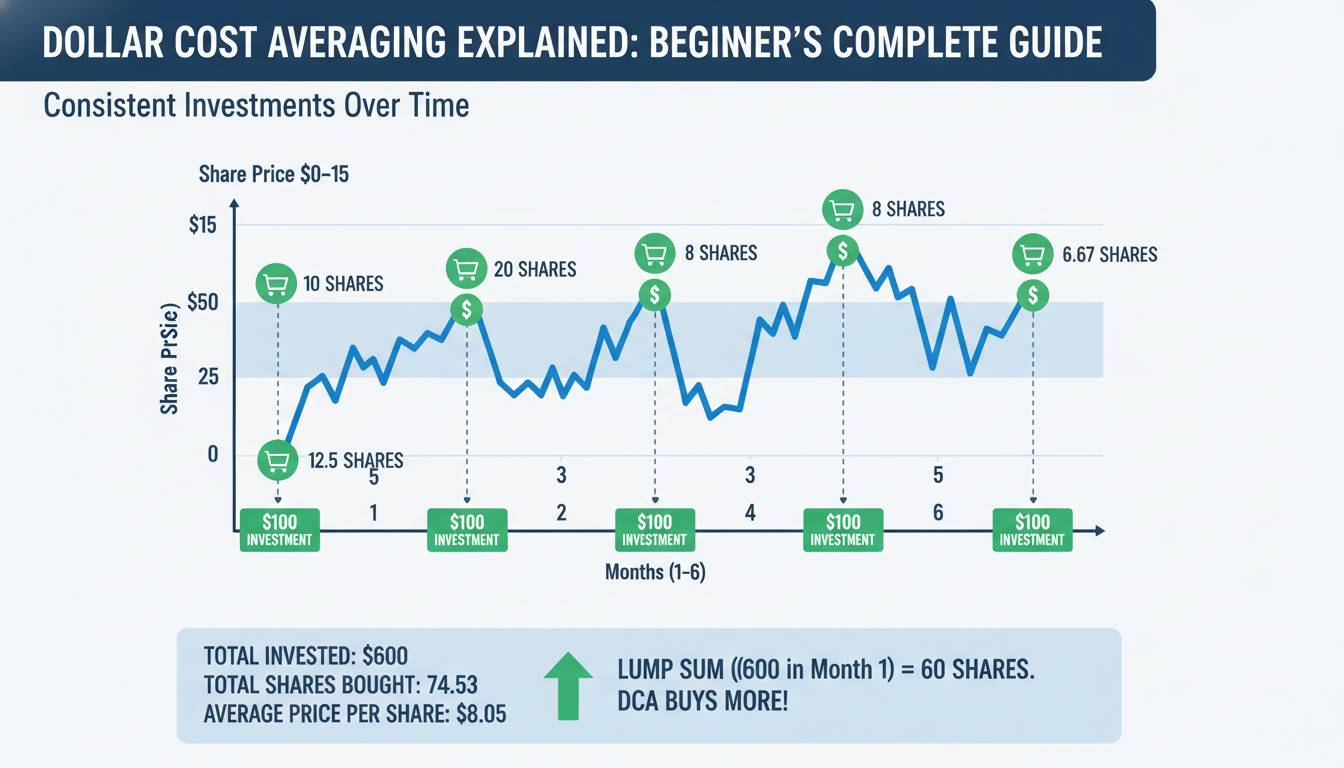

Understanding dollar cost averaging requires seeing it in action. Consider a practical example: imagine you want to invest $12,000 in an index fund that tracks the S&P 500. Instead of investing the entire amount immediately, you commit to investing $1,000 monthly for one year.

Sample DCA Implementation Over 12 Months:

| Month | Investment | Share Price | Shares Purchased |

|---|---|---|---|

| 1 | $1,000 | $100.00 | 10.00 |

| 2 | $1,000 | $90.00 | 11.11 |

| 3 | $1,000 | $80.00 | 12.50 |

| 4 | $1,000 | $70.00 | 14.29 |

| 5 | $1,000 | $75.00 | 13.33 |

| 6 | $1,000 | $85.00 | 11.76 |

| 7 | $1,000 | $95.00 | 10.53 |

| 8 | $1,000 | $105.00 | 9.52 |

| 9 | $1,000 | $110.00 | 9.09 |

| 10 | $1,000 | $100.00 | 10.00 |

| 11 | $1,000 | $95.00 | 10.53 |

| 12 | $1,000 | $105.00 | 9.52 |

In this scenario, despite significant price volatility ranging from $70 to $110, your average cost per share comes to approximately $92.50—well below the highest prices paid during the year. You accumulated 132.18 total shares with your $12,000 investment, compared to only 109.09 shares if you had invested the lump sum at the $110 price point.

This example illustrates the core advantage: when prices drop, your fixed contribution buys more shares, and when prices rise, you buy fewer—but the mathematical average works in your favor over time.

Key Benefits of Dollar Cost Averaging

The advantages of dollar cost averaging extend beyond simple mathematical optimization. This strategy offers multiple benefits that make it particularly suitable for beginning investors and those building long-term wealth.

1. Removes Emotional Decision-Making

Market volatility triggers powerful emotions—fear during downturns and greed during rallies. These emotions often lead investors to make poor decisions: selling at the bottom after markets have already declined or buying at peaks after significant gains. Dollar cost averaging creates a predetermined schedule that executes regardless of these emotional fluctuations. You simply follow your plan, and the math works itself out over time.

2. Makes Investing Affordable

Not everyone has tens of thousands of dollars readily available to invest as a lump sum. Dollar cost averaging allows you to start building wealth with much smaller amounts—perhaps $50 or $100 per month. This accessibility enables investors to begin benefiting from market growth much earlier than they would if they were saving for a large initial investment.

3. Reduces Timing Risk

The biggest risk in lump sum investing is deploying all your capital right before a market decline. Even historically successful periods have included dramatic short-term corrections. Dollar cost averaging naturally spreads this timing risk across many months or years, significantly reducing the probability of investing your entire nest egg at the worst possible moment.

4. Automates Wealth Building

Once you establish your contribution schedule, dollar cost averaging requires minimal ongoing attention. This hands-off approach fits seamlessly with busy lifestyles and prevents the temptation to tinker with your portfolio based on daily market movements or financial news headlines.

5. Supports Consistent Habit Formation

Psychologically, regular automated investments transform wealth building from an occasional event into a sustainable habit. Research on behavioral finance consistently shows that automatically saving a portion of income produces far better long-term outcomes than relying on willpower to save whatever remains at month’s end.

Dollar Cost Averaging vs. Lump Sum Investing

Understanding when dollar cost averaging makes sense requires comparing it to the alternative: lump sum investing. Each approach has distinct characteristics that make it more suitable for different situations.

Lump Sum Investing Advantages:

- Invests all capital immediately, potentially capturing more market growth

- Requires less ongoing management once executed

- Historically has outperformed dollar cost averaging in rising markets

- Simpler to execute with fewer transactions

Dollar Cost Averaging Advantages:

- Reduces timing risk and emotional decision-making

- More accessible for investors without large capital reserves

- Creates structured, automatic investing habits

- Performs better in volatile or declining markets

When to Choose Each Strategy:

The decision often depends on your specific circumstances. If you receive a large windfall—inheritance, sale of property, or workplace bonus—lump sum investing historically captures more upside over extended periods. Research from Vanguard found that lump sum investing outperformed dollar cost averaging approximately two-thirds of the time across historical periods analyzed.

However, dollar cost averaging makes more sense when you lack sufficient capital for a lump sum investment, when you’re building wealth gradually through regular income, or when market valuations appear particularly elevated. Many financial advisors recommend a hybrid approach: invest a portion of available capital immediately while maintaining a systematic contribution schedule for additional funds.

Best Strategies for Implementing Dollar Cost Averaging

Successfully implementing dollar cost averaging requires more than simply committing to regular purchases. The most effective approaches incorporate several strategic considerations that maximize the strategy’s benefits.

Choose the Right Investment Vehicles

Dollar cost averaging works best with low-cost, diversified investments that you intend to hold for years. Index funds and exchange-traded funds (ETFs) tracking broad market indexes represent ideal choices because they provide instant diversification and minimal fees. Individual stocks require more research and carry company-specific risks that can undermine the strategy’s risk-reduction benefits.

Align Contributions with Your Pay Schedule

The most sustainable dollar cost averaging schedules match your income flow. If you receive a biweekly paycheck, consider biweekly investments. If you’re paid monthly, monthly contributions work better. This alignment creates a seamless, virtually painless wealth-building process that feels natural rather than burdensome.

Start Immediately, Even Modestly

The most critical element of dollar cost averaging is starting. Many potential investors delay while waiting for the “perfect” time to begin—a strategy that virtually never produces optimal results. Starting with even $50 or $100 per month provides valuable experience with market fluctuations while beginning your wealth-building journey.

Consider Tax-Advantaged Accounts First

Maximizing tax-advantaged retirement accounts like 401(k)s and IRAs should typically precede taxable brokerage accounts. The tax benefits compound significantly over time, making these accounts particularly powerful vehicles for dollar cost averaging strategies.

Common Mistakes to Avoid with Dollar Cost Averaging

While dollar cost averaging is conceptually simple, several common errors can undermine its effectiveness. Being aware of these pitfalls helps ensure you implement the strategy correctly.

Stopping During Market Declines

The most damaging mistake is halting contributions when markets drop. This behavior contradicts the entire logic of dollar cost averaging—buying more shares at lower prices. During the 2008 financial crisis and the 2020 COVID-19 crash, investors who stopped contributing missed incredible opportunities to accumulate shares at deeply discounted prices. Historically, markets have recovered from every major crash, and those who continued investing benefited most from the subsequent rebounds.

Not Increasing Contributions Over Time

As your career progresses and income increases, maintaining the same contribution percentage builds wealth more slowly than gradually increasing your investment amount. Automating annual contribution increases—even small ones like 1-2% of income—produces dramatically larger portfolios over decades due to compound growth.

Choosing High-Fee Investments

Transaction costs and management fees eat into returns significantly over the long holding periods required for dollar cost averaging. Opting for low-cost index funds with expense ratios below 0.20% preserves more of your investment returns for compounding.

Having Too Short a Time Horizon

Dollar cost averaging truly demonstrates its value over extended periods—ideally ten years or more. Using the strategy for just one or two years provides less opportunity to smooth out market volatility and may actually underperform lump sum approaches during consistently rising markets.

Frequently Asked Questions

Does dollar cost averaging guarantee profits?

No investment strategy guarantees profits. Dollar cost averaging reduces risk by spreading purchases over time, but you can still lose money if markets decline persistently over your entire investment period. However, historically, markets have trended upward over extended periods, and dollar cost averaging has consistently produced positive returns for investors who maintained their contributions through market cycles.

How much should I invest with dollar cost averaging?

The appropriate amount depends on your financial situation, goals, and income. A common guideline is to invest 10-15% of your gross income for retirement, though this varies based on age, existing savings, and other factors. Starting with whatever amount feels sustainable—even $50 monthly—builds the habit and provides experience with market fluctuations.

Is dollar cost averaging better than timing the market?

Research consistently shows that timing the market—attempting to buy at lows and sell at highs—rarely produces superior results compared to consistent strategies like dollar cost averaging. Even professional investors with extensive resources struggle to time markets successfully. Dollar cost averaging provides a systematic, emotion-free approach that has proven effective for millions of long-term investors.

Can I use dollar cost averaging with any investment?

Dollar cost averaging works with any investment that allows fractional share purchases or regular contributions. Stocks, bonds, mutual funds, and ETFs all accommodate this strategy. The key is choosing investments you believe will grow over time and can commit to holding for years without reacting to short-term fluctuations.

What happens if I start dollar cost averaging and markets drop significantly?

This scenario represents exactly when dollar cost averaging works most powerfully. When markets decline, your fixed contributions purchase more shares at lower prices. Once markets recover—as they historically have following every major decline—those additional shares purchased at discount prices significantly boost your overall returns.

How long should I continue dollar cost averaging?

Dollar cost averaging is typically a long-term strategy. Continuing contributions throughout your working life, particularly into tax-advantaged retirement accounts, allows you to build substantial wealth through consistent contributions and compound growth. Many financial advisors recommend maintaining the strategy even in retirement by converting accumulated assets to income-generating investments.

Conclusion

Dollar cost averaging represents one of the most accessible, psychologically manageable approaches to building long-term wealth. By committing to regular, fixed investments regardless of market conditions, you eliminate the impossible task of timing market movements while developing a sustainable wealth-building habit. The strategy transforms investing from a stressful activity requiring constant attention into a simple, automated process that works steadily toward your financial goals.

The mathematical beauty of dollar cost averaging lies in its counterintuitive nature: buying more shares when prices fall and fewer when prices rise naturally creates a lower average cost per share over time. This mechanism has helped millions of investors build retirement portfolios and achieve financial independence without requiring sophisticated market knowledge or large initial capital.

Starting your dollar cost averaging journey today—regardless of how small your initial contributions might be—represents the most important step toward long-term financial security. The markets will inevitably fluctuate, but your commitment to consistent, disciplined investing will compound into substantial wealth over decades.