19Views 0Comments

Dollar Cost Averaging vs Lump Sum Investing: Which Wins?

Introduction

If you have $50,000 to invest, the question isn’t whether you should invest—it’s how. The debate between dollar cost averaging (DCA) and lump sum investing has divided financial professionals for decades, with passionate arguments on both sides. The answer isn’t simple, because the right strategy depends entirely on your financial situation, risk tolerance, and market conditions.

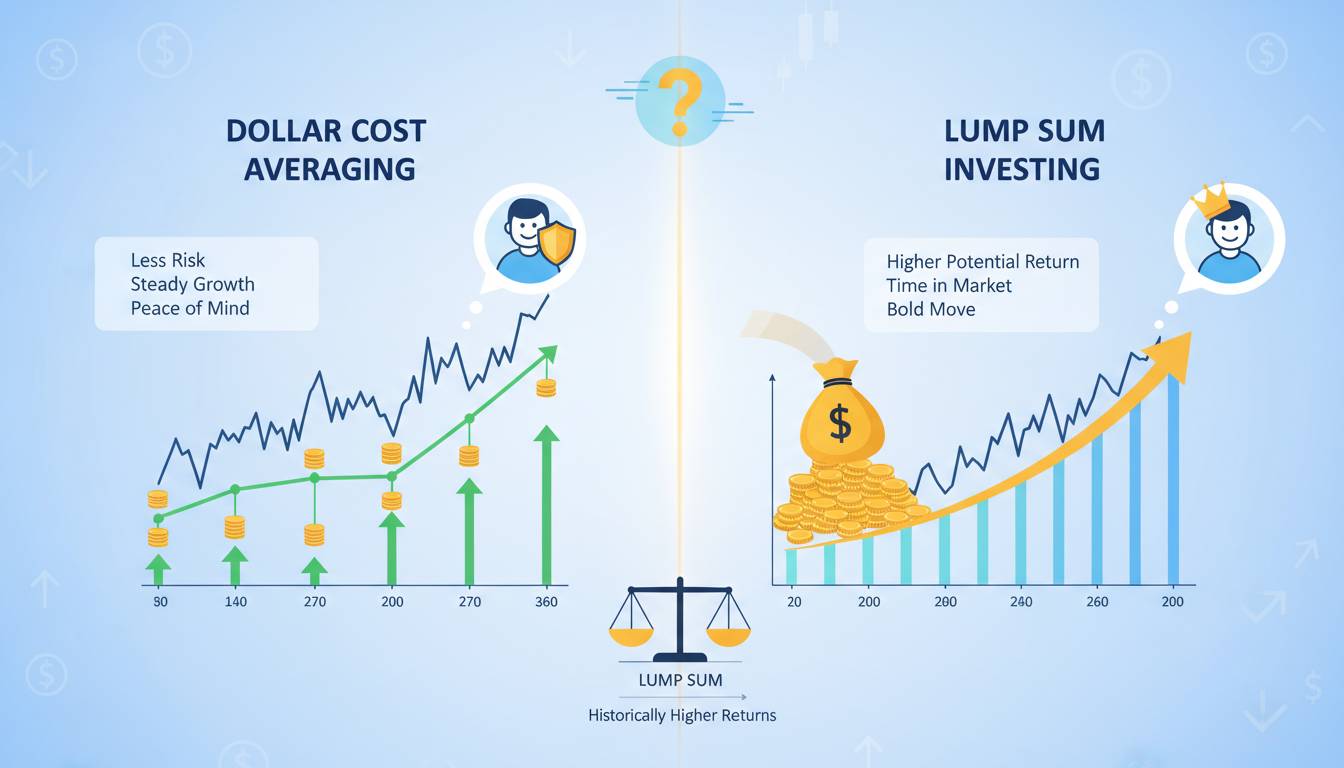

Dollar cost averaging involves spreading your investment across multiple purchases over time, buying shares at various price points. Lump sum investing means deploying all your capital immediately, catching whatever price exists on day one. Both approaches have mathematically proven advantages depending on market behavior, and understanding the nuances can mean the difference between optimal returns and costly mistakes.

This guide breaks down the mechanics, data, and strategic considerations you need to make an informed decision. You’ll learn what academic research reveals, when each approach makes sense, and how to choose based on your specific circumstances.

What Is Dollar Cost Averaging?

Dollar cost averaging is an investment strategy where you divide a total amount of money into equal installments invested at regular intervals, regardless of market conditions. Rather than investing $10,000 all at once, for example, you might invest $1,000 monthly for ten months.

The fundamental appeal lies in removing emotional decision-making from the equation. When you commit to investing a fixed amount on a schedule, you automatically buy more shares when prices are low and fewer shares when prices are high. This systematic approach creates a natural “buy low” mechanism without requiring you to predict market movements.

How DCA works in practice:

Imagine you have $12,000 to invest in an index fund. With DCA, you invest $1,000 each month for twelve months. In month one, the fund trades at $100 per share—you buy 10 shares. If prices drop to $80 in month two, your $1,000 now purchases 12.5 shares. When prices rise to $125 in month three, you acquire only 8 shares.

Over the full period, your average cost per share smooths out volatility, typically landing below the arithmetic average of the share prices. This mathematical elegance explains why DCA has persisted as a recommended strategy for decades, particularly among risk-averse investors and those investing through employer retirement plans.

The psychological benefits are equally significant. Investors using DCA report less anxiety during market downturns because they’re “getting a deal” on new shares rather than watching a lump sum investment lose value. This emotional buffering often prevents panic selling—a destructive behavior that can devastate long-term returns.

What Is Lump Sum Investing?

Lump sum investing involves committing your entire available capital to the market immediately upon receiving it. If you inherit $100,000 or sell a property for $500,000, lump sum strategy means investing every dollar the same day, regardless of current market prices.

The mathematical case for lump sum investing is straightforward: markets tend to rise over time. Historical data consistently shows that waiting to invest carries an “opportunity cost”—the returns you forfeit during the waiting period. The S&P 500 has generated approximately 10% average annual returns over nearly a century, and missing just the ten best trading days over forty years can reduce your total returns by more than half.

Research from Vanguard analyzed hypothetical scenarios across multiple decades and found that lump sum outperformed DCA approximately two-thirds of the time. The logic is compelling: if markets trend upward, getting your money working sooner rather than later generally produces superior results.

However, lump sum investing requires substantial psychological resilience. Investors must accept that their entire portfolio could decline in value shortly after investing—a difficult reality that leads many to panic during market corrections. The 2008 financial crisis saw millions of investors abandon lump sum positions, locking in losses rather than waiting for recovery.

The Research: What the Data Actually Shows

Academic research provides nuanced insights into this debate, revealing that neither strategy universally dominates the other.

Vanguard’s Landmark Study

Vanguard researchers examined rolling period returns from 1926 through 2011, comparing lump sum investing to DCA across various time horizons. Their findings revealed that lump sum investing beat DCA about 66% of the time when looking at one-year periods. Extending the DCA period to twelve months still left lump sum winning approximately 60% of the time.

The reason is simple mathematics: when markets have positive expected returns, investing earlier captures more of those returns. DCA essentially bets against this historical trend, sacrificing expected gains for reduced volatility.

Putnam Investments Analysis

Putnam researchers studied the question from 1962 through 2008, reaching similar conclusions. They found that lump sum outperformed DCA roughly 70% of the time when using a twelve-month DCA period. However, they also noted that DCA provided meaningful downside protection during severe market downturns.

Scenario Analysis

The research reveals that DCA performs best in specific conditions:

- When markets decline significantly after you receive funds

- When interest rates on cash held during DCA periods are low

- When you’re emotionally unable to handle market volatility

- When you receive funds gradually (like from a paycheck)

Lump sum performs best when:

- Markets are trending upward

- You have long investment horizons

- You can tolerate short-term portfolio volatility

- Cash drag would be costly

Comparing the Two Strategies

| Factor | Dollar Cost Averaging | Lump Sum Investing |

|---|---|---|

| Historical Win Rate | ~33-40% | ~60-67% |

| Average Underperformance | 2-4% vs lump sum | Baseline |

| Psychological Comfort | High | Moderate |

| Best For | Emotional investors, volatile markets | Long-term optimists |

| Market Timing Risk | Low | Moderate |

| Cash Drag | Higher | None |

The comparison table reveals the core trade-off: DCA wins psychologically but sacrifices expected returns. The question becomes whether that psychological comfort translates into better outcomes through reduced panic selling.

When Dollar Cost Averaging Makes Sense

Despite the mathematical headwind, DCA remains the superior choice for many investors in specific situations.

You Received a Windfall But Fear Market Timing

If you’ve inherited money or received a large bonus, jumping in immediately can feel reckless. The fear of investing right before a downturn causes analysis paralysis that stretches months—sometimes years. DCA provides a structured path forward that feels manageable, transforming overwhelming choice into simple execution.

You Have Strong Anxiety About Market Volatility

Not everyone processes market drops calmly. If watching your portfolio decline 20% would keep you awake at night or trigger selling, DCA’s gradual approach protects your mental health. The small, regular investments feel manageable even during downturns, and the knowledge that you’re “buying the dip” provides genuine comfort.

You’re Investing Through a 401(k) or Similar Plan

When money comes from regular income via payroll deduction, you’re naturally practicing DCA. Contributing 5% of each paycheck to your retirement account spreads your investments across your entire career. Trying to “time” these contributions defeats the purpose of systematic saving.

Markets Appear Overvalued

If you’re genuinely convinced markets are in a bubble—based on valuation metrics like CAPE ratio or other indicators—DCA provides a reasonable hedge. You still invest, but you reduce exposure to an immediate correction. This approach feels more comfortable than holding all cash while waiting for a crash that may never come.

When Lump Sum Investing Makes Sense

For many investors, particularly those with long time horizons and emotional resilience, lump sum remains the evidence-based choice.

You Have a Long Investment Horizon

Time is your greatest ally when investing in equities. If you’re 30 and investing for retirement at 65, a thirty-five-year window smooths out short-term volatility. The math strongly favors getting your money working immediately, capturing decades of compounding returns.

You’re Comfortable With Short-Term Volatility

If you can watch your portfolio decline 30% without panic selling, you have the psychological profile for lump sum investing. This doesn’t mean you enjoy watching losses—it means you understand the temporary nature of market downturns and trust in eventual recovery.

Markets Are Reasonably Valued

When stock valuations sit near historical averages, waiting for a better entry point offers minimal expected benefit. The research showing DCA underperformance assumes markets will eventually rise; if valuations are reasonable, that assumption seems sound.

You Want to Maximize Expected Returns

Purely from a mathematical standpoint, lump sum investing maximizes expected value. The “lost” returns from holding cash during a DCA period represent genuine opportunity cost. If your goal is maximizing wealth accumulation rather than minimizing regret, lump sum aligns with that objective.

A Hybrid Strategy: The Best of Both Worlds?

Many financial advisors now recommend a middle path that captures benefits of both approaches.

The One-Third Approach

Invest one-third of your available capital immediately. Hold one-third in cash reserves, and invest that amount over the next six to twelve months using DCA. This approach provides immediate market participation while building in a buffer for volatility.

This hybrid works particularly well for investors transitioning from DCA to lump sum thinking—those who intellectually understand the case for lump sum but haven’t built confidence in their ability to handle market drops.

The Corridor Strategy

Some investors set specific “corridors” for deployment. If markets drop 10% from current levels, they deploy another portion. If markets drop 20%, they deploy more. This creates a systematic DCA approach tied to market conditions rather than arbitrary calendar dates.

Common Mistakes Investors Make

Mistake 1: Using DCA to Time the Market

Some investors interpret DCA as permission to “wait for a better time.” They hold cash for months or years, waiting for a market correction that may never arrive. This isn’t DCA—it’s market timing with extra steps. True DCA involves regular investments regardless of conditions, not conditional waiting.

Mistake 2: Ignoring Cash Drag

When holding cash for DCA, you’re losing potential returns on that cash. Money sitting in a savings account earning 0.01% interest while you wait to invest is a genuine cost. Factor this into your decision—if cash yields are attractive, DCA makes more sense. If cash yields are negligible, lump sum becomes more attractive.

Mistake 3: Letting Perfect Be the Enemy of Good

The investor who spends months researching the “optimal” DCA schedule while holding cash is often worse off than the investor who makes a reasonable decision and acts. Don’t paralyze yourself with analysis. Choose a reasonable approach and execute.

Frequently Asked Questions

Does dollar cost averaging always work worse than lump sum?

No, dollar cost averaging doesn’t always underperform. Research shows it beats lump sum roughly one-third of the time, particularly when markets decline significantly after you receive the funds. The “average” outcome favors lump sum, but individual results vary based on when you invest and subsequent market behavior.

How long should I stretch out dollar cost averaging?

Most research compares DCA periods of 6 to 12 months. Extending beyond 12 months generally increases the performance gap favoring lump sum because cash sits idle longer. A 6-12 month DCA period represents the sweet spot for reducing volatility while limiting opportunity cost.

Is dollar cost averaging better for volatile assets like cryptocurrency?

The case for DCA strengthens with highly volatile assets where price swings are extreme and unpredictable. Crypto’s notorious volatility makes DCA particularly attractive because you’re buying across a wide range of prices. However, crypto’s fundamental uncertainty also means past performance patterns may not apply.

What if I’m investing in a retirement account like a 401(k)?

For most people with 401(k) contributions from regular income, you’re already practicing DCA through regular payroll deductions. The question becomes how to allocate new contributions—which funds to choose, not whether to dollar cost average. Lump sum vs DCA typically applies to windfalls, inherited money, or one-time investment decisions.

Should I use dollar cost averaging during a market downturn?

DCA performs best during downturns because you’re buying shares at progressively lower prices, lowering your average cost. If markets decline significantly after you begin DCA, you’ll likely end up with better results than if you’d invested everything at the start. This is one of DCA’s genuine advantages.

Can I switch between strategies based on market conditions?

Attempting to switch strategies based on market predictions essentially becomes market timing. Most evidence suggests this approach underperforms compared to committing to either DCA or lump sum consistently. Choose your strategy based on your psychological tolerance and time horizon, not current market conditions.