2Views 0Comments

How to Calculate Crypto Profit for Taxes – Complete Guide

The IRS treats cryptocurrency as property, meaning every transaction—from trading one token for another to spending crypto on purchases—can trigger a taxable event. With over 40 million Americans owning cryptocurrency and the IRS increasingly scrutinizing crypto tax reporting, understanding how to calculate your crypto profits accurately isn’t optional—it’s essential to avoid penalties, interest, and potential audits.

📊 KEY STATS

- 4 in 10 crypto owners don’t know their transactions are taxable

- $1.5 billion in crypto tax revenue was collected by the IRS from audits between 2017-2021 (IRS Data Book)

- 89% of individual tax returns with crypto transactions had errors before the IRS simplified reporting

- $7.1 trillion in crypto transactions occurred globally in 2023 (Chainalysis)

This guide walks you through every step of calculating crypto profit for taxes, from understanding your cost basis to selecting the best accounting method for your situation.

Understanding the Tax Foundation: Cost Basis and Capital Gains

Before calculating anything, you must understand two fundamental concepts: cost basis and capital gains.

Cost basis represents what you paid for your cryptocurrency, including purchase price plus any transaction fees that get added to your cost basis. When you acquire the same cryptocurrency at different prices over time, each purchase creates a separate tax lot with its own cost basis.

Capital gain or loss is the difference between your cost basis and the fair market value when you dispose of the cryptocurrency. If you sell for more than you paid, you have a capital gain. If you sell for less, you have a capital loss that can offset gains or up to $3,000 of ordinary income annually.

👤 Sarah Chen, CPA and founder of CryptoTaxPrep, explains: “Most beginners assume only profits are taxable. But understanding that losses can offset gains—and potentially lower your overall tax bill—is equally important for tax planning.”

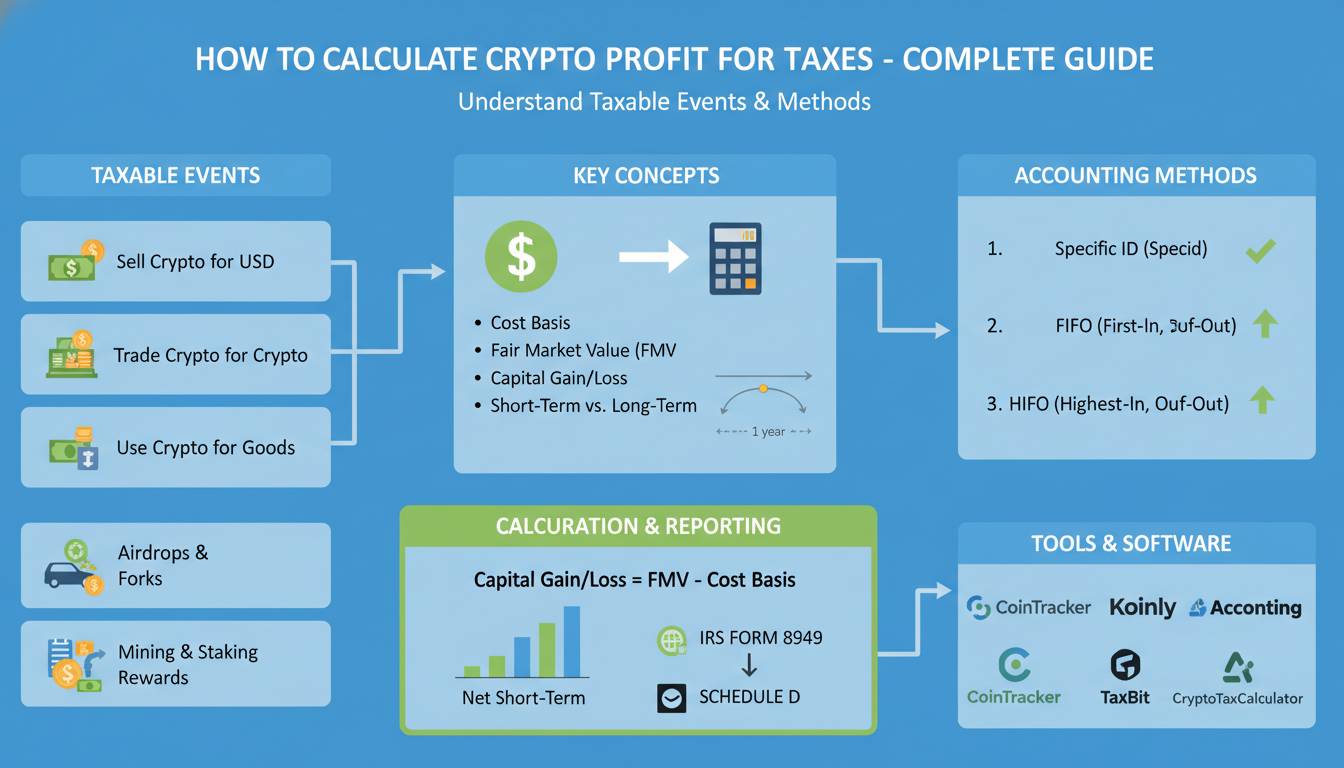

What Counts as a Taxable Disposal?

The IRS defines disposal events that trigger taxable calculations:

| Event | Taxable? | Treatment |

|---|---|---|

| Selling crypto for fiat (USD) | ✅ Yes | Capital gain/loss |

| Trading one crypto for another | ✅ Yes | Capital gain/loss (both sides) |

| Spending crypto on purchases | ✅ Yes | Capital gain/loss |

| Mining rewards | ✅ Yes | Ordinary income |

| Staking rewards | ✅ Yes | Ordinary income |

| Airdropped tokens | ✅ Yes | Ordinary income (at fair market value) |

| Gifting crypto (over $17,000/year) | ✅ Yes | Gift tax may apply |

| Inheriting crypto | ✅ Yes | Stepped-up basis |

| Holding (no sale) | ❌ No | Not taxable |

Step-by-Step: Calculating Your Crypto Profit

Step 1: Gather Complete Transaction Records

Every calculation begins with comprehensive documentation. You need:

- Date and time of every transaction

- Amount of crypto bought, sold, or traded

- USD value at the time of transaction (or foreign currency rate if applicable)

- Wallet addresses (for verification)

- Exchange statements showing cost basis

- Transaction hashes (for blockchain verification)

Pro tip: Export your transaction history from every exchange and wallet you use. Missing transactions are the #1 cause of calculation errors.

Step 2: Identify Your Tax Lots

Each unit of cryptocurrency purchased at a different time or price creates a distinct tax lot. When you sell, you must identify which specific tax lot you’re selling from—this is called “tax lot identification” and significantly impacts your tax liability.

Example Calculation:

You bought 1 BTC at these prices:

– January: 0.5 BTC at $30,000 = $15,000 basis

– March: 0.5 BTC at $40,000 = $20,000 basis

– Total: 1 BTC with mixed basis of $35,000

In June, you sell 0.5 BTC for $45,000. Your profit depends on which tax lot you identify:

If using first-in, first-out (FIFO): You’re selling the January lot (0.5 BTC with $15,000 basis)

– Proceeds: $45,000

– Basis: $15,000

– Capital gain: $30,000

If using specific identification: You choose the March lot (0.5 BTC with $20,000 basis)

– Proceeds: $45,000

– Basis: $20,000

– Capital gain: $25,000

This example shows how tax lot selection can save $5,000 in taxes.

Choosing Your Accounting Method

The method you choose for identifying tax lots determines your profit calculation. The IRS allows several approaches, each with different implications.

FIFO (First-In, First-Out)

This method sells your oldest coins first. It’s the default if you don’t specify otherwise and the simplest to implement.

| Pros | Cons |

|---|---|

| Simplest to implement | May result in higher taxes if early purchases had lower prices |

| Required by default if no method specified | Can lock in gains when you want to minimize taxes |

| Most exchanges report this way | Doesn’t allow strategic tax planning |

LIFO (Last-In, First-Out)

This method sells your most recently purchased coins first, which can be advantageous in rising markets when newer purchases have higher cost bases.

| Pros | Cons |

|---|---|

| Can minimize gains in bull markets | Complex record-keeping required |

| Matches many trading strategies | Must explicitly elect this method |

| Often results in lower short-term gains | Some exchanges don’t support this |

HIFO (Highest-In, First-Out)

This method sells your most expensive coins first, minimizing capital gains regardless of when you purchased them.

| Pros | Cons |

|---|---|

| Typically results in lowest taxable gains | Requires detailed record-keeping |

| Best for tax minimization strategies | Must be consistent throughout the year |

| Works well in any market condition | More administrative burden |

Specific Identification

This method lets you specify exactly which tax lots to sell at the time of each transaction. It offers maximum flexibility but requires precise documentation.

When to use each method:

- FIFO: Beginners, simple portfolios, automated systems

- LIFO: Active traders in rising markets who want to match recent activity

- HIFO: Anyone prioritizing tax minimization

- Specific ID: Large portfolios, complex situations, strategic tax planning

Short-Term vs. Long-Term Capital Gains

The duration you hold cryptocurrency before selling determines whether your profits are taxed as short-term or long-term capital gains—a distinction that dramatically affects your tax rate.

| Holding Period | Classification | Tax Rate (2024) |

|---|---|---|

| Less than 1 year | Short-term | Ordinary income tax (10-37%) |

| 1 year or more | Long-term | 0%, 15%, or 20% |

👤 Mark Thompson, enrolled agent and crypto tax specialist at TaxCrypto, advises: “If you’re sitting on significant gains, holding for just one additional month can mean the difference between paying 37% and 20% in federal taxes. On a $100,000 gain, that’s $17,000 in tax savings.”

Planning Opportunity

Review your holdings around tax year-end. If you have assets with substantial gains you’ve held less than a year, consider whether waiting until after the one-year mark makes sense. Conversely, if you have losses you want to harvest, selling before the one-year mark lets you offset higher-taxed ordinary income.

Income Events: Mining, Staking, and Airdrops

Not all crypto earnings come from buying low and selling high. The IRS treats certain acquisition methods as ordinary income, taxed at your marginal income tax rate.

Mining Income

When you mine cryptocurrency, the fair market value of coins received is taxable as ordinary income in the year received. Your cost basis in those coins then becomes that same fair market value.

Example:

You mine 1 ETH in February when ETH is worth $2,500. You report $2,500 as ordinary income. Your cost basis in that ETH is $2,500.

When you later sell that ETH, your capital gain or loss is calculated from the $2,500 basis.

Staking Rewards

Similar to mining, staking rewards are taxed as ordinary income at fair market value when you receive them. This applies to proof-of-stake chains including Ethereum (post-Merge), Solana, Cardano, and others.

Airdrops and Forks

Airdrops—whether from marketing campaigns or hard forks—create ordinary income equal to the fair market value of tokens received. This applies even if you didn’t request the tokens or they have uncertain value at receipt.

⚠️ CRITICAL: The IRS position is that you have income even if you can’t sell or transfer tokens immediately. Document the fair market value on the date of receipt carefully.

Reporting Crypto on Your Tax Return

Once you’ve calculated your gains and losses, proper reporting is essential.

Form 8949 and Schedule D

Individual crypto transactions are reported on Form 8949 (Sales and Other Dispositions of Capital Assets), then summarized on Schedule D (Capital Gains and Losses). Each transaction requires:

- Description of property

- Date acquired

- Date sold

- Proceeds

- Cost basis

- Gain or loss

For most individual taxpayers, exchanges will send Form 1099-DA starting in 2025 (for 2024 transactions) showing transaction details. However, don’t rely solely on this—exchange 1099s may not capture all taxable events or may have errors.

The Wash Sale Rule

While the wash sale rule traditionally applied to securities, the IRS has increasingly applied similar principles to crypto. The safest approach: avoid purchasing “substantially identical” cryptocurrency within 30 days before or after selling at a loss. Otherwise, your loss deduction may be disallowed.

Tools and Software for Crypto Tax Calculation

Manual calculation is impractical for active traders. Specialized software automates the process by connecting to exchanges and wallets.

| Tool | Best For | Starting Price | Key Feature |

|---|---|---|---|

| CoinTracker | Beginners | $49/year | Best exchange integration |

| Koinly | International users | $49/year | Most tax jurisdictions supported |

| TaxBit | High-volume traders | $99/year | Advanced accounting features |

| CryptoTrader.Tax | Budget-conscious | $19/year | Affordable for small portfolios |

| Zen Ledger | DeFi/NFT users | $99/year | Best for complex transactions |

What to Look For

- Exchange compatibility: Ensure supports all exchanges you use

- DeFi and NFT support: Critical if you use decentralized protocols

- Tax lot selection: Should allow FIFO, LIFO, HIFO, and specific ID

- Import accuracy: Verifies transactions against blockchain data

- Tax loss harvesting: Identifies opportunities to minimize taxes

Common Mistakes to Avoid

❌ MYTH: “I only need to report when I cash out to USD.”

✅ REALITY: Trading one cryptocurrency for another is a taxable disposal event. Every trade triggers potential capital gains calculations.

❌ MYTH: “My exchange doesn’t report to the IRS.”

✅ REALITY: Starting in 2024 (for 2025 filing), exchanges must report transactions over $600 via Form 1099-DA. The IRS also receives data from blockchain analysis companies.

❌ MYTH: “I’ll just estimate my gains.”

✅ REALITY: Estimation leads to incorrect reporting, penalties, and potential audit triggers. The IRS requires specific documentation for each transaction.

❌ MYTH: “I can offset crypto gains with stock losses easily.”

✅ REALITY: Crypto gains and losses are reported on Schedule D just like stocks, so they can offset each other. However, only $3,000 of net capital loss can offset ordinary income per year.

Special Considerations

DeFi and Yield Farming

Decentralized finance transactions often create multiple taxable events. Providing liquidity might trigger taxable events when tokens are deposited and when removed. Yield farming rewards are typically ordinary income. These require especially careful tracking.

NFTs

Creating and selling NFTs: ordinary income or capital gain depending on whether you’re the creator. Selling NFT investments: capital gains. Purchases with NFTs: taxable disposal of the NFT.

Foreign Accounts

If you use foreign exchanges, you may need to file FinCEN Form 114 (FBAR) if your foreign crypto accounts exceed $10,000 at any point during the year.

Conclusion

Calculating crypto profit for taxes requires understanding cost basis, selecting an appropriate accounting method, distinguishing short-term from long-term gains, and properly reporting income events. While the complexity can feel overwhelming, systematic record-keeping and the right tools make the process manageable.

The most effective strategy combines year-round transaction tracking with tax-lot optimization at year-end. Review your holdings regularly, consider holding periods when making selling decisions, and consult a tax professional for complex situations involving significant transactions, DeFi activities, or international accounts.

Remember: the goal isn’t just compliance—it’s strategic tax management that preserves more of your crypto gains.

Frequently Asked Questions

Do I have to pay taxes on crypto if I didn’t sell?

Holding cryptocurrency itself is not a taxable event. You only owe taxes when you dispose of crypto through selling, trading, spending, or receiving it as income. However, keep records of your cost basis for when you eventually sell.

What happens if I don’t report my crypto transactions?

Failure to report can result in penalties ranging from 20% to 75% of the underpaid tax, plus interest. The IRS has increased enforcement significantly, using blockchain analysis to identify non-reporters. Voluntary disclosure programs exist for those who haven’t reported, but penalties increase the longer you wait.

Can I deduct my crypto losses?

Yes. Capital losses from crypto can offset capital gains from any source (crypto or other investments). If your losses exceed your gains, you can deduct up to $3,000 against ordinary income annually, with excess losses carried forward to future years.

How do I calculate profit if I received crypto as a gift?

You inherit the giver’s cost basis (carryover basis). If you don’t know the giver’s basis, you must determine fair market value at the time of receipt using available historical data. When you eventually sell, your gain or loss is the difference between proceeds and this inherited basis.

What records do I need to keep?

Maintain records for every transaction including: date, type of transaction, amount in crypto and USD value, wallet addresses involved, exchange records, and any fees. Keep these records for at least 7 years in case of IRS audit. Using tax software that maintains blockchain-verified records provides the strongest documentation.