16Views 0Comments

Snowball vs Avalanche: Which Debt Payoff Method Wins?

The average American household carries $8,884 in credit card debt, with total U.S. consumer debt exceeding $17 trillion. For millions of households, the question isn’t whether to pay off debt—it’s how to do it most effectively. Two methods dominate the conversation: the debt snowball and the debt avalanche. Both are proven strategies endorsed by financial experts, but they work in fundamentally different ways and produce different results depending on your financial situation and psychological makeup.

The short answer: The avalanche method saves more money mathematically, while the snowball method provides faster psychological wins. The “winner” depends entirely on your debt profile, your motivation style, and whether you need early victories to stay committed to the payoff journey.

Understanding the Debt Snowball Method

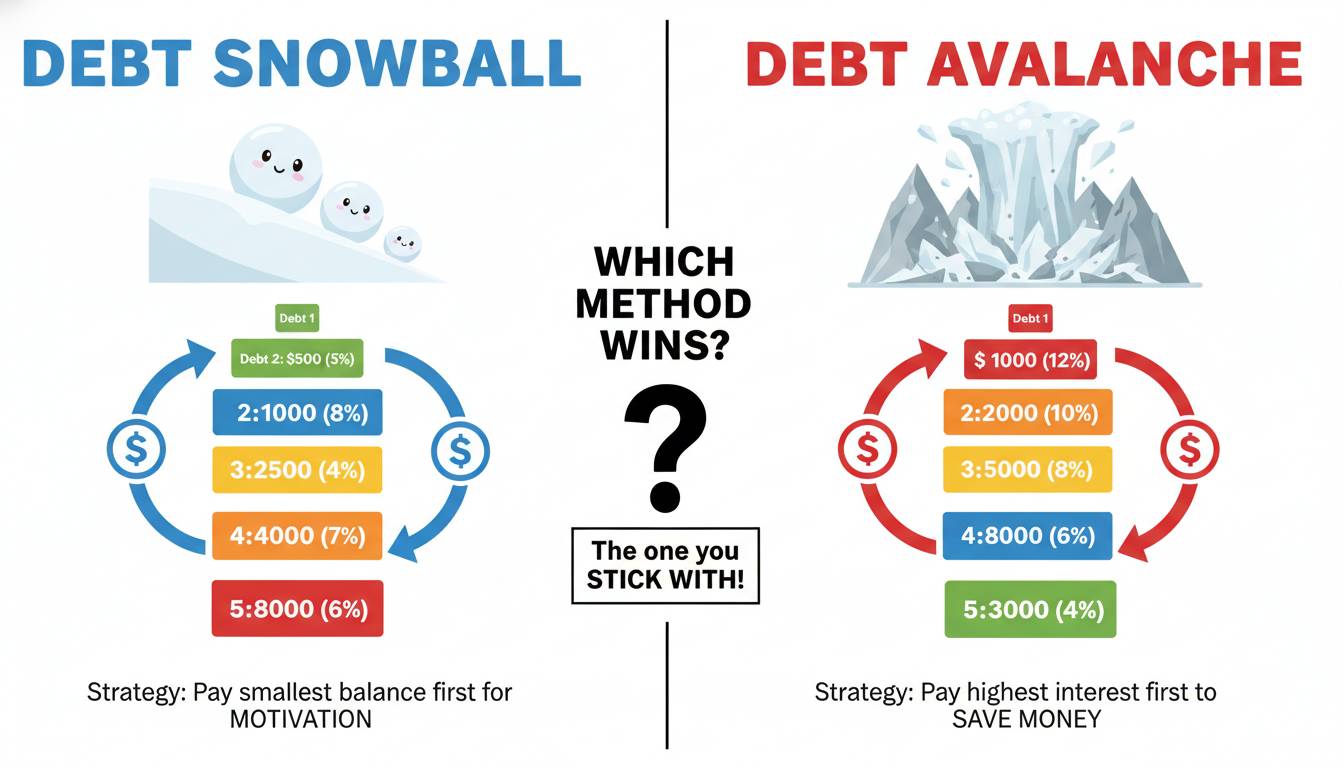

The debt snowball method, popularized by financial guru Dave Ramsey, prioritizes paying off smallest balances first while making minimum payments on all other debts. Once the smallest debt is eliminated, you roll that payment into the next-smallest balance, creating a “snowball” effect that accelerates your progress.

Key principles of the snowball approach:

- Debts are ranked by balance size, not interest rate

- Psychological momentum is the primary goal

- Quick wins keep motivation high throughout the process

- Extra payments beyond minimums go to the smallest debt

This method appeals to people who struggle with delayed gratification or have become discouraged by their debt payoff journey. The immediate satisfaction of eliminating an entire account provides tangible evidence that progress is possible.

Understanding the Debt Avalanche Method

The debt avalanche method takes the opposite approach: you prioritize paying off debts with the highest interest rates first, regardless of balance size. Mathematically, this minimizes the total interest paid over time, making it the most cost-efficient strategy.

Key principles of the avalanche approach:

- Debts are ranked by interest rate, highest to lowest

- Total interest savings is the primary objective

- Longer-term financial optimization takes precedence

- Extra payments go toward the highest-rate debt

Financial professionals generally recommend this method for people who can stay motivated without immediate visual wins, as it requires more patience but delivers superior mathematical outcomes.

Side-by-Side Comparison: Snowball vs Avalanche

| Factor | Snowball Method | Avalanche Method |

|---|---|---|

| Primary Sort | Smallest balance first | Highest interest rate first |

| Total Interest Paid | Higher | Lower (typically 10-20% less) |

| Payoff Speed (First Debt) | Faster | Depends on balance |

| Psychological Momentum | Stronger | Weaker initially |

| Best For | Motivational debtors | Mathematical optimizers |

| Risk of Quit | Lower | Higher without discipline |

📊 KEY INSIGHT: According to a 2019 study published in the Journal of Financial Counseling and Planning, borrowers using the snowball method were 36% more likely to stay on track with their debt payoff plans compared to those using the avalanche method, despite paying more interest overall.

When the Snowball Method Makes Sense

The snowball method isn’t just for beginners—it genuinely serves specific situations better.

You should choose snowball if:

- You have multiple small debts that feel overwhelming

- You’ve tried paying off debt before and quit

- Your self-discipline wavers without visible progress

- You have high-interest debt but also several small balances

- You need to rebuild confidence in your financial abilities

The psychological boost from eliminating a credit card with a $500 balance can provide the momentum needed to tackle larger debts like car loans or student loans. This method treats debt payoff as a behavioral change, not just a mathematical problem.

Real scenario: Sarah has four debts—a $400 medical bill, a $1,200 credit card, a $5,000 car loan, and $12,000 in student loans. Using the snowball method, she attacks the medical bill first. Within 2-3 months, she has one less creditor to pay, one fewer monthly bill to manage, and concrete proof that becoming debt-free is achievable.

When the Avalanche Method Makes Sense

The avalanche method serves sophisticated financial planners who understand compound interest and can maintain focus on long-term goals.

You should choose avalanche if:

- You’re naturally disciplined with money

- Your highest-interest debt also happens to be your largest

- You have strong self-control and don’t need frequent wins

- You’re mathematically inclined and want to optimize

- Your debts have widely varying interest rates (15% vs 25%+)

The math advantage: On a $10,000 debt at 20% APR versus $5,000 at 10% APR, the avalanche method would direct extra payments to the 20% debt first. Over 36 months, this approach could save $1,500-$2,000 in interest compared to snowballing the smaller balance first.

👤 EXPERT INSIGHT: “The avalanche method is objectively superior from a pure financial perspective,” says licensed financial planner Michael Taylor. “But personal finance is personal. If the method that saves money causes you to quit, it actually costs you more.”

A Real-World Example: $20,000 in Credit Card Debt

Let’s compare both methods using a realistic scenario:

The debts:

– Credit Card A: $3,000 at 22.99% APR

– Credit Card B: $7,000 at 26.99% APR

– Credit Card C: $10,000 at 19.99% APR

Monthly payment capacity: $800 (plus minimums)

Snowball Approach

- Month 1-4: Pay $800 toward Card A (minimum ~$75 on others). Eliminate Card A in 4 months.

- Month 5-11: Roll $800 into Card C (now $1,875/month total toward Card C). Eliminate Card C in 7 months.

- Month 12-22: All $800 goes to Card B. Eliminate Card B in 11 months.

Total time: 22 months | Total interest paid: Approximately $5,800

Avalanche Approach

- Month 1-8: Pay $800 toward Card B (highest rate). Eliminate in 8 months.

- Month 9-14: Roll $800 into Card A ($1,475/month). Eliminate in 6 months.

- Month 15-21: All $800 toward Card C. Eliminate in 7 months.

Total time: 21 months | Total interest paid: Approximately $4,900

Difference: The avalanche method saves about $900 in interest and finishes one month faster—just by prioritizing interest rate over balance size.

Common Mistakes That Derail Both Methods

Regardless of which method you choose, certain errors can sabotage your progress:

| Mistake | Impact | Solution |

|---|---|---|

| Not cutting up credit cards | Easy to rack up new debt | Freeze cards or physically destroy them |

| Treating raises as new income | Slows payoff significantly | Automatically redirect raises to debt |

| Ignoring emergency fund | Derails progress when unexpected expenses hit | Build $1,000 mini-emergency fund first |

| Making only minimum payments | Debt lasts decades | Always pay more than minimum |

| Trying to payoff too aggressively | Burnout and financial strain | Budget for enjoyment too |

⚠️ IMPORTANT: Before aggressive debt payoff, ensure you have at least a basic emergency fund. Without one, unexpected expenses will force you back into debt, negating your progress.

Hybrid Approaches: Getting the Best of Both

Financial flexibility often beats ideological purity. Some borrowers achieve optimal results by combining elements of both methods:

The modified snowball: Pay off 1-2 smallest debts first (for momentum), then switch to avalanche for remaining debts. This provides early wins while still optimizing long-term interest.

The hybrid approach: Attack high-interest debt first but celebrate milestones along the way. Track progress visually with charts or apps to maintain motivation.

The debtCCS (Consumer Credit Counseling Service) method: Work with a certified credit counselor to negotiate lower interest rates, then apply snowball or avalanche to the reduced balances.

Expert Perspectives: What Financial Professionals Recommend

Different experts emphasize different approaches based on their client experience:

👤 Jean Chatzky, CEO of HerMoney Media:

“Most people need the psychological win that snowball provides. Money is emotional. If the mathematically perfect plan causes you to quit, it’s the wrong plan.”

👤 Suze Orman, Financial Author:

“The avalanche method should be the default, but only for those who can actually stick with it. Most people cannot.”

👤 Anthony C. B. Chen, CFP®:

“I’ve seen clients succeed with both methods. The best method is the one you’ll actually follow. I ask clients: ‘Will you stay motivated if you don’t see a debt eliminated for 18 months?’ If they hesitate, we go snowball.”

Making Your Decision: A Practical Framework

Answer these questions to determine which method suits you:

Question 1: Have you successfully paid off debt before?

– Yes → Avalanche may work

– No → Start with Snowball

Question 2: Is your highest-interest debt also your largest debt?

– Yes → Avalanche makes more sense

– No → Snowball may provide better momentum

Question 3: Do you need to see progress quickly to stay motivated?

– Yes → Snowball is your choice

– No → Avalanche optimizes savings

Question 4: How much total interest are you paying?

– Under $2,000 difference → Choose based on motivation style

– Over $5,000 difference → Strong argument for Avalanche

Conclusion

The snowball vs. avalanche debate ultimately misses the point: the best debt payoff method is the one you’ll stick with. The avalanche method saves money—the snowball method saves willpower. Both work when applied consistently.

If you’re motivated by quick wins and need momentum to stay committed, the snowball method delivers psychological victories that compound into lasting behavioral change. If you’re disciplined by nature and can visualize the end goal without frequent reinforcement, the avalanche method will save you hundreds or thousands in interest.

The ultimate strategy: Choose the method that matches your personality, track your progress religiously, and celebrate every debt eliminated—no matter how small. Debt freedom isn’t just about the math; it’s about transforming your relationship with money entirely.

Frequently Asked Questions

Which method saves more money?

The avalanche method saves more money mathematically—typically 10-20% less in total interest compared to the snowball method. However, the difference often amounts to hundreds rather than thousands of dollars for average consumer debt.

Can I switch methods halfway through?

Yes, absolutely. Many people start with snowball for motivation and switch to avalanche once they’ve built momentum. Others realize their original choice doesn’t match their personality and adjust accordingly.

Do both methods work for all types of debt?

Both methods work for any revolving debt (credit cards, lines of credit) and installment loans (auto loans, personal loans). For fixed-rate loans like mortgages or student loans with very low rates, acceleration may not provide meaningful savings.

How much extra should I pay each month?

Even $50-100 extra per month can shave years off your payoff timeline. Use the debt avalanche calculator to see exactly how small extra payments impact your total interest and payoff date.

Should I pay off my mortgage using these methods?

These strategies are typically recommended for consumer debt (credit cards, auto loans, personal loans). Mortgage debt usually has lower interest rates and different tax implications, making aggressive early payoff less beneficial than investing the difference.

What if I have student loans with different interest rates?

Federal student loans have fixed rates that are generally lower than credit card rates. Private student loans vary more widely. Consider consolidating or refinancing private loans to a lower rate, then apply snowball or avalanche to the remainder.