2Views 0Comments

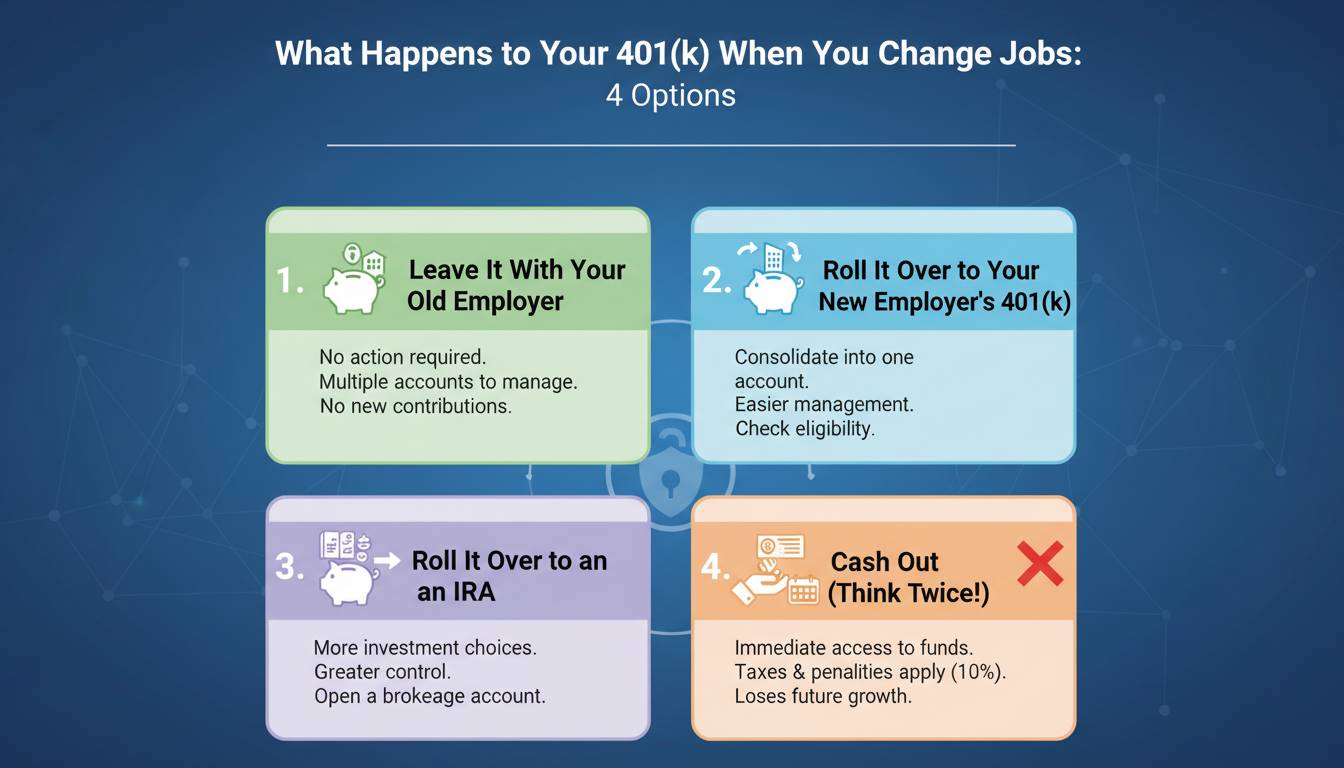

What Happens to Your 401(k) When You Change Jobs: 4 Options

When you leave your job, one of the most important financial decisions you’ll face is what to do with the money you’ve accumulated in your employer’s 401(k) plan. With millions of Americans switching jobs throughout their careers—research suggests the average worker will change jobs 12 times during their working life—this is a question that affects nearly everyone saving for retirement. The good news is that your 401(k) doesn’t disappear when you punch out for the last time. In fact, you have multiple pathways to preserve and continue growing your retirement savings.

Your 401(k) remains yours regardless of employment status. The money in your account is legally your property, and you cannot lose it simply by changing jobs. However, the choices you make about what to do with those funds can significantly impact your long-term retirement security, your tax situation, and your investment costs. Making an informed decision requires understanding all four primary options available to you, along with the advantages, disadvantages, and tax implications of each.

This guide breaks down exactly what happens to your 401(k) when you change jobs, walks through each option in detail, and provides the expert insights you need to choose the strategy that best fits your financial situation.

Understanding Your 401(k) Options at a Glance

When you leave an employer, federal law provides you with four main courses of action for your existing 401(k) balance. Each option carries different tax consequences, investment opportunities, and levels of administrative convenience. Before diving into the details, here’s a high-level overview of your choices:

Option 1: Leave It with Your Former Employer

Many employer-sponsored retirement plans allow you to keep your money in the plan even after you’ve terminated employment. This is sometimes called a “left-behind” 401(k) or maintaining a “former employee” account.

Option 2: Roll Over to a New Employer’s 401(k)

If your new company offers a retirement plan, you can typically transfer your old 401(k) balance into your new employer’s plan, consolidating your retirement savings in one location.

Option 3: Roll Over to an Individual Retirement Account (IRA)

You can move your 401(k) funds into a Traditional IRA or Roth IRA at a brokerage firm of your choice, maintaining the tax-advantaged status of your savings while gaining more control over your investment options.

Option 4: Cash Out the Account

You can withdraw the entire balance, though this option comes with significant tax consequences and penalties that make it generally inadvisable for most workers.

The option that’s right for you depends on factors including whether your new employer offers a 401(k), your desired level of investment control, fee structures, and your specific retirement timeline. Let’s examine each option in depth.

Option 1: Leave Your 401(k) with Your Former Employer

How It Works

After separating from your employer, you can typically elect to keep your money invested in your former company’s 401(k) plan. The account remains open, continues to grow tax-deferred, and you maintain your existing investment selections (though you may be restricted from making new contributions or changing allocations depending on the plan’s specific rules).

Key Advantages

No Immediate Tax Consequences

Leaving money in a 401(k) triggers no taxes or penalties. The funds remain in a tax-advantaged environment until you eventually withdraw them in retirement.

Preserves Certain Protections

401(k) plans offer strong federal protections against creditors under the Employee Retirement Income Security Act (ERISA). This can provide peace of mind if you have concerns about potential legal judgments.

Potentially Lower Costs for Large Balances

Some high-cost employer plans actually charge lower administrative fees for larger account balances, meaning leaving your money could mean lower annual fees compared to moving to a small IRA.

Maintains Special Tax Treatment for Company Stock

If your 401(k) contains significant company stock that has appreciated substantially, leaving the account may allow you to take advantage of net unrealized appreciation (NUA) tax rules when you eventually take distributions—a potential tax benefit that’s lost if you roll over to an IRA.

Important Considerations

Limited Investment Options

You’re restricted to the investment choices offered by your former employer’s plan, which may be limited or include expensive actively managed funds.

Potential for Higher Fees

Employer plans often charge higher administrative fees than low-cost IRA providers, particularly for smaller account balances. These “recordkeeping” fees can eat into returns over time.

Multiple Accounts Complexity

If you’ve changed jobs multiple times and left 401(k) accounts with several former employers, managing multiple retirement accounts becomes increasingly complicated. Research indicates that American workers accumulate an average of 11 different employer retirement plans throughout their careers.

Forced Cash-Out for Small Balances

Under current regulations, employers can require you to roll over or cash out balances below $5,000 (though they must provide notice and give you time to respond). Balances under $1,000 may be automatically cashed out and sent to your address.

Option 2: Roll Over to Your New Employer’s 401(k)

How It Works

If your new workplace offers a 401(k) or similar retirement plan, you can initiate a direct rollover (sometimes called a “transfer”) that moves your old 401(k) balance into your new employer’s plan without triggering taxes or penalties.

Key Advantages

Consolidation of Retirement Savings

Combining multiple 401(k) accounts into one makes it easier to track your overall retirement savings, understand your asset allocation, and manage required minimum distributions later in life.

Maintains Tax-Deferred Status

A direct rollover to another 401(k) preserves the tax-deferred growth of your retirement savings without any immediate tax consequences.

Potentially Access to Better Investment Options

If your new employer’s plan offers lower-cost investment options, a wider selection of funds, or access to low-cost index funds, consolidating could improve your overall investment portfolio.

May Preserve Penalty-Free Access

Some 401(k) plans allow in-service withdrawals or loans that wouldn’t be available if your money were in an IRA, providing additional flexibility if you need access to funds before retirement age.

Important Considerations

New Plan’s Investment Options

You’re limited to whatever investment choices your new employer offers, which may not be as diverse or low-cost as what you could access through an IRA.

New Plan’s Fee Structure

Employer plans vary significantly in their administrative fees and expense ratios. Before rolling over, examine the new plan’s fee disclosure to ensure you’re not moving to a more expensive option.

Waiting Periods

Some employers impose eligibility waiting periods before you can contribute to their 401(k) or before employer matching contributions begin. If there’s a gap before you can participate in the new plan, this could temporarily interrupt your retirement contributions.

Creditor Protections Vary

While 401(k) plans generally have strong creditor protections, these protections only apply to the new employer’s plan if it maintains ERISA coverage. Certain governmental or church plans may have different protection levels.

Option 3: Roll Over to an Individual Retirement Account (IRA)

How It Works

You can move your 401(k) funds into a Traditional IRA (if coming from a traditional 401(k)) or a Roth IRA (if coming from a Roth 401(k)), either through a direct rollover or by receiving a check and depositing it into an IRA within 60 days.

Key Advantages

Unlimited Investment Choices

Unlike employer plans restricted to a menu of selected funds, IRAs at brokerage firms give you access to virtually any investment—individual stocks, bonds, mutual funds, ETFs, and more.

Typically Lower Costs

Many IRA providers offer extremely low-cost index funds and ETFs with expense ratios a fraction of what employer plans often charge. This fee difference can save tens of thousands of dollars over decades of compounding.

More Control Over Asset Allocation

With complete flexibility to buy and sell any investments, you can construct exactly the portfolio allocation you want and adjust it as your goals or risk tolerance changes.

Easier Estate Planning

IRAs offer straightforward beneficiary designations and can be easily integrated into your overall estate plan, making it simpler to ensure your retirement savings go where you intend.

Potential for Backdoor Roth Contributions

If your income exceeds Roth IRA eligibility limits, having a Traditional IRA can complicate the “backdoor Roth” strategy due to pro-rata rules. However, a direct rollover from a traditional 401(k) to a Traditional IRA maintains simplicity.

Important Considerations

Different Creditor Protection Levels

Traditional and Roth IRAs receive protection under federal bankruptcy law (up to approximately $1.3 million, adjusted periodically), but state creditor protections vary and are generally weaker than ERISA protections for 401(k) accounts.

No Access to Company Stock NUA Benefits

If your old 401(k) held significant appreciated company stock, rolling to an IRA eliminates the ability to take advantage of net unrealized appreciation tax treatment, potentially resulting in higher taxes if the stock represents a large portion of your balance.

Required Minimum Distribution Rules

Unlike some 401(k) plans that allow you to delay distributions past age 73 if you’re still working, IRAs require you to begin taking required minimum distributions at age 73 (for those reaching age 73 in 2023 or later), regardless of whether you’re still working.

Option 4: Cash Out Your 401(k)

How It Works

You can simply withdraw all funds from your 401(k), receiving a check for the balance minus any mandatory withholding.

Key Disadvantages and Consequences

Immediate Tax Hit

Any distribution from a traditional 401(k) is taxed as ordinary income in the year received. If you were in the 24% federal tax bracket, a $100,000 withdrawal becomes $76,000 after federal taxes—before state taxes.

10% Early Withdrawal Penalty

If you cash out before reaching age 59½, the IRS imposes an additional 10% penalty on the taxable portion of your withdrawal, unless you qualify for specific exceptions (such as death, disability, or certain financial hardships).

Lost Compounding Growth

Perhaps the greatest cost is invisible: the future investment returns you’ll forgo by removing your money from a tax-advantaged account. Someone who cashes out $50,000 at age 35 could lose over $250,000 in potential growth by age 65, assuming a 7% annual return.

State Taxes and Withholding

Most states tax 401(k) distributions as ordinary income, and your former employer will typically withhold 20% for federal taxes—meaning you may owe additional taxes come tax filing time.

When It Might Be Appropriate

Cashing out should generally only be considered as a last resort. However, there are limited scenarios where it might make sense:

- Financial hardship meeting IRS criteria: Certain immediate financial needs may qualify for penalty-free withdrawals, though taxes will still apply.

- Very small balance with no other options: If you have less than $1,000 and cannot afford to pay rent or buy essentials, a cash-out might be more practical than managing a small account.

- Short-term financial crisis: This should only be considered after exploring all other options, including loans from other sources, cutting expenses, or seeking emergency assistance.

Financial advisors almost universally recommend avoiding cash-outs, as the immediate tax consequences and lost compounding can dramatically undermine your retirement security.

Critical Factors to Consider Before Making Your Decision

Tax Implications

The tax treatment of your decision significantly impacts its overall value. A direct rollover—whether to another 401(k) or an IRA—maintains your tax-advantaged status and defers taxes until you withdraw funds in retirement. However, if you take a distribution and don’t complete a rollover within 60 days, the IRS treats it as a taxable event, and you’ll face the 10% penalty if you’re under 59½.

Timing Considerations

60-Day Rollovers

If you receive a check from your old 401(k), you have 60 days to deposit those funds into an eligible retirement account to avoid taxes and penalties. Missing this deadline is a costly mistake.

Year-of-Transfer Rules

Rollovers completed in the same calendar year avoid immediate taxation, while those crossing years can create complex tax situations. Working with a tax professional can help you navigate these nuances.

Investment Expense Ratios

The fees you pay in investments can dramatically affect your final retirement balance. Employer plans frequently include actively managed funds with expense ratios of 0.5% to 1.0% or higher, while low-cost index funds in IRAs may charge 0.03% to 0.15%. Over 30 years, this difference can translate to tens of thousands of dollars in lost returns on a typical balance.

Employer Stock Concentration

If your old 401(k) holds a significant portion of your former employer’s stock, special considerations apply. Keeping the stock in a 401(k) or moving it to another employer plan allows you to potentially defer capital gains taxes through net unrealized appreciation (NUA) treatment when you eventually take distributions. Rolling to an IRA generally eliminates this benefit.

Common Mistakes to Avoid

Mistake #1: Taking a Check and Cashing Out Unintentionally

Some employees, eager to “close the chapter” on their old job, request a check for their 401(k) balance without understanding the tax consequences. If you receive a check and don’t deposit it into an eligible retirement account within 60 days, it’s treated as a taxable distribution.

Solution: Always request a direct trustee-to-trustee transfer if you want to move your money without taxes.

Mistake #2: Ignoring Small Balance Accounts

Workers who change jobs frequently sometimes accumulate numerous small 401(k) accounts, losing track of them entirely. These “forgotten” accounts can be subject to escheatment (being turned over to the state) if left unclaimed.

Solution: Track all retirement accounts and consider consolidating when you change jobs.

Mistake #3: Not Comparing Investment Options

Automatically rolling over to a new employer’s 401(k) without comparing investment options and fees can mean ending up with a more expensive portfolio.

Solution: Review the expense ratios and investment choices in both your old and new plans, as well as IRA alternatives, before deciding.

Mistake #4: Missing Required Minimum Distributions

Some workers who leave their 401(k) with a former employer forget that required minimum distributions still begin at age 73 (for those born in 1951 or later). Missing RMDs results in a 25% penalty on the amount that should have been distributed.

Solution: Mark RMD deadlines on your calendar or work with a financial advisor to ensure compliance.

How to Decide: A Decision Framework

Choosing the right option depends on your specific circumstances. Here’s a practical framework to guide your decision:

Choose to Leave It with Your Former Employer If:

– Your old plan has excellent, low-cost investment options

– You have a very large balance and want to preserve creditor protections

– You hold significant company stock and want to preserve NUA tax benefits

– You plan to return to that employer eventually

Choose to Roll Over to a New Employer’s 401(k) If:

– Your new plan has good investment options with low fees

– You want to consolidate all your retirement savings in one place

– You value the simplicity of having a single retirement account

– You want to maintain access to possible plan loans

Choose to Roll Over to an IRA If:

– You want maximum control over your investment choices

– You can find lower-cost investment options than your employer plans

– You value the ability to implement any investment strategy you choose

– You’re comfortable managing the account yourself or working with a broker

Consider Cashing Out Only If:

– You’re facing a true financial emergency with no alternatives

– The balance is so small that the administrative burden exceeds the value

– You’ve exhausted all other options and have an immediate, critical need

Expert Insights: What Financial Advisors Recommend

Financial professionals consistently emphasize that the “best” option depends on individual circumstances, but some patterns emerge from expert guidance:

On Consolidation: “In most cases, I recommend consolidating old 401(k)s into an IRA, unless the new employer’s plan has exceptional features or lower costs,” says Michael RFC, a certified financial planner. “The simplicity of having one account to manage, combined with typically lower investment costs, usually wins out.”

On Avoiding Cash-Outs: “The biggest mistake I see is people cashing out their 401(k) when changing jobs,” notes a retirement planning specialist. “That immediate cash looks appealing, but the tax hit and lost compound growth can cost you hundreds of thousands of dollars in the long run.”

On Professional Guidance: “If your 401(k) holds company stock or you’re dealing with complex tax situations, it absolutely makes sense to consult a tax advisor or fee-only financial planner before making your decision,” advises another financial expert. “The cost of professional guidance is minimal compared to making a costly mistake.”

Frequently Asked Questions

Can I take my 401(k) with me when I change jobs?

Yes, you have several options to take your 401(k) with you. You can roll it over to your new employer’s 401(k), roll it over to an IRA, or leave it in your former employer’s plan. You can also choose to cash it out, though this comes with significant tax penalties if you’re under age 59½.

What happens if I don’t do anything with my 401(k) when I leave my job?

If you don’t take action, your 401(k) will typically remain in your former employer’s plan, continuing to grow tax-deferred. However, the plan may have provisions that force a cash-out if your balance is below $5,000. It’s important to verify your account status and understand your plan’s specific rules to avoid unintended consequences.

Will I pay taxes if I roll over my 401(k) to an IRA?

No, if you complete a direct trustee-to-trustee transfer, you won’t pay taxes immediately. The money moves from one tax-advantaged account to another, maintaining its tax-deferred status. However, if you receive a check and don’t deposit it within 60 days, the IRS treats it as a taxable distribution.

Is it better to roll my 401(k) into an IRA or keep it in my employer’s plan?

This depends on your specific situation. An IRA typically offers more investment choices and often lower fees, while keeping your 401(k) with a former employer may preserve certain creditor protections and company stock tax benefits. Compare the investment options, fees, and your specific needs before deciding.

Can I partially roll over my 401(k)?

Yes, you can typically choose to roll over only a portion of your 401(k) balance while leaving the rest in your former employer’s plan or taking a different action with a portion. This can be useful if you want to keep company stock for NUA treatment while moving other assets to an IRA.

What is the deadline to roll over my 401(k) after changing jobs?

For a 60-day rollover (where you receive a check), you have 60 days from receiving the distribution to deposit it into an eligible retirement account. However, the preferred method is a direct trustee-to-trustee transfer, which has no deadline and avoids any tax withholding.

Conclusion: Protecting Your Retirement Future

Your 401(k) represents years of hard work and savings, and making smart decisions when changing jobs can preserve—and potentially grow—that wealth. The four options available—leaving your money with your former employer, rolling to a new employer’s plan, rolling to an IRA, or cashing out—each serve different needs and circumstances.

For most workers, a direct rollover to a low-cost IRA offers the greatest flexibility, typically lower fees, and unlimited investment choices. However, specific situations—such as needing strong creditor protection, holding significant company stock, or having access to an exceptionally good employer plan—may make one of the other options more appropriate.

Whatever you do, avoid the temptation to cash out unless you face a true emergency. The immediate tax consequences and the loss of decades of tax-deferred compounding can dramatically undermine your retirement security. Take time to compare your options, consider the long-term implications, and make a decision that will serve you well for the rest of your life.

Your retirement savings worked hard to grow while you were employed. Now it’s your job to ensure that money continues working just as hard for you.